This week’s Blue Harbinger weekly reviews where we are in the market cycle, which sectors tend to perform best in each phase of the cycle, and finally we review a specific investment opportunity for members to consider.

The above chart shows which stock market sectors tend to perform best across each phase of the market cycle. And judging from the continued strong performance of technology stocks, for example, it feels like we continue to be in the early phase of the market cycle recovery (especially considering interest rates remain low an inflation hasn’t yet gotten of control.

However, with more interest rate hikes on the horizon, and many investors worrying market valuations have gotten a little ahead of themselves, the market cycle could be shifting. For example, high yield bond spreads widening last week, which is often a sign of market sentiment changes.

In addition to the market cycle, there are shorter-term market moves based simply on a “flight to quality.” For example, when fear is high, riskier stocks pullback more than safer ones. An even more specific example, is stock specific fear. When fear is high, individual stock prices pull back, and this can create some very attractive entry points. This week, we share one such stock, which happens to be in the healthcare sector, and its share price pulled back sharply just this past week on concerns over some of its operators. Without further ado, here is the stock idea…

MedEquities: 7.8% Yield – Are You Buying This Dip?

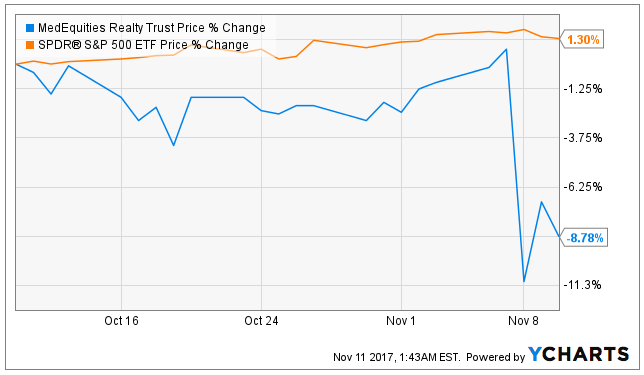

MedEquities (MRT) is a healthcare REIT that pays a 7.8% dividend yield, and despite this week’s earnings beat and guidance raise—the shares just sold off significantly, and the price to AFFO ratio is interesting. The following paragraphs review the attractive qualities of this relatively new and growing REIT. And we also highlight some of the risks, including exactly why the shares sold off. Finally, we offer our views on whether investors should consider buying this dip.

Overview:

MedEquities Realty Trust, Inc. (MRT) is a real estate investment trust (“REIT”). The Company invests in a diversified mix of healthcare properties and related real estate debt, focusing mainly on “higher acuity” properties (i.e. skilled nursing facilities and acute care hospitals) spread across the US, as shown in the following graphic.

Higher-acuity healthcare facilities are generally considered riskier investments than other healthcare properties because the constant pressure on insurance reimbursements rates under Affordable Care Act put pressure on the companies leasing these properties (i.e. the operators). And compounding these risks is the fact that MedEquities has a relatively small amount operators (i.e. concentration risk).

Despite the general riskiness of operators in this space, MedEquities has been growing profitable since the company was founded in 2014 and since its IPO in October of 2016. Specifically, debt levels remain low (as of 9/30/17, net debt to gross asset value was only 32.9%, and the ratio of net debt to consolidated adjusted EBITDA for the quarter annualized was a conservative 3.7 times), the dividend payout ratio is very conservative (management just announced it is only 73%, down from the 79% at its IPO), and the company continues to steadily make new investments that contribute to the growth in Adjusted Funds from Operations (“AFFO” has grown 11% since the IPO approximately 1-year ago).

Adding to the attractiveness of the company, just this week it increased the midpoints of guidance ranges for the full year 2017 from what was previously published. Specifically, net income increased from a midpoint of $0.63 to a new range of $0.64 to $0.65. And FFO increased from a midpoint of $1.10 to be $1.12. Further, AFFO increased from a midpoint of $1.12 to $1.13.

Further still, the company is still on track to meet its annual assumption of $150 million in investments for 2017 (and the cash yields on new investments remain attractive at 8.5% to 9%).

For your reference, we wrote about MedEquities in detail last April, and you can read that write-up here: MedEquities Realty Trust: An Attractive 7.2% Yield. Comparing the graphics in that report versus this report shows the company has been making progress on growing its investments, and diversifying its operator concentrations.

Also worth noting, MedEquities was fortunate in that the hurricane in Texas did not damage any of its current facilities. However, it did prevent a couple of opportunities the company was planning on, to fall out of the pipeline indefinitely (because the sites were literally under water). Nonetheless, MedEquities remains on target for its $150 million in new investments for 2017.

However, despite the many attractive qualities of this REIT, the shares declined over 9% after earnings were announced this week.

The Reason for this Week’s Big Share Price Decline:

The reason shares of MedEquities declined sharply following this week’s quarterly earnings announcement is because a portfolio of 10 skilled nursing facilities in Texas (which are leased to GruenePointe, and account for 24% of MedEquities’ total revenues) violated lease covenants.

Specifically, for the quarter ended June 30, 2017, the trailing 12 month EBITDAR and fixed charge coverages slipped 1.06 times and 0.9 times respectively, below the covenant levels of 1.2 times and 1.1 times.

However, it’s very important to note two things: (1) this operator has consistently paid rent in full and on time each month, and (2) management believes this is not a systemic problem that cannot be fixed, but rather it’s an operating management problem, and the company has taken steps to rectify the situation (including replacing several members on the operator’s management team, and focusing more on long-term growth than short-term cost cutting).

Further, the 24% of MRT’s total revenues that this operator represents will be 20% by year end as MRT continues to grow its investments (and is expected to be even lower in 2018 as MedEquities continues to use its dry powder to make more new investments).

Also important to note, MedEquities expects to grant a covenant waiver for the coverage ratios for 12 to 18 months, while the aforementioned initiatives (e.g. new management, and a more long-term focused strategy) bring about expected improvements over time.

Yet another important thing to keep in mind, the majority of MedEquities’ operators continue to deliver steady performance. And MedEquities continues to closely monitoring the operating performance of the portfolio that violated financial covenants.

Valuation:

The following chart shows MedEquties’ price to AFFO ratio compared to other healthcare REITs.

The companies in the chart are all healthcare REITs, but they have varying exposures across the acuity spectrum.

The market has generally been perceiving higher risk (related to healthcare reform and insurance reimbursement rate pressure on healthcare REIT operators) and assigning lower valuations to skilled nursing facilities operators such as Omega Healthcare Investors (OHI) and MRT. However, MRT has less legacy assets considering it was formed in 2014 (and IPO'd in late 2016), which means the company owns more high-quality healthcare real estate.

And trading just under 10 times 2017 AFFO (as shown earlier) is very cheap, in our view. And worth noting, Omega Healthcare is trading at an even lower valuation multiple, but that company continues to face challenges and risks from its tenant/operators (for example, see: Omega Healthcare down 6.4% after tenant troubles).

Conclusion: Is MedEquities Worth Investing?

If you are an income-focused investor, we believe MedEquities is worth considering for an investment, but only within the constructs of a diversified investment portfolio.

MedEquities is a risky company considering its operator concentration (even though diversification is improving, as described earlier), and considering it operates within the higher acuity healthcare space (also riskier, as described earlier).

However, we also believe the rewards outweigh the risks, considering MedEquities' low price-to-AFFO valuation, the company’s continued growth trajectory, its strong balance sheet, and because the operator that violated debt covenants continues to make lease payments and is expected to improve its operations going forward.

We do not currently own shares of MedEquities, but we do believe this week’s price decline makes the shares particularly more attractive and worth considering.

All of our current holdings are available here.