As mentioned in our previous note, BDCs are like banks, only riskier. Not only are BDCs facing increasing stress due to slowing economic growth and increasing interest rates (i.e. the tradeoff between higher floating rate interest payments received and higher default risk on loans), but some BDCs (such as those focused on venture capital) are dramatically over-exposed to fallout from the Silicon Valley Bank mess. In this note, we share updated data on 40 BDCs, and then dive deeper into 4 specific venture-capital-focused BDCs—and how we expect them to fare in light of the SVB mess—buyer beware!

BDC Overview: They are Risky!

For starters, BDCs are like banks (they makes loans, specifically to small/ middle-market businesses), but they are riskier (because the loans are typically too small, too unique and too risky for traditional banks in the first place). In fact, following the ’08-’09 financial crisis, BDCs grew because they picked up new business that new bank regulations (and reserve requirements) wouldn’t allow traditional banks to deal in. This is your first clue that BDCs are risky!

Next, the fact the BDCs offer such high dividend yields (see table below) is your next clue that BDCs are risky. Specifically, the charge higher rates on loans (thereby enabling the higher dividend yields) because the loans are risky and higher rates are required to offset the increased risk of default.

Next, BDCs don’t pay taxes on corporate income as long as they pay almost all of it out as dividends to investors. This is built into the tax law as an incentive to get lenders (i.e. BDCs) to loan to business that are otherwise too risky). This should be another red flag indication that BDCs are risky.

