In our view, EastGroup Properties (EGP) just go more attractive, and we continue to own this 3.6% yielding REIT in our Income Equity portfolio...

EGP has sold off 9% since September 28th as it got caught up in the indiscriminate selling across the REIT sector (REITs were overheating this year and have recently pulled backed sharply). We believe now is a decent time to add shares if you don’t already have a position. Specifically, the valuation is attractive, the dividend is well-covered (and growing), and the business is relatively stable.

About EGP:

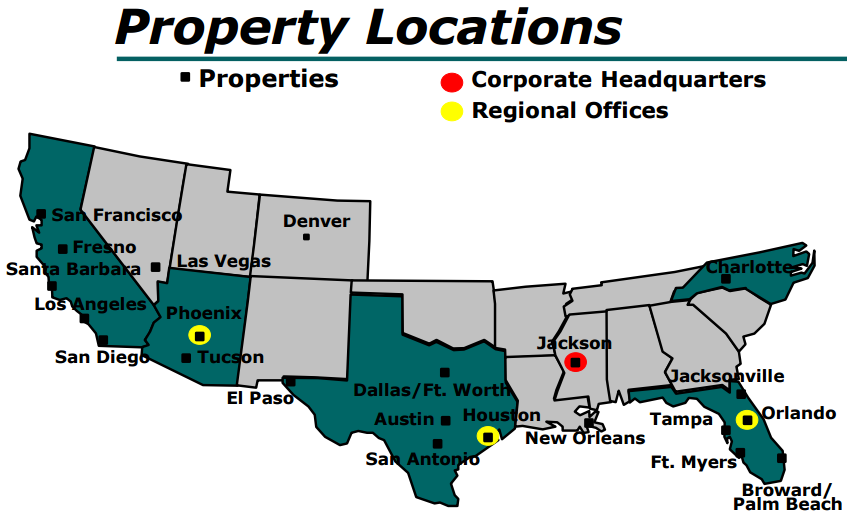

EastGroup Properties is an equity real estate investment trust (REIT) focused on the development, acquisition and operation of industrial properties in various Sunbelt markets across the United States (as shown in the following map). EGP provides functional, flexible and business distribution space for location sensitive tenants primarily in the 5,000 to 50,000 square foot range. The Company owns approximately 320 industrial properties and an office building.

According to EastGroup, some of the main benefits of Industrial Real Estate are stability, limited capital requirements, lack of obsolescence, and flexibility. EastGroup also makes clear they compete on location, not on price. The company believes their attractive locations help protect it during market downturns.

EGP’s Dividend:

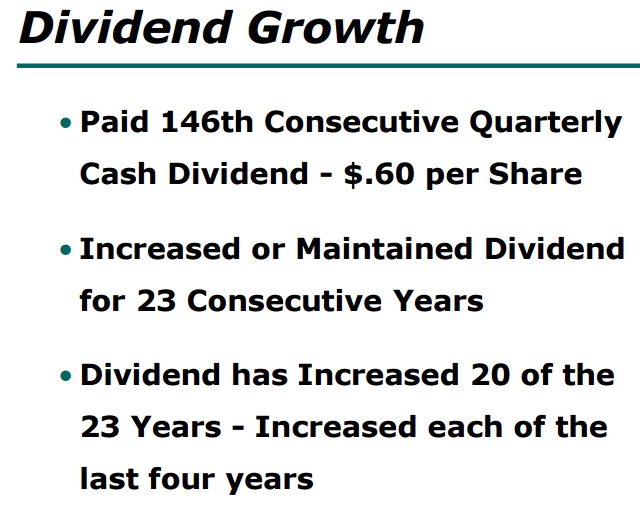

As shown in the following graphic, EastGroup has paid 146 consecutive quarterly cash dividends, and the company has increased or maintained the dividend for 23 consecutive years.

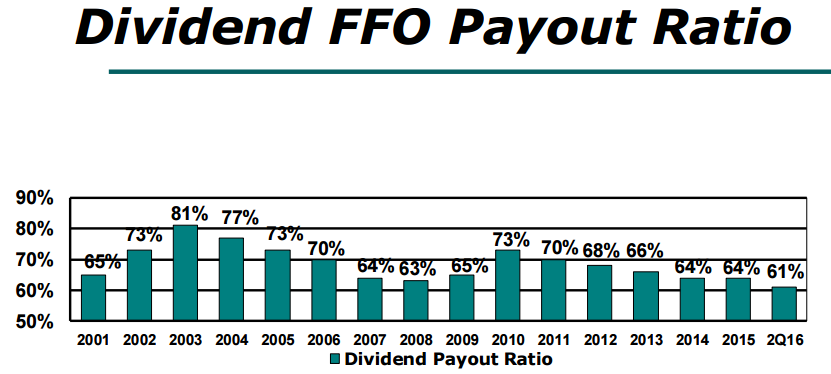

The following chart helps demonstrate the strength of EGP’s dividend considering the company has a fairly low dividend payout ratio (this is a sign of dividend strength and safety).

(Note: FFO stands for funds from operations, and it is a common REIT valuation that adjusts for property dispositions to give a clearer picture of earnings power).

Worth noting, EGP just announced another dividend increase on September 1st (paid on September 30th).

Valuation:

From a valuation standpoint, EGP’s recent 9% price decline has made it more attractive. For example, its price to FFO ratio has fallen from nearly 20x (19.9x) two weeks ago to only 18.0 now. For perspective, the following chart shows where this FFO multiple has stood in recent history:

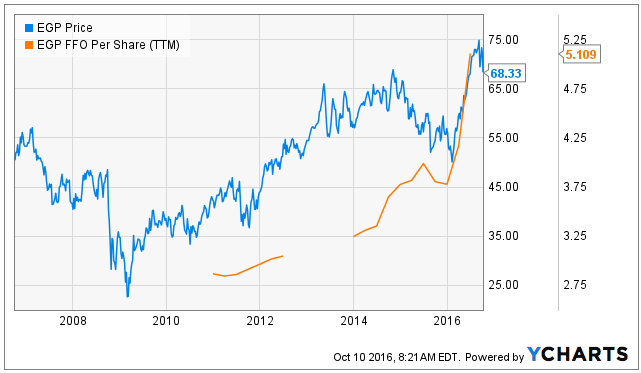

And for added perspective, here is a chart of EGP’s historical price and FFO per share:

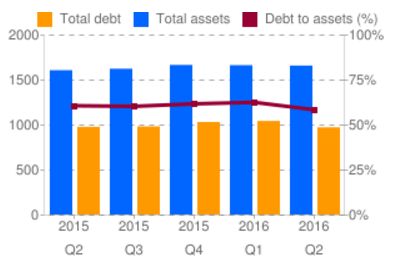

Also worth noting, EGP’s debt level is reasonable and not growing as shown in the following chart:

Conclusion:

We like EGP because of its recent price decline, attractive valuation, stable business and big dividend. We continue to own it in our Income Equity strategy, and we believe now is a decent time to consider adding shares. You can read our original EGP Thesis here.