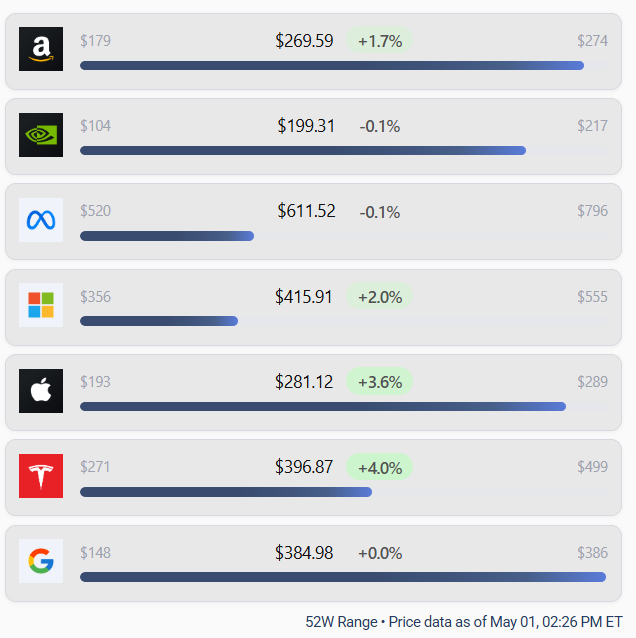

The latest earnings cycle from the “Mag 7” cohort—Apple, Microsoft, Amazon, Alphabet, and Meta—offered a clear message: fundamentals remain strong, but investor focus has shifted decisively toward AI monetization and capital discipline. The result was a paradoxical week where most companies beat expectations, yet stock reactions diverged sharply. This has created increasingly compelling investment opportunities.

Big Picture: Earnings Beats, Narrative Shift

Across the board, results were strong. Revenue and EPS generally exceeded estimates, with cloud, advertising, and ecosystem monetization all showing resilience. Amazon, Microsoft, Meta, and Alphabet each delivered meaningful top-line growth, while Apple reinforced its cash-return story.

However, the market is no longer rewarding beats alone. Instead, the key variable is return on AI investment. Companies signaling disciplined or clearly monetizable AI strategies outperformed, while those emphasizing aggressive capital expenditure (capex) faced skepticism.

Winners: Alphabet, Amazon, Apple

Alphabet (GOOGL): AI Monetization Leader

Alphabet emerged as the clearest winner this cycle. Its cloud division posted explosive growth—up roughly 60%+—demonstrating that AI demand is already translating into revenue at scale.

Importantly, Alphabet’s narrative is not just spending—it’s monetizing AI today via Google Cloud and search enhancements. With a massive backlog of enterprise contracts and improving margins, Alphabet is increasingly viewed as the “proof point” that AI capex can generate near-term returns.

Investment takeaway: Alphabet combines visible AI revenue, operating leverage, and scale, making it arguably the highest-quality AI compounder in the group.

Amazon (AMZN): Multi-Engine Growth with AI Optionality

Amazon delivered one of the strongest prints of the week, driven by AWS growth (28% YoY), advertising strength, and improving retail profitability.

The underappreciated angle is Amazon’s vertical integration in AI infrastructure, particularly its custom Trainium chips. Management suggested this could become a multibillion-dollar business, potentially competing with Nvidia.

While capex remains elevated, Amazon’s diversified model—cloud, ads, e-commerce, and emerging AI hardware—provides multiple monetization pathways.

Investment takeaway: Amazon offers the broadest AI exposure across infrastructure, applications, and consumer platforms, with optionality that is not fully priced in.

Apple (AAPL): Capital Discipline as a Feature

Apple’s earnings lacked the AI excitement of peers, but that’s basically why the stock works. Investors rewarded its measured spending approach, strong free cash flow, dividend growth, and massive buyback authorization.

In a market increasingly wary of unchecked AI spending, Apple’s restraint stands out. Its ecosystem strength (iPhone, services) continues to generate predictable cash flows, giving it flexibility to invest in AI without overcommitting upfront.

Investment takeaway: Apple remains a defensive compounder—less AI torque, but superior capital returns and balance sheet strength.

Mixed to Negative Reactions: Microsoft and Meta

Microsoft (MSFT): Strong Business, Timing Problem

Microsoft posted solid results, including continued Azure growth, but shares declined as management raised capex guidance significantly.

The issue isn’t demand—it’s timing. Microsoft is investing heavily to meet AI demand, but capacity constraints and front-loaded spending are delaying margin expansion.

Investment takeaway: Microsoft remains a long-term AI leader, but near-term returns may lag as infrastructure investments catch up with demand.

Meta (META): Spending Ahead of Monetization

Meta arguably had one of the strongest operating quarters, yet it was the worst stock performer. The reason: a massive increase in capex guidance (up to ~$145B), tied to AI infrastructure and metaverse ambitions.

Investors are questioning whether Meta’s spending will generate returns comparable to its core advertising engine, which remains highly profitable.

Investment takeaway: Meta is a high-risk, high-reward AI bet—compelling fundamentals, but execution risk tied to capital allocation.

Key Themes for Investors

1. AI Is Real—and Expensive

Big Tech is on pace to spend hundreds of billions on AI infrastructure, underscoring both the scale of the opportunity and the risk.

2. Monetization > Hype

Alphabet and Amazon outperformed because they demonstrated current revenue impact, not just future potential.

3. Capital Discipline Matters Again

Apple’s outperformance shows that in a higher-rate environment, free cash flow and shareholder returns still command a premium.

Bottom Line

This earnings week reinforced that the Mag 7 remains structurally advantaged, with dominant platforms, pricing power, and unmatched AI capabilities (massive moats!). The divergence in stock reactions is less about fundamentals and more about timing of returns on unprecedented investment cycles.

The market’s reaction was clear:

Buy monetizers (Alphabet, Amazon)

Hold compounders (Apple, Microsoft)

Be selective with spend-heavy stories (Meta)

However, in the long-term, IF spending is a harbinger of growth, investors may want to conisider the recent laggards in particular.

In aggregate, these companies aren’t just participating in the AI cycle—they are defining it, and that makes the Mag 7 compelling core holdings, despite any near-term volatility.