This report reviews one of the largest and most diversified global Software-as-a-Service (“SaaS”) companies. The company has delivered strong performance in the recent quarter despite a turbulent period for the global economy. The increased rush for business digitalization and adoption of ‘work from home’ policies by global enterprises has improved the value proposition of the company’s product offerings further. Investors have taken cognizance of the tailwinds and the company’s strong business franchise as the stock has appreciated significantly this year. In this report, we analyze the company’s business model, the impact of COVID-19 on its business, competitive position, and finally conclude whether the the common stock still offers upside potential for “income via growth” investors.

Overview: Adobe (ADBE)

(for your reference, a PDF version of this report is available here).

Adobe is a multinational cloud-based software company that offers a diverse portfolio of products and services. Headquartered in San Jose, California, the company was incorporated in 1982. Its well-known product offerings include Adobe Sign, Acrobat, Photoshop, Lightroom, Illustrator, XD and Premiere Pro. The company is a global tech behemoth with nearly 23,000 employees. Geographically, Americas account for 58% of revenue, whereas EMEA and APAC region contribute 26% and 16% to the revenue respectively.

Adobe’s Share Price:

Adobe conducts its business through 3 operating segments:

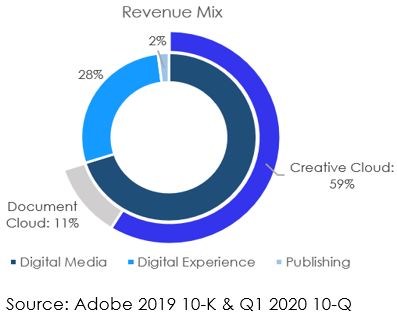

Digital Media: This is Adobe’s largest segment accounting for 70% of total revenue out of which ~84% comes from Creative Cloud while ~16% from Document Cloud. Creative Cloud is a subscription service focused on professionals in creative industries such as artists, designers, developers, photographers and marketers. Adobe offers them over 20+ creative applications with an option to buy software subscription on a standalone basis or subscription to the whole software bundle as a package. Besides applications, creative cloud also provides cloud storage facility as well as ability to create and customize creator’s portfolio websites thereby providing them seamless content sharing and opportunity to showcase their work. Document Cloud is a subscription service that allows users to create, view, edit, approve, sign, track, store and share documents across devices. Document Cloud primarily includes Adobe Acrobat DC, Sign and Scan. Customers include individuals, small businesses and enterprises.

In order to attract customers, Adobe’s pricing structure has been developed in such a manner that creators utilizing over 2 or 3 Adobe apps would tend to benefit more by purchasing entire bundle of over 20 applications. For example, Business plan for single app per license is ~$34 per month while complete bundle is available for ~$80 per month essentially incentivizing creators to purchase complete bundle. Moreover, subscription access to all creative solutions at one price also enables creators to explore Adobe’s new apps and tools that they have not used before. This results in further cementing of the relationship between users and Adobe. In fact, 2/3rd of creative cloud’s annual recurring revenue is derived from ‘All App’ subscribers now.

Digital Experience: Through this segment, Adobe offers a collection of integrated software solutions primarily targeting the advertising industry. Product offering includes analytics, campaign management, target advertising, content management and open source e-commerce platform. The segment accounts for 28% of total revenue. This segment also includes Marketo, a marketing cloud platform Adobe acquired in 2018 for $4.73 billion and Magento, an open source e-commerce platform acquired for $1.64 billion.

Publishing: This segment accounts for just 2% in total revenue and includes Adobe’s low growth, mature, legacy products and solutions. Revenue is generated from licensing these solutions to OEMs (original equipment manufacturers) of workflow software, printers and other output devices.

In addition, the company also owns a creative intelligence platform called Adobe Sensei which can integrate with company’s creative cloud, document cloud as well as experience cloud, and add more value for customers through incremental AI and machine learning capabilities.

As per the 2019 investor presentation, the company will have a total addressable market of over $128 billion in 2022 that comprises of $31 billion Creative Cloud TAM, $13 billion Document Cloud TAM, and $84 billion Experience Cloud TAM. While the company has already penetrated ~20% of creative cloud TAM, the Document and Experience Cloud segments have only been penetrated ~10.5% and ~4% respectively.

COVID-19: Pros outnumber Cons

COVID-19 led shutdowns have taken their toll on commercial activities globally, however, the adverse impact on Adobe has been limited to its advertising cloud business because of the decline in advertising spend by global enterprises. Adobe expects to generate $200 million in advertising revenue in FY20 which represents an anticipated YoY decline of almost 45%.

“As we saw the extent of the global decline in advertising spend, we made the strategic decision mid-quarter to cease pursuing transaction-driven Advertising Cloud deals. Together this resulted in a shortfall of approximately $50 million relative to our targeted Q2 revenue” - John Murphy, EVP & CFO, Q2 Earnings call.

Despite the hit to the advertising business, the company is a beneficiary of the current dislocation medium to long term as enterprises rush to digitally manage workflows and improve digital customer experience. As a result of the overall resiliency of the business, the company was able to deliver impressive double-digit growth in Q2 2020 revenue of 14% on a YoY basis while seeing gross margins increase by 150 basis points to 86.7% during the quarter. Adobe Sign, the company’s cloud-based e-signature service offering has seen a strong 175% increase in usage since the beginning of 2020. Although Adobe is currently a smaller player in the e-signature market segment, the company is taking significant steps to penetrate the market further.

