At Blue Harbinger, we tend to write frequently about investments that pay big dividends. However, not all attractive investments pay a dividend. This article focuses on an attractive “disciplined growth” company, that currently pays zero dividend, but has very attractive price appreciation potential, and it is currently “on sale,” in our view.

Ellie Mae Inc (ELLI)

Ellie Mae is a leading provider of innovative on-demand software solutions and services for the residential mortgage industry. We have written about Ellie Mae’s attractiveness in the past, but we do not own shares. Here is our previous detailed Ellie Mae article from back in December:

And the price climbed dramatically since that article, but the recent price decline is giving potential investors another bite at the apple.

Specifically, the price decline (as shown in the above chart) has increased our interest level, and that’s why we’re writing this article (i.e. Ellie Mae is high on our watch list, and we may buy shares in the near future).

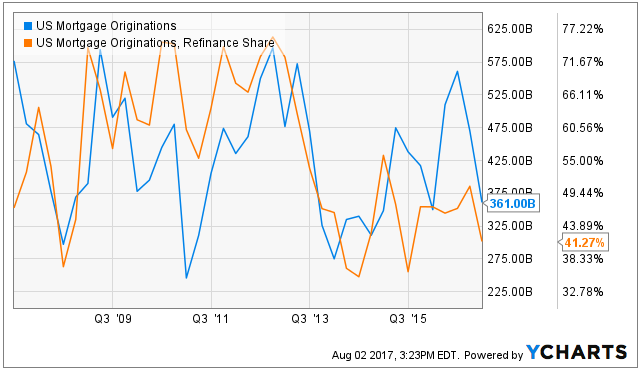

It is important for investors to understand, ELLI is highly dependent on mortgage originations (both purchases and refinances), and Ellie Mae’s CEO believes originations are at a low point but will normalize resulting in resumed high growth for Ellie Mae.

For perspective, the following chart shows current and historical US mortgage originations, including the share attributable to refinancing.

According to Elli Mae CEO, Jonathan Corr:

“The mortgage market is in the process of transitioning from a refi centric one to a purchase driven one. Some of our customers experienced closed loan volume lower than we expected in the second quarter as they dealt with declining refi volume, while the tight housing inventory held back purchase volume. We also saw some enterprise customers, which comprise an increasing portion of our customer base, take longer to ramp on our platform than planned. These factors led to a lower closed loan volume than expected, so we are resetting assumptions for the year as the market completes this transition. Beyond this year, we expect the market to normalize and for our business to resume stronger growth.”

Why the Price Decline?

As described by CEO Corr in our previous quote (above), Ellie Mae recently lowered guidance for 2017 revenues, and the price of the shares declined sharply. More specifically, Ellie Mae reported Q2 EPS on July 27 of $0.51 versus consensus estimates of $0.53, and also reported Q2 Revenues of $104.1 million versus consensus estimates of $110.51. Further, ELLI now sees FY 2017 EPS of $1.47-$1.50, below analyst consensus estimates of $1.90. Further still ELLI sees FY 2017 revenues of $400M-$405M, far below last quarters FY 2017 guidance of $433M-$440M.

Why is Elli Mae Attractive?

Ellie Mae is attractive because it offers a highly valuable software solution with no real competition, a very large total addressable market (lots of room for growth), and the shares are on sale after last week’s conservative forecast by management that caused the share price to decline. If you are looking for an attractive “disciplined growth” stock that is currently on sale, Ellie Mae is absolutely worth considering after this big decline (it’s a small hiccup on the road to much bigger success and profits). We don't currently own shares of Ellie Mae, but we may initiate a position in our Disciplined Growth portfolio in the near future.