Energy demand was reduced by the pandemic (for example, less people needed gas to drive their cars to work), and that came after supply was increased by improved extraction technologies (for example, fracking). This resulted in major pain for the energy sector, especially as investors flocked to the technology stocks that naturally fit the “social distancing” story during the pandemic. However, a lot has changed this year, as oil prices are up and the energy sector (XLE) has gained about 40%! In this report, we highlight 50 high-yield energy stocks that are up big, and then dive into three names that are particularly attractive and worth considering.

Sector Rotation:

For starters, a big sector rotation is under way this year, as value stock sectors Energy and Financials (XLF) lead the market higher, while technology stocks (XLK) continue to lag, as you can see in the following chart.

source: Ycharts

And a lot of investors believe this trend may continue for a while as tech stock valuations remain high (even after this year’s weakness) and value stocks (energy in particular) have new life. Before getting into the details, let’s first have a look at over 50 high-yielding energy sector stocks that are up big this year.

50 High-Yield Energy Stocks, Up Big:

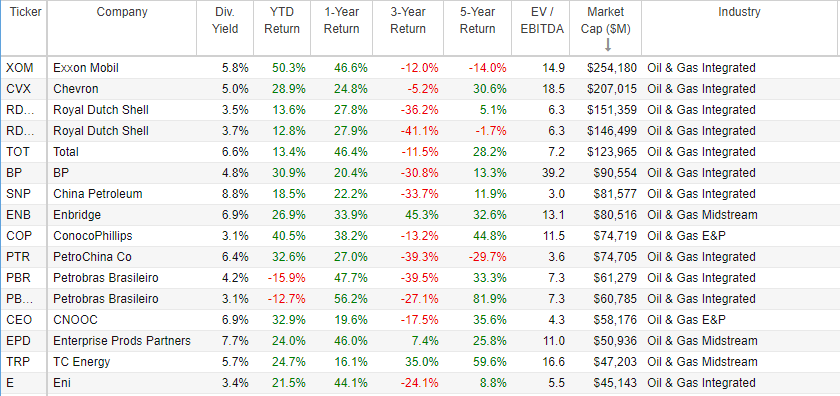

The following table includes energy sector stocks that yield at least 3%. The list is organized by market cap, and as you can see—performance has been very strong so far this year.

source: StockRover

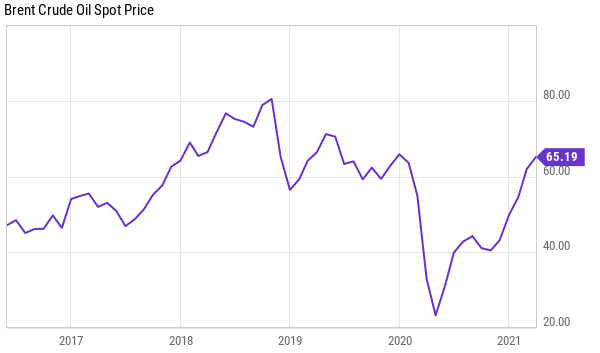

Of course a big driver of this energy sector rebound has been strength in oil prices. For example, as you can see below, the Brent Crude Oil spot price has shown significant gains since the initial depths of the pandemic, and especially so far this year.

source: Ycharts

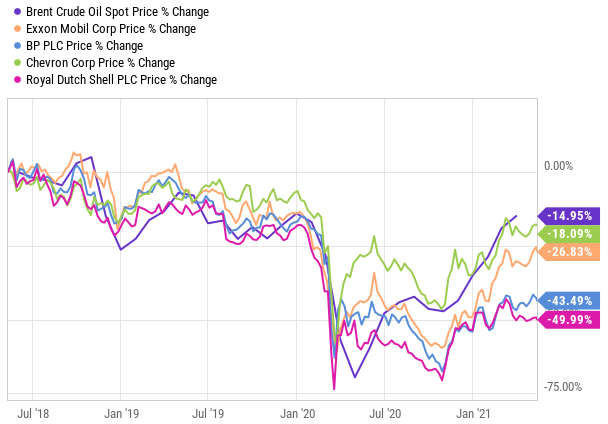

And as oil prices rise, so too do the prices of the big integrated energy companies. Specifically, there is a significant correlation between the stock prices of these companies and the price of oil, as you can see below.

source: Ycharts

Inflation:

Worth mentioning, inflation has kicked up this year. For example, CPI (which includes energy costs) accelerated at its fastest pace in over 12 years. The following quote from a recent CNBC article provides some good perspective:

Inflation in April accelerated at its fastest pace in more than 12 years as the U.S. economic recovery kicked into gear and energy prices jumped higher, the Labor Department reported Wednesday.

The Consumer Price Index, which measures a basket of goods as well as energy and housing costs, rose 4.2% from a year earlier. A Dow Jones survey had expected a 3.6% increase. The month-to-month gain was 0.8%, against the expected 0.2%.

