With earnings season for big-dividend Business Development Companies (BDCs) about to kick off in a few weeks, it’s worth reviewing high-level data on the group (i.e. 40+ Big-Yield BDCs) and Main Street Capital (MAIN) In paticular. We consider current price-to-book values (versus history), current market conditions (including how much credit spread risk is priced in) and the breakdown of historical returns (in terms of price gains versus dividend income). We conclude with which BDCs we currently like best (including the ones we own and the ones we are considering).

40 Big-Yield BDCs Compared

The following table is sorted by market cap (with industry stalwart Ares Capital at the top). It also shows the all-important dividend yield, as well as where the current price sits relative to the 52-week and 5-year price range, and the valuation metric price-to-book (plus current P/B versus 5-year range).

You likely recognize at least a few of your favorite BDCs in the above table, and we’ll refer to this data throughout this report.

Why BDCs are Special:

No Corporate Taxation: For starters, BDCs don’t pay tax at the corporate level as long as they pay out their income as dividends. This gives BCDs a big advantage over other companies, and this advantage was created by an act of Congress in the 1980’s because they wanted to make it easier for small businesses to thrive (BDCs provide financing and capital to small (middle market) companies).

Less Regulation: Another reason BDCs are special is because they are allowed to take on “risks” that traditional banks are not allowed to due to stricter regulatory rules (and reserve requirements) following the great financial crisis. Generally speaking, this enables BDCs to invest in attractive opportunities that traditional banks are not able to. This is amazing because (as you can see in our earlier table) some BDCs have actually outperfomed the market (e.g. the S&P 500 over the last 5 and 10 years) which is a lot more than you can say for other big-yield investment categories (such as bond closed-end funds and many REITs). It’s doubly amazing because the S&P 500 includes many top growers like the “Magnificent 7” megacaps (which have dominated market performance).

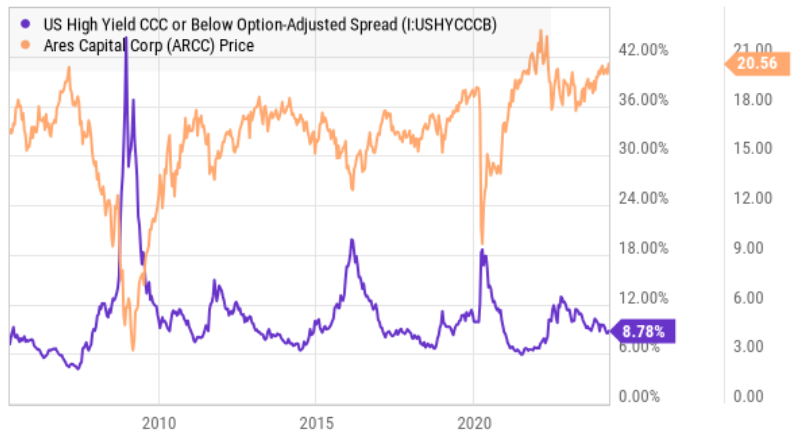

How Much Risk is Priced In:

To get an idea of how much current market risk is priced into BDCs we can look to credit spreads. Credit spreads are the difference in yield between low risk loans/bonds (such as US treasuries) and higher risk loans/bonds (such distressed debt and BDCs).

As you can see in the chart above (we’re using industry leader Ares Capital as a proxy), BDC prices tend to rise and fall with credit spreads, and the market is currently NOT pricing in too much risk (which can be an indication of subdued price returns going forward). Said differently, now may not be the best time to invest in BDCs if you are looking for strong price gains, however most people invest in BDCs for the big dividend income (as we describe in the next section). And to support this point, you’ll notice in our earlier chart that a lot of BDCs do NOT currently trade at big discounts to book value (instead they trade at small premiums versus history).

