This week's Blue Harbinger Weekly is a continuation of our free report, Top 10 Big Yield Ideas to Start 2018, but this version contains all the details for the Top 5. Without further ado, here are the top five...

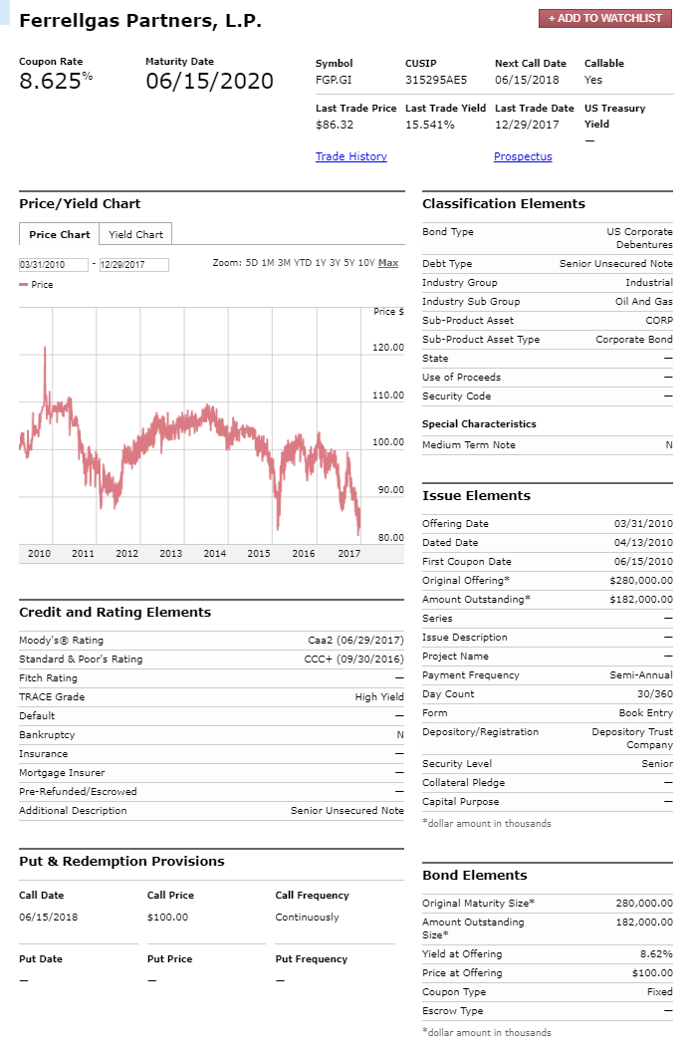

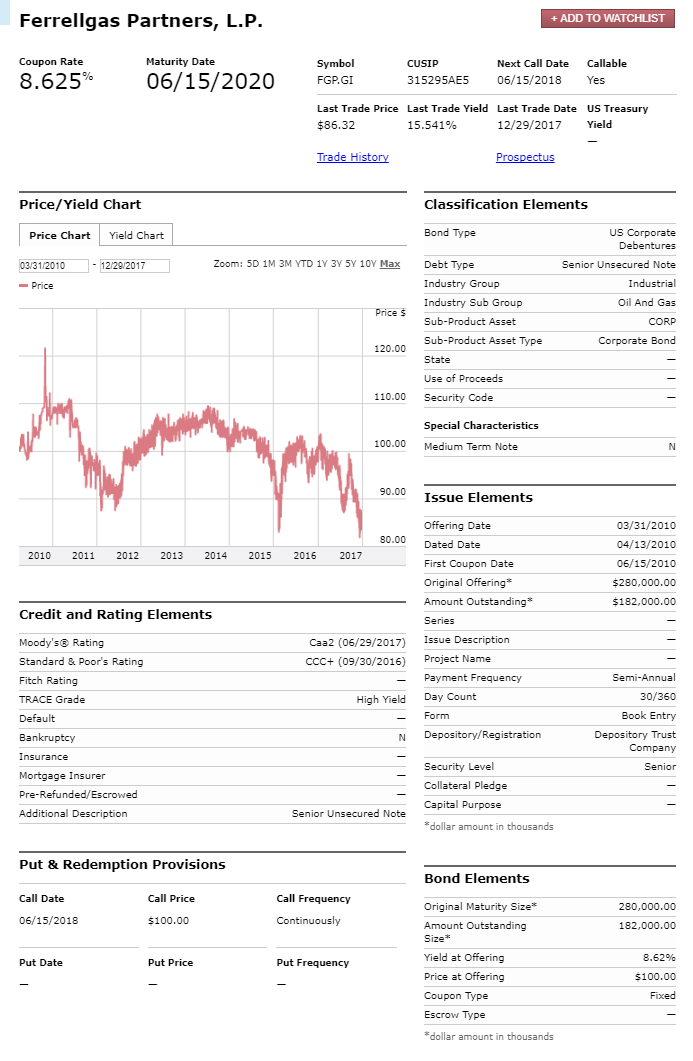

5. Ferrellgas (FGP) 2020 Bonds, Yield: 15.5%

Similar to AmeriGas, Ferrellgas is a retail marketer and wholesale provider of propane. However, unlike AmeriGas, Ferrellgas cut its big distribution about a year ago, the equity sold off, and the company has a very high debt load. Ferrellgas had been trying to expand its business to be less dependent on weather, and that’s what got it in trouble as the combination of expansive spending and warm weather proved too much, and that’s when they cut the distribution.