Energy Stocks, Dividend Stories:

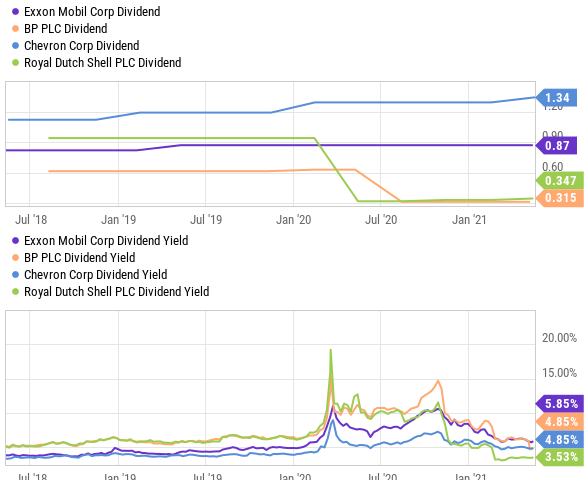

Returning to the energy sector, volatile oil prices have impacted the dividends of many popular stocks in the space. For example, you can see the recent history of dividend payments (and cuts) as well as dividend yields, for popular energy sector stocks Exxon Mobil (XOM), BP (BP), Chevron (CVX) and Royal Dutch Shell (RDS.B), below.

source: Ycharts

And of course the strength of the dividends is tied to the cash flows of the company (which in turn is tied to the price of oil) as you can see in this next chart.

source: Ycharts

And perhaps encouraging, the recent uptick in the price of oil may bode well for continued strength in the sector.

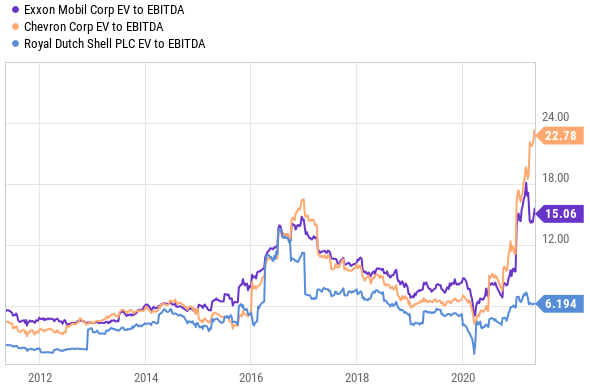

Valuation Multiples (EV/EBITDA):

Enterprise Value to EBITDA (earnings before interest taxes depreciation and amortization) is a popular valuation multiple in the energy space (EV is preferred over market cap because it captures the high debt loads common in the sector, and EBITDA because it is a more pure form of earnings power for these capital intensive businesses), and you can see that multiples fell during the onset up the pandemic, but have since been on the rise.

source: Ycharts

But before you go claiming the rally is already over and valuation multiples are already to high, it makes sense to consider the forward valuation mutiples (because after all, companies should be valued based on their future value, instead of looking only in the rear view mirror), and in this case these same companies look relatively attractive.

source: Ycharts

What’s more, if energy prices stay at their current levels, these businesses can maintain attractive profitability that was elusive (if not impossible) with oil prices trading much lower (more on a specific example of this later).

Midstream Companies:

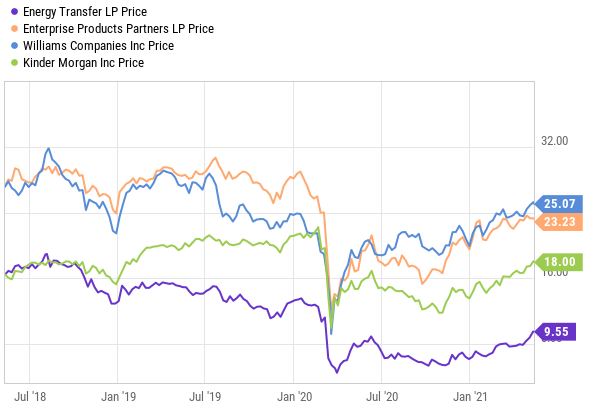

Massive integrated energy companies (such as Exxon and BP) are not the only way to play the energy sector, and midstream players (i.e. the companies that help transport oil and gas) have attractive qualities of their own (including steadier earnings based on long-term contracts, as well as higher yields that so many investors desire).

For starters, here are a few popular high-yielding midstream players, and as you can see below—their prices have been a bit steadier than others in the energy sector.

source: Ycharts. (ET) (EPD) (WPZ) (KMI)

And while midstream companies are in theory supposed to be protected against volatility in oil prices (because of the long-term contracts that are a fundamental part of their businesses), they are not immune to the potential bankruptcies of energy exploration and production companies (i.e. if the companies these midstreams have contracts with go bankrupt—those long-term contracts aren’t so attractive anymore).

