“Investing is the only business I know that when things go on sale, people run out of the store” – Mark Yusko

If you are looking for high-flying aggressive growth stocks, this article is NOT for you. However, if you are an income-focused contrarian investor, you may want to consider the ideas presented in this article. In particular, you may have noticed that consumer staples stocks have been significantly lagging the rest of the market lately, and that’s often an attractive time to buy. For example, here is a chart with varying sector and style performance as of the end of April:

The Consumer Staples sector is down 11.13% this year ,whereas the S&P 500 is almost unchanged (-0.38%), and Consumer Discretionary, Information Technology, and Energy are all up. We could digress into the continuing momentum of growth stocks, and how value stocks (like staples) are due for a comeback (especially considering value tends to outperform growth over market cycles anyway), but this report is about Consumer Staples specifically.

Consumer Staples tend to be less volatile companies that can be profitable in good times and in bad. They also tend to pay attractive growing dividends. Arguably, Consumer Staples have been benefiting for decades as interest rates were moving lower thereby allowing these stable companies to lever their returns at low interest rates, refinance their debts at attractive lower rates, and even borrow money to buy back their own shares. One of the big questions now is has the sector sold off enough to warrant the risks of higher interest rates going forward? Another big question is do these companies have enough growth left to deliver returns that are attractive to investors? After all, low volatility dividend payers were an investor favorite not too long ago for their larger than average dividends and relatively low volatility.

We ran a screen for Consumer Staples companies offering at least a 2.5% dividend yield, and the results are included in the following table.

Three stocks from the list that we believe are worth considering, if you are a contrarian income-focused investor, are listed below.

Procter & Gamble (PG), Yield: 4.0%

If you don’t know, P&G makes things like shampoo, toilet paper, tooth paste and razor blades, to name just a few. And after years of strategic repositioning, P&G has recently completed its efforts to shed over 100 non-strategic brands; it’s arguably now a meaner, leaner, more potent company. And as you can see in the table above, the shares have performed terribly this year. And the recent share price decline is something that contrarian investors get excited about because they like to “buy low,” especially blue chip companies like P&G.

Procter & Gamble remains profitable, its dividend yield is large, and its products and services are not going away. The shares have sold-off because the sector has been out of favor, but also because the rate of recovery has been slower than expected following its strategic repositioning. Sentiment is negative, as analyst have been downgrading the shares, and this heightened negativity is often an attractive opportunity for contrarians. And despite the downgrades, the street still believes the shares are undervalued as shown in the following chart.

And with a forward PE ratio of only around 17, now is an attractive time to consider purchasing shares of Procter & Gamble.

We own shares of Procter & Gamble.

Kraft Heinz (KHC), Yield: 4.4%

The Kraft Heinz company manufactures and markets food and beverage products in the United States, Canada, Europe, and internationally. Its products include condiments and sauces, cheese and dairy products, meals, meats, refreshment beverages, coffee, and other grocery products. And to the delight of many contrarian investors, the shares have sold off over 26% so far this year, thereby creating a more attractive entry point for contrarian income-focused buyers.

Perhaps worth mentioning, Kraft Heinz is a Warren Buffett favorite as his firm, Berkshire Hathaway, owns about one quarter of the outstanding shares (3G Capital also owns about a quarter, as well). This is not surprising considering Buffett is famous for being a value investor, and the shares currently trade at an attractively low forward price to earnings ratio. The market also has strong growth expectations for the company, as shown in the table near the start of this report. Further, despite some recent downgrades, the street continues to believe the chares are significantly undervalued, as shown in the following chart.

The money flow index for KHC, as shown in our earlier table, sits at an extremely low 27. This is an indication of an oversold stock that is increasingly attractive for contrarians, especially considering EPS growth estimates remain very healthy for the foreseeable future (as shown in our earlier table).

Colgate-Palmolive (CL), Yield: 2.6%

Colgate-Palmolive is a low-beta staple company that produces products including toothpastes, soaps and laundry detergents, to name a few. This company’s shares recently sold-off following an earnings announcement that beat expectations, however fell short on revenue. The announcement caused the forward P/E ratio to sink, which is a good thing for contrarians considering the stability of this attractive blue chip company.

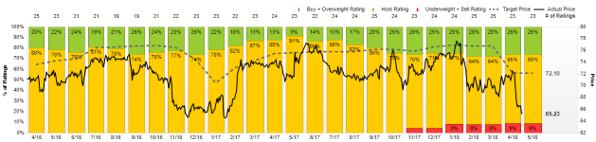

We view the sell-off as a buying opportunity, and the Street does too, as shown in the following price target chart.

Specifically, the Street maintains a price target of over $72, giving the shares over 10% upside in the near-term, and even more over the long-term, to go along with the steady 2.6% dividend yield.

And with plenty of free cash flow to keep supporting dividends and share buybacks, Colgate Palmolive is worth considering.

Conclusion:

As we mentioned in our intro, if you’re looking for more aggressive income-producing stocks, this article is not for you. However, if you’re looking for lower volatility and balance in your portfolio, then out of favor consumer staples stocks are worth considering for their healthy dividends and for their steady growth prospects. And for their sharply discounted prices