We’re still nervous about the equity, but we do own Ferrellgas bonds, and we’re excited about the recent spat of cold weather as it will improve cash flows for the company. Ferrellgas had been working to improve business by gaining customers through competitive pricing, and now with a more efficiently run business, improving customers, and more expected cold weather, we believe things are looking up for Ferrellgas, particularly these 2020 bonds.

{kind=link}

Overall, we believe the bonds are particularly attractively priced right now, and the income is very attractive too.

4. Omega Healthcare (OHI), Yield: 9.4%

If you’ve been waiting for a sell-off in this big-dividend healthcare REIT, you finally got it during the 4th quarter of 2017, and the shares continue to trade at an attractively low price, in our view. We wrote about the potential for this big sell-off during the 3rd quarter of 2017 in this report...

Essentially, Omega is facing challenges from several of its operators, as revealed during its disappointing earnings release back on October 30th.

Specifically, the shares were down after the company missed earnings estimates and reported troubles with one of its health care properties, Orianna Health Systems. Orianna has been placed on a cash basis, and Omega is in discussions regarding moving some or all of the Orianna portfolio to new operators. Omega expects current annual contracted rent to fall once the transition is complete. However, getting this investment off the books may be the best thing for investors (in terms of maintaining a quality portfolio). Other REITs have successfully divested of troubled operators (e.g. Simon Property Group got rid of Washington Prime and HCP got rid of Quality Care Partners).

We continue to own shares of this big 9.4% dividend yield healthcare REIT in our Blue Harbinger Income Equity portfolio, and we believe it currently trades at a very attractive price if you’re looking to put more dollars to work.

3. Income-Generating Put Sales

Yield: 6.0% - 15%

Another attractive income-generating strategy we like to utilize occasionally is income-generating put option sales. This is a strategy where we sell out-of-the-money put options (to generate immediate income) on stocks that we'd like to own, especially at a lower price. If the price falls and the shares get "put" to us - we're happy to own them, and if they never get put to us then we're happy to simply keep the income we generated for selling the puts in the first place.

We generally find this strategy works best when short-term noise and fear are high because that's when the premium income is higher. For example, here is an income-generating options trade (put option sale) we’ve written about in the past:

We like to occasionally share this type of trade with readers, and please feel free to share feedback and ideas on the strategy.

2. Teekay Preferred Shares (TOO-B), Yield: 8.6%

Teekay Offshore Partners (TOO) is a provider of marine transportation, oil production, storage, long-distance towing and offshore installation and maintenance and safety services to the offshore oil industry.

We first wrote about the attractiveness of these preferred shares to members back in 2016 in this report:

However, the share price has been very volatile this year, and the current small discount to its “call price” ($24.85 vs $25.00) makes TOO-B very attractive, in our view.

Our thesis for these TOO-B shares is similar to our Tsakos thesis… the market is incorrectly extrapolating recent bad new, and missing the supply and demand market cycle forces that will drive this company’s value higher. We believe the preferred shares are attractive to income-focused investors because they pay a big dividend, and they are safer than the common.

For more perspective on the recent volatility, the market dramatically overreacted to bad news this summer (e.g. a cancelled contract by Petrobas, and a Morgan Stanley downgrade), and the shares sold off. However, the company has remained profitable, has significant cash flow, and can easily support the preferred share dividend payments (and can free up more than enough cash by cutting the common share dividend, if need be). Certainly there are risks (the market could turn south again), but the industry is recovering (demand continues to grow, and competition is lower as many firms have already filed bankruptcy). Teekay has plenty of financial wherewithal to keep supporting the preferred share dividends, and we expect the share price will rebound above par.

Overall, the preferred shares are cumulative, they’re ahead of the common in the capital structure, the company has plenty of financial wherewithal, they trade at a small discount (a good thing), and they’re not redeemable by the company until 4/20/2020. We believe TOO-B is attractive and worth considering if you are an income-focused investor.

1. Tsakos Energy (TNP), Yield: 5.1%

We wrote about the attractiveness of Tsakos preferred shares earlier in this report, but unlike the preferred shares, we do currently own the common shares. In addition to a big dividend, we believe Tsakos has significant price appreciation potential in 2018. The share price is currently trading lower thereby providing a very attractive entry point, in our view. You can read all the details on our Tskakos thesis in this recent members-only report:

Conclusion:

We believe all of the opportunities highlighted in this article offer an attractive risk-versus-reward opportunity for income-focused investors. Importantly, we ranked these opportunities from 10th to 1st, but we’d never put all our investment dollars in only one of these opportunities. We always invest via a diversified investment portfolio, and you can view all of our current holdings here.