The appeal of the PIMCO Dynamic Income Fund (PDI) is easy to understand. A double-digit distribution yield, monthly income, and the PIMCO brand have made the fund one of the most widely followed closed-end funds (CEFs) in the income-investing universe. But as with any high-yield CEF, investors should look beyond the headline payout and ask a more important question: how sustainable is the income stream?

PDI remains a highly sophisticated credit vehicle managed by one of the strongest fixed-income teams in the industry. However, recent coverage data and Section 19 disclosures suggest investors should approach the fund with a more cautious and selective mindset than they may have during the ultra-low-rate era.

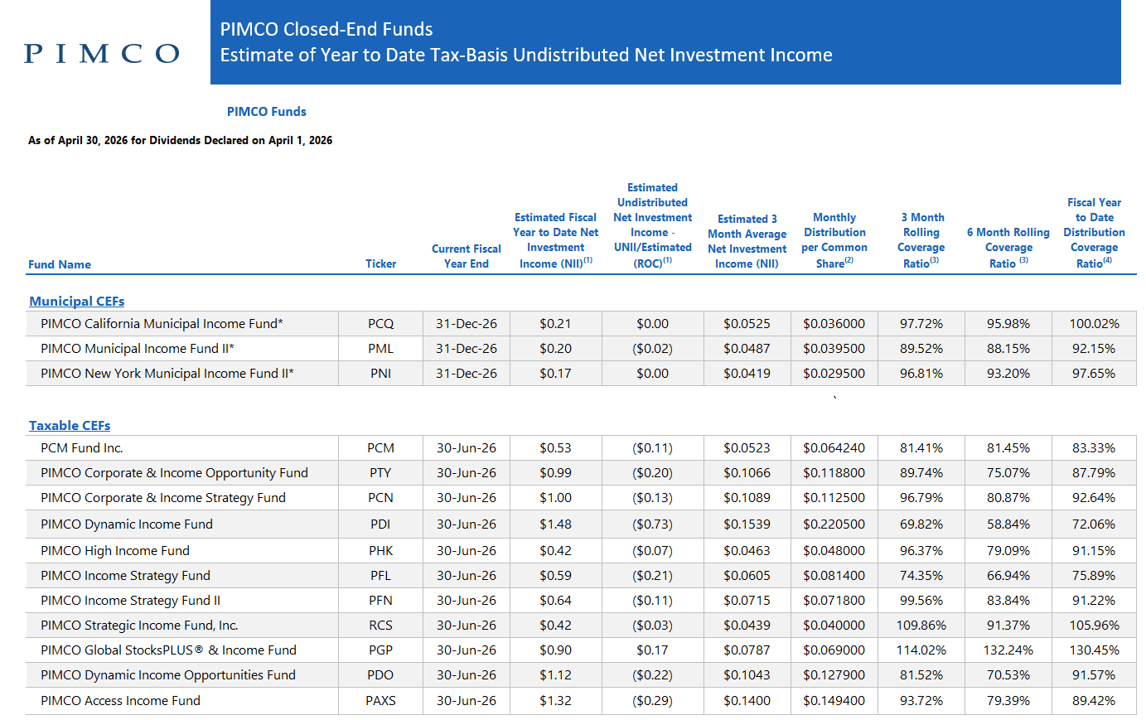

Distribution Coverage

The first issue income investors should examine is distribution coverage. According to PIMCO’s latest UNII report, PDI’s fiscal year-to-date distribution coverage ratio sits at roughly 72%, while six-month coverage is closer to 59%. In practical terms, the fund is currently not fully earning its distribution through net investment income.