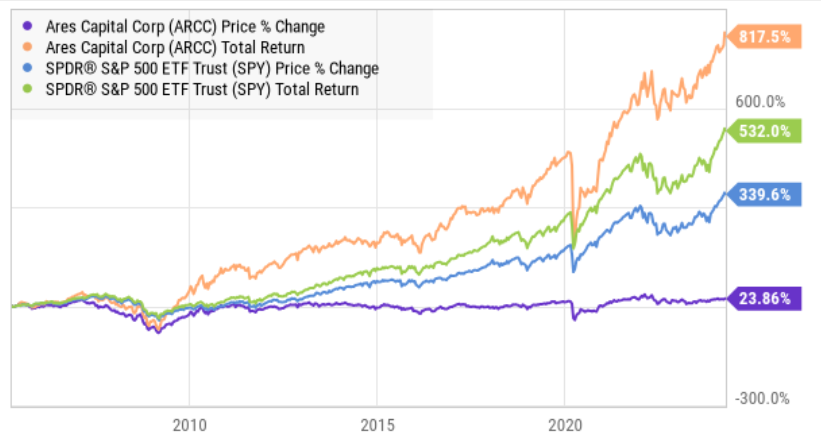

Historical Price Gains Verus Dividend Income

Sticking with Ares as an industry proxy, you can see that historically most of BDC returns have come from dividends NOT price gains (i.e. Ares’ price has been relatively flat over time, which means those big longer-term total returns have come from the big dividend payments—which is exactly what a lot of investors are looking for). Ares’ total return has easily beaten the S&P 500 over this time period.

Main Street Capital Is Special:

Main Street Capital is a popular BDC, and it is special for a few reasons.

Internally Managed: Main Street is internally managed (a lot of people like this because it has the potential to reduce expenses/fees and reduce conflicts of interest between shareholders and management).

Consistent Premium to Book: A lot of investors are afraid to invest in Main Street because it consistently trades at such a high price relative to book value (currently ~1.6x) as compared to other BDCs (see our earlier table). However, as you can see in the chart below, Main Street also has a strong history of delivering better price returns than a lot of BDCs.

So whereas Main Street’s dividend yield is low by BDC standards (6.1%), its price returns are high, and its total returns have been steallar (as you can see in our earlier table.

Growing Monthly Dividend: And Main Street also has a very stong history of growing the monthly dividend (to keep pace with the price gains over time). Only a handful of BDCs pay monthly (most pay dividends quarterly).

Exposure to Houston: Another thing we currently like about Main Street is that it is based in Houston where energy (oil) is a very big deal (and oil has recently been performing very well). This bodes well for Main Street’s business (even though they are diversified across many industries) because the local economy and opportunities are likely thriving to the benefit of Main Street.

On it’s previous quarterly earnings announcement, Main Street beat expectations on portfolio company strength, including:

Distributable net investment income of $1.12 per share, beating a $1.07 consensus estimate (and gained from $1.04 in the previous quarter and $0.98 a year earlier).

Total investment income was $129.3 million (beating the $127.6 million steet expectation, and rose from $123.2 million the previous quarter and $113.9 million a year earlier).

Main Street is set to announce earnings again on or around approximately May 2nd.

Conclusion:

Very rarely, BDCs will present attractive “buy low” opportunities (such as when ciedit spreads blow out—which is NOT the case right now). However, big dividends are the main show when it comes to BDCs, and the dividends paid by top BDCs are consistently high (and attractive if you are an income-focused investor).

Main Street looks particularly expensive on a price-to-book value basis as compared to other BDCs, but it’s not. Main Street consistently trades at a bigger premium because it consistently generates higher price returns (and offers a slightly lower (but still big) dividend yield).

MAIN’s lower yield can also be helpful if you own MAIN in a taxable account becuase BDC dividends are generally NOT qualified (meaning they don’t qualify for the lower dividend tax rate). Specifically, if you own Main Street in a taxable account it may be to your advantage to get more of your return from price appreciaton (because you control when the capital gains are taxed (i.e. when you sell) and those capital gains may be taxed at a lower rate (depending on your tax bracket). For reference, in 2023, approximately 8% of MAIN’s dividend was taxed as qualified and approximately 92% was taxed as ordinary income.

Overall, if you are are income-focused investor, BDCs remain attractive. They are NOT poised to deliever outsized price gains right now (they rarely ever are), but they are poised to keep paying big steady dividend income (which is exactly what a lot of income-focused investors want).

We are currently long shares of Main Street Capital (MAIN), Ares Capital (ARCC), Oaktree Securies Lending (OCSL) and Hercules Capital (HTGC).