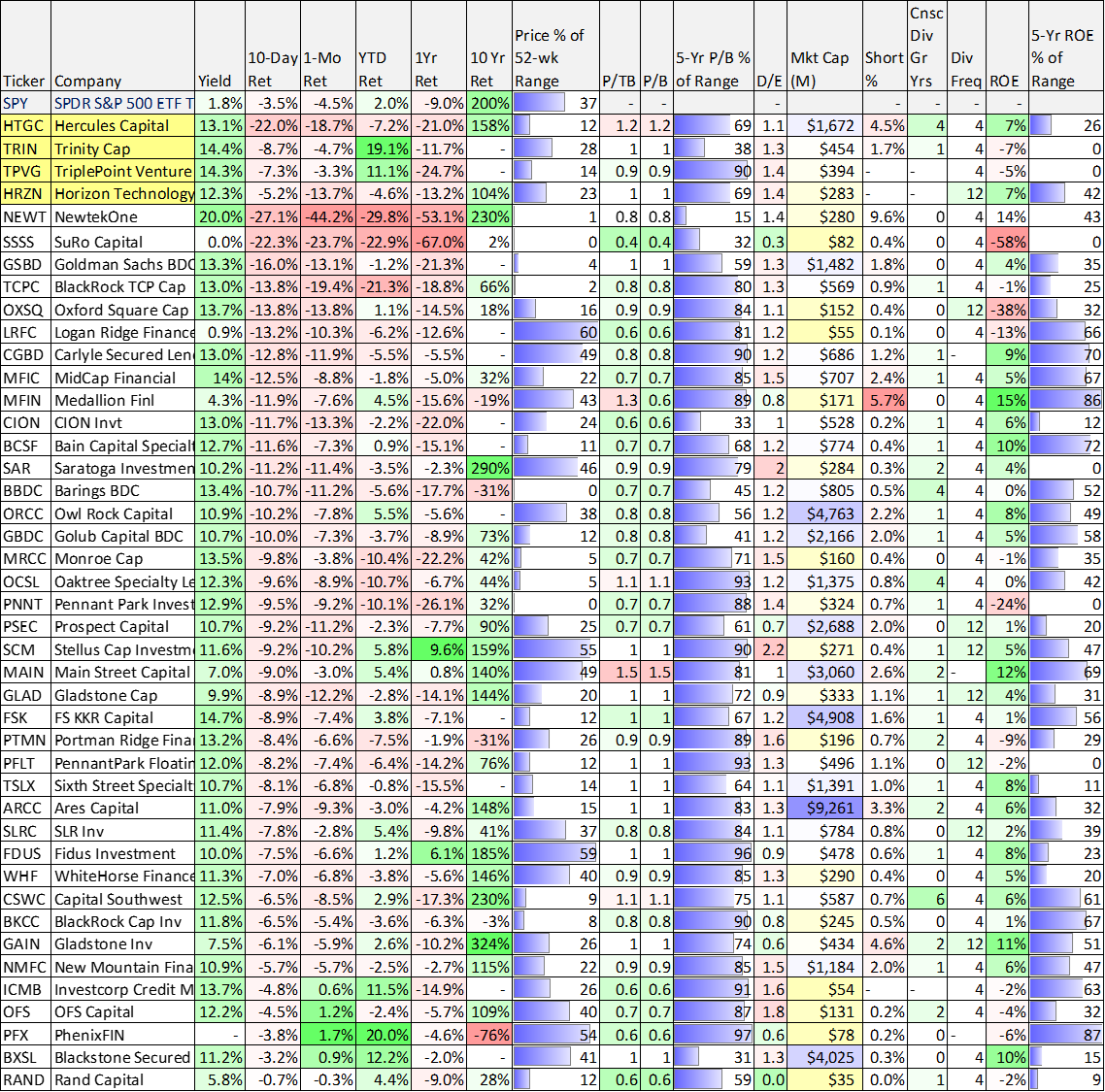

data as of Friday’s close 17-Mar-2023

And some BDCs are riskier than others because they concentrate all their business in certain types of loans (such as venture capital) instead of diversifying more broadly (such are Ares Capital, for example, as we recently wrote about in detail here).

Silicon Valley Bank Fallout:

In fact, the 4 BDCs highlighted in yellow in the table above are concentrated in the venture capital space (i.e. they make loans to a lot of private startup and growth companies) the same industry as Silicon Valley Bank (SIVB).

And for a little perspective, according to SIVB’s website:

“We bank nearly half of all US venture-backed startups, and 44% of the US venture-backed technology and healthcare companies that went public in 2022 are SVB clients. source: PitchBook and SVB analysis, as of 12/31/22.

In a nutshell the 4 BDCs highlighted in yellow and SIVB are operating in the same space. Specifically, the VC growth startup companies that BDCs lend to are also largely using SIVB as their bank. This create big risks (as we will describe below).

Bank Distress: Another Government Bailout

Before getting into the four specific BDCs, it’s worth noting that the government has basically announced a bailout of SIBV, et al. Specifically, they are making sure that companies banking with SIVB will have access to all of their cash, including cash in excess of the $250,000 FDIC guarantee. At first, this may sound like “problem solved,” but it’s more complicated than that.

For example, it’s not 100% clear that the new government run SIVB (it’s run by the government until they can find a new buyer) will fully extend lines of credit. Specifically, startups that bank with SIVB relied on lines of credit to keep their business running. But once the government finds a new buyer for SIVB—it’s not clear if those lines of credit will be extended for the long-term, or if they will attempt to get out of that business altogether. This article does an excellent job of explaining the risks associated with this disruption.

4 Venture Capital Focused BDCs:

Now let’s take a closer look at each of the 4 VC-focused BDCs impacted by the banking mess, including statements about the situation from the companies themselves (i.e. current 8K reports they all submitted to the SEC).

Hercules Capital (HTGC) is a business development company. The firm specializes in providing venture debt, debt, senior secured loans, and growth capital to privately held venture capital-backed companies at all stages of development from startups, to expansion stage including select publicly listed companies and select special opportunity lower middle market companies that require additional capital to fund acquisitions, recapitalizations and refinancing and established-stage companies.

Here is a link to the 8K Current Report Hercules filed with the SEC with regards to SIVB. And here are some key highlights from that report.

Hercules has enjoyed a competitive and collaborative relationship with SVB throughout our own 18-year history and we have partnered with them on a variety of lending transactions over the years. We do not, however, hold any cash or cash equivalents or have any direct banking or operational relationship with SVB and we do not expect any direct impact on our day-to-day operations as a result of SVB’s closure.

For instance, here is an example of how Hercules and SIVB worked together:

Silicon Valley Bank, the bank of the world's most innovative companies and investors, and Hercules Capital, Inc. (NYSE: HTGC), today announced that they provided a $300 million credit facility to Oak Street Health, a network of value-based primary care centers for adults on Medicare.

TriplePoint Venture Growth (TPVG) is a business development company specializing investments in venture capital-backed companies at the growth stage investments. It also provides debt financing to venture growth space companies which includes growth capital loans, secured and customized loans, equipment financings, revolving loans and direct equity investments.

And here is a link to the 8K Current Report TPVG submitted to the SEC with regards to Silicon Valley Bank. And here are some key highlights from that report.

