Apollo Commercial Real Estate Finance (ARI), Yield: 10.2%

Apollo is a Mortgage REIT that is catching the eye of many income-focused investors because of its big yield (10.2%) and recent price decline (-6%) since June. This article provides an overview of the company, reviews the challenges and opportunities it faces, and then concludes with our views on whether or not it’s a good investment.

Overview:

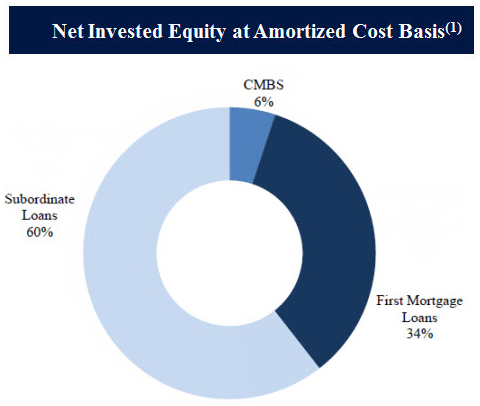

Apollo manages a diversified investment portfolio with a total amortized cost of $3.6 billion, including first mortgage loans, subordinate loans and commercial mortgage backed securities, with an overall weighted average loan to value of 64%.

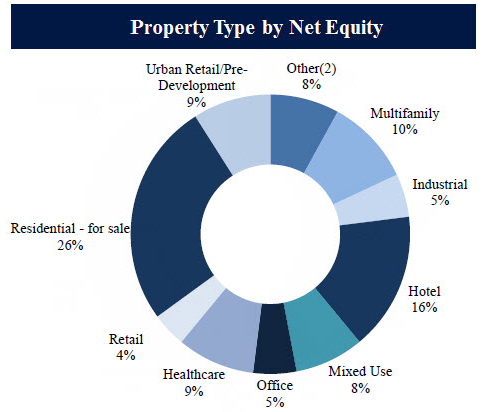

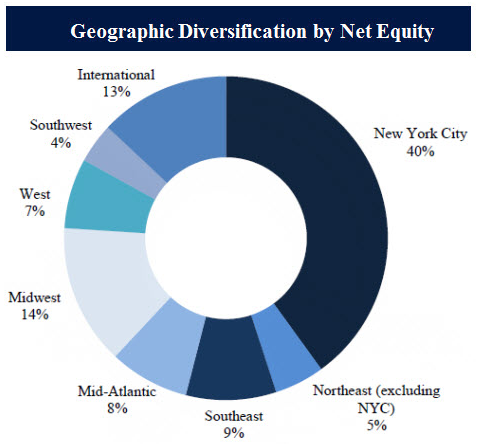

Apollo’s investments are diversified across property types and geographies, as shown in the following graphics.

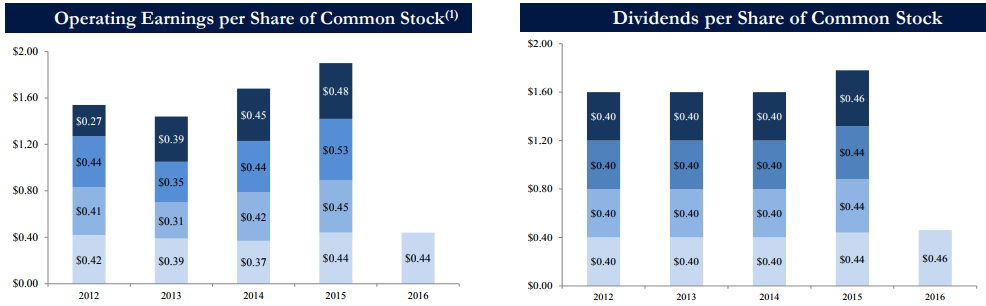

Also, the portfolio’s fully levered weighted average IRR is 13.3%, with a weighted average term of 2.8 years, and 90% of the loans have floating interest rates. And for perspective, the following graphic (from the company’s most current investor “fact sheet” shows that operating earnings have been covering the dividend in recent years.

And more recently operating earnings per share was $0.46 in Q2 2017 versus a dividend of $0.46 per share.

Apollo's Positives:

Apollo currently has a variety of good thing going for it. For example:

Diversified Portfolio: As shown in our earlier graphics, Apollo’s investments are well-diversified across property types and geographies. This helps reduce risks. For example, if one sector of commercial real estate is performing badly (for example, “office”) then the company’s exposure to other sectors (e.g. industrial, multi-family or healthcare, to name a few) can help minimize the risks.

Commercial Real Estate is Strong: According to the SIOR Commercial Real Estate Index, commercial real estate (the market Apollo invest in) is currently very strong (especially on the east coast where ARI has a concentration of investments) as shown in the following chart.

First Lien Mortgages: Another positive thing Apollo has going for it is that a significant and growing portion of its investments are in first lien mortgages. For example, per our earlier chart, 34% of the company’s investments are in first lien mortgage. This compares favorably to other mortgage REITs that are almost exclusively subordinated debt. Further, as the following table shows, the company’s recent Q2 investments have been heavily weighted toward first lien.

