This week’s Weekly reviews an attractive +7% yield MLP that is on sale. We also review two growth stocks that we own in our Disciplined Growth portfolio. The MLP is very hated (and misunderstood) right now (which is why we like it), and the growth stocks have both rallied hard this year (they’re up 30% and 47%), and we share our views on how to play them going forward.

1. Enbridge Energy Partners (EEP), Yield: 7.7%

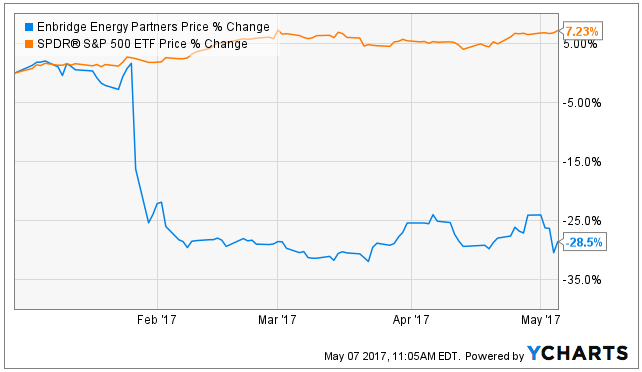

For starters, the MLP is Enbridge Energy Partners (EEP). And as the following chart shows, the markets is not happy with the company lately (its price is down 28.5% this year).

If you don’t know, EEP operates a portfolio of crude oil and natural gas pipeline systems. The crown jewel of the portfolio is EEP’s long-term deals with Canada’s Lakehead system, which generates lots of steady revenue to support juicy distributions to investors. EEP also operates natural gas infrastructure in Oklahoma and Texas, but in areas that have less favorable economics compared to other premier basins. In fact, it is these less economical regions that have cause EEP to cut its distribution, and subsequently caused the price to plummet as shown in our earlier chart. As a result, EEP is a very hated MLP right now.

In addition to being hated, EEP is also misunderstood, and these are the two reasons why we believe it is an attractive investment opportunity. The company is misunderstood because despite the distribution cut, the Canada Lakehead system contracts continue to be stable cash flow generators that are fairly unrelated to commodity prices. The distribution as it stands right now is very safe (supported by the Lakehead system), and the Oklahoma and Texas infrastructure provide upside if economics improve. We make no attempts to predict the future prices of commodity prices or supply/demand, but if the economics do not improve EEP will be fine, and f economics do improve EEP will be even better. If you are an income-focused investors, the 7.7% distribution is safe and worth considering for an allocation within your diversified long-term investment portfolio.

2. Facebook (FB), Yield: 0.0%

Facebook has been an absolute juggernaut in the lucrative world of online advertising. The company’s gigantic user base and quality collections of user information has allowed advertisers to target users, and they’ve been paying Facebook handsomely for it. Further, Facebook’s initiative to move into mobile-advertising (smart phones) has been widely successful and now exceeds desktop advertising revenues significantly. The big question though, can Facebook keep growing at a rapid pace or is it destined to slow down?...

…the answer, of course, is that it cannot grow at such a rapid pace forever, especially considering its market capitalization of $433 billion makes it larger than many entire countries around the world. Of course Facebook can get bigger, but it’s not going to grow at the same pace… And the market knows it, considering Facebook’s price-to-earnings ratio (relative valuation) has come down while it’s earnings (net income) has continued to grow, as shown in the following chart.

Said differently, even though the share price has continued to increase (as shown in the following chart) it’s not as expensive (relative to earnings) as it was.

Also, Facebook does have continued growth opportunities from growing and improving advertising revenues. It can also grow from new initiatives like applying artificial intelligence technology and the launce of virtual reality initiatives like Oculus rift.

Overall, in our view, Facebook is NOT overpriced, it has more upside growth, and we will continue to own the shares in our Blue Harbinger Disciplined Growth portfolio, despite the shares recent (and continued) strong gains.

Perhaps worth noting, we have owned our Facebook shares since purchasing them at $27 back in 2013. Our only sale of Facebook shares so far, was when the shares first doubled for us (from $27 to $54) we sold half of our position, and we’ve just been letting our profits ride (we’re playing with the houses’ money), and we believe Facebook has more long-term growth ahead. We have no plans to sell Facebook.

3. Paylocity (PCTY), Yield = 0.0%

Our third investment idea (also owned in our Disciplined Growth portfolio) is Paylocity. Paylocity is a cloud-based provider of payroll and human capital management (HCM), software solutions for medium-sized organizations. And the shares were up another 9% Friday (47.58% year-to-date) after a very positive earnings announcement.

Our thesis on Paylocity has remained the same since we purchased shares in 2015: The company continues to spend heavily on growth now because the business is “sticky” (once a company implements its HCM program, it’s unlikely to switch). Eventually, Paylocity will stop spending heavily on growth and will turn into an enormous cash cow (i.e. high revenues and low expenses). Alternatively, it may eventually be purchased by a larger company (such as ADP) at which time Paylocity shareholder will be compensated with a very healthy premium.

Paylocity, experienced a bump in the road after the November election because a portion of its business has been tied to implementing the Affordable Care Act (the market feared “repeal and replace”). However, aa complete repeal seems increasingly unlikely, and this is only a small portion of PCTY’s business anyway.

Without question, PCTY has been a volatile investment as shown in the following chart.

However, as a long-term investor, we’re comfortable with the volatility because we believe the long-term upside is great. Specifically we plan to keep holding our shares.

If you don’t currently own shares, and you’d like to, but you’re scared to purchase right after the big price gains so far this year, then you may want to consider selling put options. Specifically, you can sell June 2016 puts with a strike price of $40 per share, and receive a $0.40 premium (income) now that you keep no matter what, and you get to buy the shares at an significant discount ($40 per share) if the share price falls below $40 before the option expires next month, as shown in the following table.

This is a strategy we have implemented in the past (our previous put options expired unexecuted, so we just kept the income instead of buying more shares).

Overall, Paylocity is an attractive (albeit volatile) growth stock with significant long-term upside potential. As patient long-term investors, we plan to keep owning it in our Blue Harbinger Disciplined Growth portfolio.

And as a reminder, you can view all of our current holdings here.