Neither the Company nor TriplePoint Advisers LLC (the “Adviser”), the investment adviser of the Company, maintains any deposit, payment processing or other accounts or credit facilities with SVB or Signature Bank, or their successors. The Company does not participate in any credit facilities agented by SVB or Signature Bank, or that include SVB or Signature Bank as a lender.

The Company and the Adviser continue to closely monitor the situation regarding the SVB and Signature Bank receiverships and related developments as they relate to any of the Company’s borrowers and will continue to assess any indirect impact to the Company as a result of the same.

Horizon Technology Finance (HRZN) is a business development company specializing in lending and and investing in development-stage investments. It focuses on making secured debt and venture lending investments to venture capital backed companies in the technology, life science, healthcare information and services, cleantech and sustainability industries.

And here is a link to the 8K Current Report TPVG submitted to the SEC with regards to Silicon Valley Bank. And here are some key highlights from that report.

Neither Horizon Technology Finance Corporation (the “Company”) nor Horizon Technology Finance Management LLC (“HTFM”), the investment adviser of the Company, maintain any deposit or other accounts or credit facilities with Silicon Valley Bank or Signature Bank, or their successors. Less than 2.5% of the fair value of the Company’s debt portfolio is junior in priority to a debt investment of Silicon Valley Bank or its successors. Less than 0.3% of the fair value of the Company’s debt portfolio is junior in priority to a debt investment of Signature Bank and its successors.

Trinity Capital (TRIN) is a business development company. It is a venture capital firm specializing in venture debt to growth stage companies looking for loans and/or equipment financing.

And here is a link to the 8K Current Report TPVG submitted to the SEC with regards to Silicon Valley Bank. And here are some key highlights from that report.

Trinity does not maintain any accounts or credit facilities with SVB. Management is closely monitoring the situation regarding the SVB receivership as it relates to any of the Company’s borrowers and continues to assess any indirect impact to the Company as a result of the same.

Trinity has a total liquidity position of approximately $173 million, comprised of approximately $162 million of undrawn capacity under its credit facility and $11 million in unrestricted cash and cash equivalents as of December 31, 2022. The Company’s Board of Directors previously approved a stock repurchase program, under which the Company may acquire up to $25 million in the aggregate of Trinity’s outstanding common stock, which the Company’s Board of Directors intends to use judiciously.

Pros and Cons of Investing in These 4 VC BDCs:

Cash is Safe: Per the government bailout, cash deposits at SIVB are safe. This is a huge “pro” for the companies these 4 VC BDCs invest in. It solves a lot of the immediate problens and challenges.

Lines of credit at SIVB appear safe, for now (but this could change, as per the linked article we provided earlier).

None of the BDCs bank their own money at SIVB (even though many of their portfolio companies do). This is a good thing.

All 4 of VC BDCs likely have made loans to BDCs that bank with SIVB (considering roughly 50% of the VC industry does). This could create challenges down the road, especially depending on what eventually happens to their lines of credit.

All 4 of the BDCs have ample liquidity, as they explained in their 8Ks. And this appears to be true considering they’re all well below the 2x leverage limit (as per data in our earlier table).

Some Assets Horizon at risk: per the 8K notes, Horizon appears to have a very small amount of junior debt that appears likely to get wiped out.

Hercules has the biggest market cap, an indication of potentially more strength and stability.

Hercules had an extensive relationship with SIVB, thereby indicating they may not be able to source new business as easily going forward, depending on who eventually acquires SIVB. For example, if JP Morgan or Goldman Sachs were to acquire it—they could just cut Hercules out of the picture on future deal flow and instead just direct the business to their own JP Morgan or Goldman Sachs lenders or BDCs. SIBV could be a great way for some other company to gain valuable VC industry relationships.

Trinity Share Buybacks: Trinity hints that they could be using the recent sharp price declines to buy back more shares (possibly a good thing if the business recovers and if they’re being purchased at a discount to NAV).

The economy is bad, but it can still get worse (which would mean more pain for BDC as more loans default). We believe the economy will get better, we just don’t know when.

Our Bottom Line Takeaways:

We like TPVG first, TRIN second, Hercules third and Horizon last. However, we still like BDCs ARCC, MAIN and ORCC more that all of them because they are better diversified (we own all three in our High Income NOW Portfolio).

If we had to buy one of the four, it would likely be TPVG, but for now we’re sticking with ARCC, ORCC and MAIN. However, if the prices of these four VC-focused BDCs keep falling, we are tempted to buy one or more. At the end of the day, it depends on your personal situation, goals and tolerance for risk.