Attractive IRR: the fully levered internal rate of return (“IRR”) on ARI’s investment portfolio is 13.3%. This is a very attractive return, and it gives the company room to operate efficiently and support a high dividend payout to investors. Also, new investments in Q2 had a weighted average IRR of 15%, which is encouraging.

Conservative Capital Structure: Currently, ARI’s debt-to-equity ratio is 1.0x. This is a relatively low level of leverage, and it gives the company financial flexibility to take advantage of the most attractive new investment opportunities in that arise.

Low Loan to Value: Another attractive characteristic of ARI’s investment portfolio is its low loan to value, currently only 54%. This is an indication of lower default risk because investors are far less likely to walk away from properties when they have significant equity in them.

Floating Rate Loans: Approximately 90% of the loans in ARI’s investment portfolio are floating rate loans. This positions the company well for a rising interest rate environment. However, the weighted average life of the loan portfolio is only 2.8 years. This means they’ll get some benefit from rising rates during this time, but also have capital freeing up in the future when interest rates are expected to be higher (this is a good thing for ARI’s net interest margins). For perspective, Apollo estimates that every 50 basis point increase in LIBOR would increase net interest income per diluted share of common stock by approximately $0.09 on an annual basis.

Price Pullback: The price ARI shares has pulled back 6% since mid-to-late June, which makes for a more attractive entry point in the eyes of some contrarian investors. Also, the company’s price-to-book value is reasonable, and it has decreased since last quarter. For example, the company’s book value per share of common stock was $16.16 at June 30, 2017, as compared to book value per share of common stock of $16.05 at March 31, 2017, whereas the share price was $18.81 on March 31 (i.e. a 17.2% premium price to book value) versus $18.07 now (i.e. an only 11.8% premium price to book value).

Opportunistic Management Team: One of the benefits of being an mREIT investing in mortgages (versus a bank investing in mortgages) is that an mREIT can be more opportunistic (banks are hamstrung by tight risk management guidelines and rules). For example, in August of 2016, ARI acquired AMTG for 89.25% of AMTG’s book value, and in connection with the transaction, ARI issued 13.4 million shares of common stock at an 8% premium to ARI’s book value per share. ARI may likely be able to identify more attractive opportunistic investments in the future, especially considering its low current level of leverage.

Apollo's Negatives:

In addition to the positives, there are also multiple “negatives” to investing in Apollo that investors should be aware of.

External Management Team: Apollo is managed by an external management team, ACREFI Management, and there are conflicts of interest in the relationship. For example, according to Apollo’s annual report:

There are various conflicts of interest in the [management] company’s relationship with Apollo which could result in decisions that are not in the best interests of the company’s stockholders.

Troubled Assets: According to the latest quarterly earning conference call, the company is currently dealing with two (arguably three) troubled investments. For example, last quarter, ARI recorded a $5 million provision for loan losses and impairment against a $49 million investment in a newly constructed 50 unit condominium project in Bethesda, Maryland.

Also, ARI continues to work through a challenging property is New York at 111 West 57 Street, commonly known as the Steinway building.

Further still, during the latest earnings call, ARI management commented that “the only other transaction that we’re spending a lot of time from an asset management perspective today is, a retail loan in suburban Ohio, that is commonly known as Liberty Center.”

In aggregate, these challenged investments make up a small portion of the overall investment portfolio. Some challenging situations are usually inevitable, the market price already reflects the situation, and the company is working through it.

Market Conditions Are Changing: As we mentioned previously, commercial real estate investment conditions are currently strong, however that can change quickly. For example, according to ARI’s annual report: “Current economic climate remains very favorable for ARI’s business model. 2017 is a peak year for commercial real estate loan maturities, with close to $400 billion of loans maturing.” This creates a lot of opportunities for ARI this year, but considering 2017 is a “peak year,” it also implies there will be less market-wide opportunities going forward. For reference, here is a look at commercial real estate debt maturities in the recent past and going forward.

Conclusion: Should You Invest In Apollo?

Overall, Apollo faces a variety of risks and opportunities (as described above). We believe that the “positives” outweigh the “negatives” for Apollo, but it is still a very risky company. Specifically, we believe Apollo has the financial wherewithal to support the dividend for now (operating earnings were $0.46 per share last quarter, and so was the dividend), and the company’s continuing new investments will help support the dividend going forward (the IRR on new investments last quarter was 15%).

Further, Apollo’s relatively low level of leverage and it’s high quality investment portfolio will allow its management team to take on new types of investments (perhaps more risky, if needed) to continue to support the dividend going forward.

If we could only own one stock, it probably would NOT be Apollo because it is too risky, but within the constructs of a well-diversified income-focused investment portfolio, Apollo is worth considering. We’ve added Apollo to our “watch list,” and for reference you can view all of our current holdings here.