One of our favorite long-time members (HB from Texas) recently asked “If you had to pick two or three securities for primarily income, but good candidates for capital growth, which would they be?” He mused REITs, MLPs, preferred stocks and bonds. For your consideration, this article includes three blue chip ideas that we consider attractive right now because of their strong income, as well as their potential for healthy price appreciation to boot.

Before getting into the three ideas, it is worth noting there’s been a recent flight to quality. For example, as the market has been selling off this quarter, fearful investors have flocked to REITs thereby resulting in that sector positing strong returns versus the overall market, as shown in the chart below. For this reason, we have not included any REITs on our list (we do own REITs though, and you can view them here).

Instead, we have selected three blue chip ideas that are currently out of favor. Specifically, they are contrarian ideas because the market doesn’t like them at all right now, but we believe they have strong long-term prospects. Without further ado, here is the list…

1. Johnson & Johnson (JNJ), Yield: 2.7%

If you missed the news, JNJ shares were down about 15% on Friday, following a Reuters story that said the company knew for decades that its baby powder contained asbestos.

Johnson & Johnson almost immediately refuted the claim saying:

"The Reuters article is one-sided, false and inflammatory. Simply put, the Reuters story is an absurd conspiracy theory, in that it apparently has spanned over 40 years, orchestrated among generations of global regulators, the world's foremost scientists and universities, leading independent labs, and J&J employees themselves.. Johnson & Johnson's baby powder is safe and asbestos-free."

However, the damage had been done and the shares stayed down (~15% for the day). In support of JNJ, several prominent Wall Street firms came out and said the sell-off was way overdone. According to analyst Larry Biegelsen at Wells Fargo:

"Based on prior high-profile product liability cases in drug and device sectors, we believe any potential settlement should be manageable for JNJ… Even if all 11,700 talc cases settled for $280,000 per case (the highest per case settlement amount among the cases we've tracked), the total liability to JNJ would be $3.3 billion. With over $19 billion of cash and marketable securities at the end of the third quarter, we continue to see the talc litigation as manageable for the company."

About JNJ and Why it is Attractive: If you don’t know, Johnson & Johnson is a well-diversified healthcare company, and the business is exhibiting growth across its three operating segments: Consumer (+0.7%), Pharmaceutical (+19.9%), and Medical Devices (+3.7%). The groups represent 20%, 45% and 35% of total sales, respectively.

JNJ’s business has the ability to perform well in both good and bad market conditions because of its blockbuster drugs (Remicade and Stelara), its new pipeline drugs (10 in pre-registration), and its ongoing new medical devices (innovative contact lenses, less invasive surgical tools). This isn’t a company that’s going to grow 500% per year, but the business isn’t going to disappear either considering its many important contributions to the healthcare industry.

JNJ's free cash flow (operating cash flow less capital expenditures) is over 20% of sales, thereby allowing continuing long-term dividend growth, ongoing share repurchases, and acquisition opportunities.

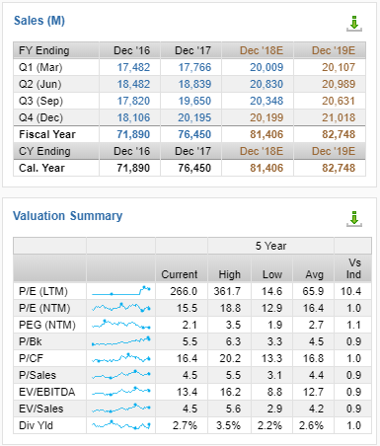

From a valuation standpoint, prior to Friday’s sell-off, JNJ sat near the middle of its historical range in terms of forward ratios including price-to-sales, EV-to-EBITDA, and price-to-earnings. However, after Friday it now sits near the lower end of the range for the same ratios. Plus its competitive advantages include high switching costs for customers in the device segment, and strong brand power from the consumer group.