“As with our Creative business, Document Cloud benefited from tailwinds associated with knowledge workers and communicators working from home, and we had a particularly strong quarter driving new business for Adobe Sign, with net new ARR more than doubling year-over-year.” - John Murphy, EVP & CFO, Q2 Earnings call.

Moreover, Photoshop express monthly active users surpassed 20 million, Fresco saw 40%+ increase in downloads, Premiere Rush monthly active users were up 75% on a QoQ basis. A similar surge in usage was seen in other Document Cloud applications as well.

Dominating the market with strong economic moats

Adobe’s products especially Photoshop (with over 20 million monthly active users) and Illustrator are amongs the most widely used solutions with a strong global reach and reputation among creative professionals. They are essentially gold standards in creative industries that most professionals need to be familiar with to advance their careers. In fact, Adobe’s promotional offers for students allows them to become well versed with Adobe’s solutions from an early stage. Most big and small enterprises include Adobe’s software offerings as an integral part of their business workflow. Switching to a new or existing alternative for Adobe products may not be viable for existing users (both companies as well as creative professionals) due to additional time required to learn the new software resulting in high “switching cost”. Recently, Adobe provided 30 million students with creative cloud access and teachers with distance learning support in response to school closures due to COVID-19.

Besides high switching costs, the proprietary file format for few of its widely used products (e.g. psd, psb, ai, xd, and more) results in a “network effect” and help preserve the company’s market position. A substantial growth in user base over the years has led to the file formats becoming a widely accepted standard globally. Adobe’s software then becomes almost mandatory for users to eliminate difficulties in sharing and to felicitate collaboration amongst groups.

A largely subscription-based business leads to stickiness in revenue

In 2013, the company decided to overhaul its business model. It discontinued its Creative Suite offering that provided a perpetual license on purchase and enabled all new feature updates through Creative Cloud subscription service. The subscription-based business model allows Adobe to generate more predictable and stable cash flows. The share of subscription revenue has significantly grown in the past few years. 92% of the total revenue comes from subscriptions as compared to just 67% in 2015.

Strong and consistent operating performance over the years

The company has delivered strong top-line as well as bottom-line performance during the recent years, supported by regular introduction of new products and services while continually updating existing solutions to improve their value proposition. Revenue has grown at a strong CAGR of ~22% between 2014-2019 while gross margins have stayed between 84% to 87% over the years. The overall revenue growth has been led by 24.2% CAGR revenue growth in Digital Media segment and 18.8% growth in Digital Experience segment while Publishing segment revenue has grown 6.5% during the same period.

Strategic acquisitions such as Marketo and Magento have also led to an increase in customer base for experience cloud. The inorganic expansion has provided an opportunity to cross-sell existing Adobe’s experience cloud solutions to customers of acquired companies. As per 2019 Analyst Meet, nearly 90% of the top 100 experience cloud customers opted for over 3 products in 2019 as compare to 66% in 2014 and generated ~$6 million in average ARR as compared to just ~$3 million in 2014.

Creative Cloud is expected to continue to grow given the strong moats and one-stop solution it offers. Adobe Sign’s rising popularity and market size also offer vast room for growth ahead in the e-signature market within the document cloud.

Adequate liquidity allows the company to be opportunistic

Adobe generates strong positive and stable cash flows backed by its subscription-based business model. TTM Q2 2020 CFO stood at $4,808 million, enough to cover the company’s total debt. Besides, the company had strong liquidity position of $3,044 million in cash and cash equivalents and $1,307 million in short-term investments as of May 2020. Total long-term debt stood at $4,114 million with limited near-term maturity and a well-spread maturity schedule. Despite strong cash flows, Adobe does not pay dividends however it uses the excess cash to repurchase equity shares and make strategic acquisitions. In H1 2020, the company repurchased shares worth $1.7 billion. Below are major acquisitions the company has executed over the last few years.

Premium valuation however well-deserved given powerful moats and strong growth prospects

The company not surprisingly trades at a premium valuation both in absolute terms due to its strong business franchise as well as relative to its own past due to tailwinds from a ‘work from home’ economy to its business long term. We continue to believe that the company still provides long-term oriented investors upside as it is set to experience above average growth in all its business verticals including creative cloud, document cloud as well as experience cloud.

Risks:

Prolonged slowdown: The current weak economic scenario has so far just impacted Adobe’s advertising solutions business. A prolonged slowdown or a slow recovery may result in rest of the business verticals to experience some slowdown as the benefits from ‘work from home’ get offset by cyclical slowdown. Having said that, Adobe will come out of any such period without experiencing much damage due to its subscription model, ready to capitalize on secular tailwinds in its end markets.

Conclusion

Adobe has delivered strong operational performance over the years and is well-positioned to capitalize on the addressable market opportunity in its verticals using its strong competitive positioning and execution. Additionally, the COVID-19 outbreak has just accelerated its growth profile further in the medium to long term. We believe the stock is a must-have mega tech holding in any long-term oriented investor’s portfolio. And in particular, if you are looking for an “income via growth” stock (i.e. generating income by selling some of your long-term winners) Adobe is attractive.