And while the popular midstream companies we have highlighted do continue to offer high yields (see chart below) they have faced their own “dividend” challenges.

source: Ycharts

Three (3) Energy Stocks Worth Considering:

With that stock market and energy sector backdrop in mind, we do believe select energy-related stocks continue to be very attractive and worth considering for investment, despite the strong performance of the sector already so far this year.

1. Adams Natural Resources Fund (PEO), Yield: 6.1%

The Adams Natural Resources Fund (PEO) is a big-yield closed-end fund trading at a wide discount to its net asset value. And with increasing momentum in the energy sector (combined with the re-opening trade and higher oil prices/inflation) this one is worth considering. Here is a peak at the fund’s 10 largest holdings (as of the most recent quarter-end reporting, 3/31/21), which are heavily concentrated in the energy sector:

source: Adams Funds

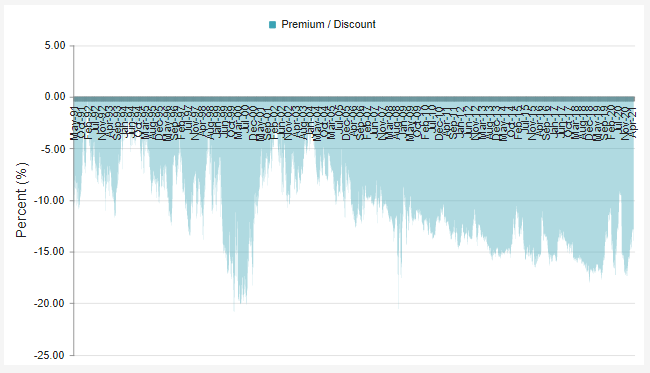

And also compelling, it trades at a wide discount to its net asset value, as you can see in this next chart.

source: CEF Connect

One of the unique characteristics of closed-end funds is that they can trade at large premiums or discounts to net asset value (i.e. the aggregate market value of the underlying holdings) because (unlike ETFs and mutual funds) CEF prices are determined entirely by supply and demand (i.e. there is no immediate mechanism in place to keep the price and NAV aligned). And while there is no guarantee the discount will go away, the discount does mean you get access to the dividend streams of the underlying holdings at a discounted price—which is attractive.

Important to note, PEO pays three smaller quarterly dividends, followed by a larger year-end dividend in Q4. The fund pays at least 6% annually (last year was 6.1%) and this year is looking like the payout can be significantly higher, considering the very strong performance of the sector and the holdings.

2. Exxon Mobil (XOM), Yield: 5.8%

With inflation on the rise, the pandemic trade continuing to unwind, and growing momentum on the side of value plays, Exxon Mobil looks good. The company announced expectation-beating Q1 earnings back on April 30th (they beat on earnings and revenues), and since that time Wall Street analyst price target increases have been rolling in (see below).

source: Factset

Unlike some of its peers, Exxon is making it through the pandemic without draconian cuts to its dividend. And with a valuation multiple on the low end of its historical range, the shares are worth considering for the dividend and the continuing price appreciation potential (especially with energy prices up). According to Morningstar sector strategist, Allen Good:

“[Exxon] should also benefit from the lift in oil and natural gas prices… Combined with a more restrained capital budget reiterated at last month’s annual analyst day, we think investors will begin to come around given its low valuation. As such, it remains our preferred name in the sector.”

As the pandemic trade continues to unwind (popular tech stocks are still not cheap), Exxon will continue to benefit, especially as the sector has momentum (and the higher commodity prices to back it up). For yield and price appreciation potential, Exxon is worth considering.

3: Enphase Energy, Yield: 0.0%

Enphase Energy is a leading provider of microinverters and batteries used for solar energy generation and storage. It doesn’t offer a big dividend yield, but it does have many attractive qualities (including a very significant amount of long-term price appreciation potential). Just last week completed a detailed report on Enphase, where we had a positive overall take. Aside from highlighting a couple big risk factors in that report, we concluded positively, as follows:

Enphase Energy is one of the most attractive plays in solar space. Operating in the fast-growing sustainable energy solutions industry, the company has demonstrated strong top-line growth and expanding margins over the last few years. While the company’s valuation is at a bit of a premium, Enphase’s microinverter technology and its highly integrated grid agnostic solar deployment with storage and real-time remote monitoring presents a strong moat. We like the opportunity here for long-term oriented investors, especially on the recent price pullback.

The shares are down further in the week since we shared that report, thereby making the valuation more compelling, in our view.

Conclusion:

Energy stocks are up big this year as oil prices are up and the pandemic trade continues to unwind. And the sector seems to have the momentum and legs to keep running, given the strengthening cash flows and the fact that pandemic darling tech stocks are still quite expensive. In our view, Exxon Mobil (XOM), the Adams Natural Resources Fund (PEO) and alternative play Enphase Energy (ENPH) are all attractive. We currently own shares of PEO and ENPH.