JNJ Bottom Line: This is a strong business, with lots of cash and cash flow to cover the dividend, cover potential litigation, and to opportunistically buy back shares as well as keep re-investing in the business. The healthcare sector will grow, and JNJ will continue to be a leading contributor to that growth. The shares are attractively priced, especially after Friday’s sell-off.

2a. BlackRock Credit Allocation Fund (BTZ), Yield 6.9%

2b. PIMCO Dynamic Credit and Mortgage Income Fund (PCI), Yield 8.8%

If it is strong income you’re looking for, with the potential for a little price appreciation too, then fixed income closed-end funds may be worth considering for you. In the article linked below, we have highlighted two attractive closed-end funds (“CEFs”) that currently trade at attractive discounts to their Net Asset Values (thereby providing the potential for price appreciation), plus they pay big distributions to investors that are supported by a widely diversified portfolio of many individual bonds that are held in the funds. Very important to note, one of the CEFs focuses on investment grade bonds (BTZ) and the other holds mostly non-investment grade bonds (PCI). This is important because it means BTZ is more sensitive to interest rates, whereas PCI is more sensitive to credit spreads (i.e. the overall level of fear in the market). Said differently, PCI holds somewhat riskier underlying securities, but it also compensates for that risk with bigger distributions (income) paid to investors.

You can view all the latest metrics and numbers about these two CEFs (including there price discounts versus NAV) on Morningstar’s CEF Quick Rank, here…

And you can check out our recent detailed write-up (mostly on PCI, but it also has some details on BTZ), in this article: PCI: Attractive 8.6% Yield, But Know The Big Risks.

3. International Business Machines (IBM), Yield: 5.2%

IBM is one of the most hated stocks around, and that is a good thing for income-focused contrarians looking for some price appreciation too. For starters, IBM is hated because its revenue, net income and share price have been steadily declining for years…

However, there are two main reasons we believe IBM is worth considering if you are an income-focused contrarian looking for a little long-term price appreciation too:

IBM’s Backlog of Legacy Business will support the big dividend for many years. Specifically, IBM’s big ($120 billion) backlog and maintenance/outsourcing contracts give the company lots of cash flow for years to come. This is basically what has supported IBM’s big dividend over the years.

IBM’s recent Red Hat acquisition means the company is finally serious about revving up the growth engines. You can read the acquisition press release here: IBM TO ACQUIRE RED HAT, COMPLETELY CHANGING THE CLOUD LANDSCAPE AND BECOMING WORLD’S #1 HYBRID CLOUD PROVIDER.

To give you a flavor for IBM’s business, and why the share price has been lagging in recent years… IBM basically missed out on the huge secular trend to cloud computing that has basically fueled the growth for all of its competitors and peers in recent years. Companies across all industries are migrating data to the cloud, but IBM instead chose to keep living in the 20th century by supporting only onsite and hybrid-cloud solutions. The worldwide transition to the cloud has expanded very rapidly, and it has basically been leaving IBM in the dust. However, IBM’s recent acquisition of Red Hat is a small game changer, and creates the potential for some growth (i.e. share price appreciation).

To be clear, however, we are not expecting IBM to turn into a rapid growth company. Instead, it’s a strong cash flow and dividend company that now has realistic potential for some share price appreciation.

The share price of IBM declined sharply on the news of the acquisition, which is normally the case when a larger company acquires a smaller one (IBM’s market cap is currently $108 billion, Red Hat’s is currently $31 billion, and the acquisition is expected to be completed in the second half of 2019).

IBM is not a top-rated growth stock, but of the 23 Wall Street analysts covering the firm, they believe the stock should be trading at over $154 per share, thereby giving IBM 28.8% upside versus it’s current price.

Conclusion:

If you are looking for strong income, with the potential for some price appreciation, Johnson & Johnson, IBM and select fixed-income closed-end funds (e.g. BTZ and PCI) currently present attractive opportunities. In fact, we currently own all three. And for reference, you can view all of our current holdings here.