Paylocity (PCTY) has negative net income, and a forward price-to-earnings ratio (91.4x) that would make most value investors shriek! However, it has also been experiencing “hyper” revenue growth that is hard to ignore. This article reviews Paylocity’s hyper-growth in five charts, and then provides our views on whether this Arlington-Heights-Illinois-based, zero-dividend-paying company, is worth considering.

Paylocity is a cloud-based provider of payroll and human capital management (HCM), software solutions for medium-sized organizations. The company's services are provided in a software-as-a-service delivery model utilizing its cloud-based platform. It is arguably a better and cheaper solution than those provided by the big boy on the block, ADP (you can read more about this in our previous Paylocity reports, here). However, before diving in head first, there are some jaw-dropping Paylocity metrics that are worth considering.

The first two charts (below) are more than enough to make most value investors run and hide. For starters, Paylocity’s net income is negative, and it has been for a while…

This next chart shows Paylocity’s forward price-to-earnings ratio (91.4x is obscenely high and unattractive to most value investors)…

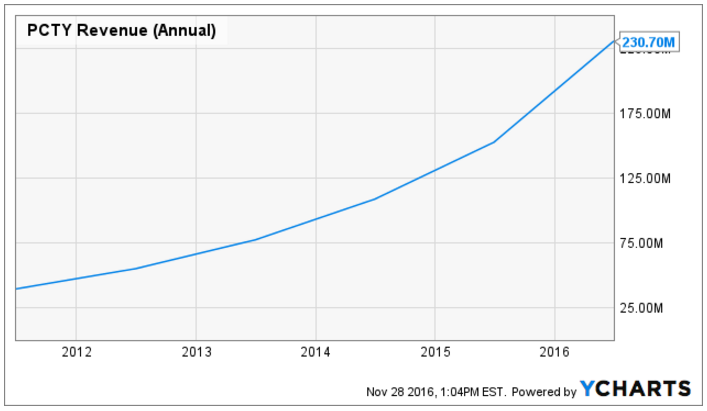

However, if Paylocity has one, over-riding, redeeming quality, it is its “hyper” revenue growth as shown in the following chart…

However, as shown in this next chart, what good is hyper revenue growth if expenses (in particular, Selling, General & Administrative expenses) are growing almost equally as fast?

And the market seems to agree with this negative sentiment as the price has fallen sharply this month as shown in this next chart…

The main reason the shares fell is because Paylocity lowered its earnings-per-share guidance for next quarter, below analyst expectations. Specifically, during its November 3rd earnings announcement…

"Paylocity Holding sees Q2 2017 EPS of $0.01-$0.03, versus the consensus of $0.04. Paylocity Holding sees Q2 2017 revenue of $66-67 million, versus the consensus of $68 million."

However, Paylocity still reported better than expected EPS, and provided strong full-year 2017 guidance….

"Paylocity Holding (NASDAQ: PCTY) reported Q1 EPS of $0.07, $0.04 better than the analyst estimate of $0.03. Revenue for the quarter came in at $65 million versus the consensus estimate of $63.58 million."

"Paylocity Holding sees FY2017 EPS of $0.36-$0.40, versus the consensus of $0.37. Paylocity Holding sees FY2017 revenue of $296-298 million, versus the consensus of $296.2 million."

However, as we’ve written before, what makes Paylocity so very attractive is that its revenue is sticky (i.e. once they’ve gained a customer, they keep that customer—attrition is very low). For example, as reported in Paylocity’s latest earnings release…

"Total recurring revenue was $62.6 million, representing 96% of total revenue."

High customer retention (combined with hyper-sales-growth) is the “magic” of Paylocity (i.e. it’s why investors are willing to bid up the forward P/E so high). Specifically, Paylocity is spending heavily on SG&A expenses to capture new customers now, but eventually SG&A expenses will stop growing so rapidly (and will actually may decline), the customers will stick with Paylocity (switching costs are high), and Paylocity will essentially become an enormous "cash cow." We’ve written about this multiple times in the past: Historical Paylocity reports and updates.

In a nutshell, we are drinking the Paylocity Kool-Aid, and the recent sharp price decline on this volatile stock makes now an attractive entry-point for long-term growth-oriented investors. We own Paylocity in our Blue Harbinger Disciplined Growth portfolio, and (as long as the business model doesn’t change dramatically) we expect to continue owning Paylocity for many years to come. Not only will sales and profitability grow (and it will likely eventually become a "cash cow"), but it will eventually become the target of bigger acquiring companies at which point it would be acquired at a very healthy premium (i.e. shareholders would be rewarded handsomely). We own Paylocity in our Blue Harbinger Disciplined Growth portfolio.