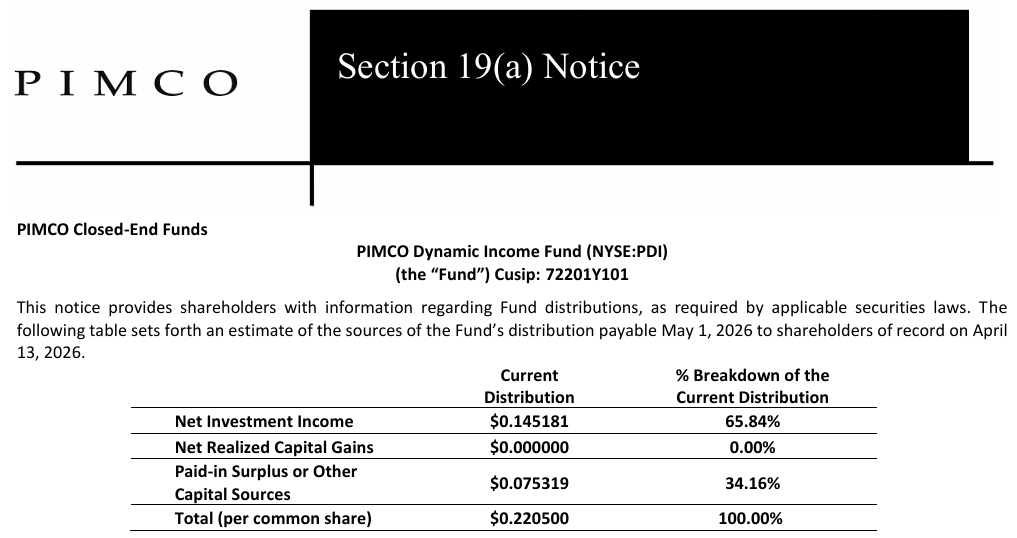

Section 19(a) Notices

That weakness is reinforced by the fund’s recent Section 19(a) notices. For example, the most recent one estimated that approximately 34% of the latest distribution came from “paid-in surplus or other capital sources” rather than traditional investment income or realized gains. While that does not automatically mean destructive return of capital, it does indicate that the current payout is being supported by sources beyond straightforward portfolio income generation.

Importantly, PDI’s undistributed net investment income balance (UNII) is also negative at approximately -$0.73 per share. Investors often overlook UNII, but it effectively serves as a reserve cushion for future distributions. A negative balance suggests the fund has less flexibility if market conditions weaken further.

That said, context matters.

About PDI

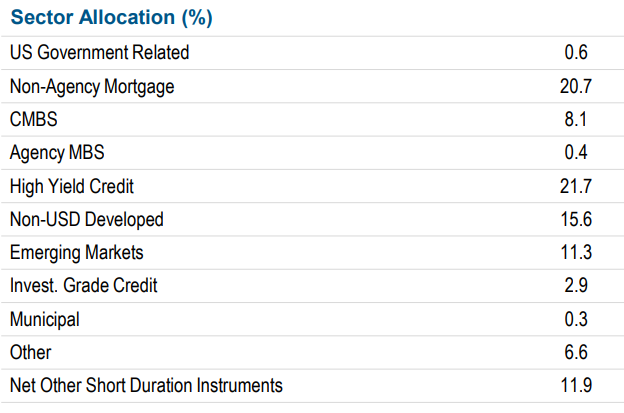

PDI is not a simple bond fund. The portfolio is an actively managed, leveraged global credit strategy that includes non-agency mortgages, high-yield credit, emerging-market debt, structured products, and derivative positions. PIMCO’s managers have historically used active trading, leverage, and institutional-level credit strategies to support distributions during periods when traditional bond income alone may not have been sufficient.

This is one reason many investors continue to give PIMCO funds the benefit of the doubt. The firm has deep credit research capabilities, extensive derivatives expertise, and access to institutional fixed-income markets that many competitors cannot replicate. Investors are not simply buying a portfolio of bonds; they are buying PIMCO’s active management platform.

Leverage

Still, leverage remains a major variable.

PDI currently operates with effective leverage above 36%, which amplifies both income potential and portfolio volatility. Leverage can work extremely well in stable or improving credit markets, but it also increases downside risks when spreads widen or financing costs rise. The painful drawdowns experienced by many leveraged bond CEFs during the 2022 rate shock remain a reminder that elevated yields rarely come without elevated risks.

Premium to NAV

Another factor investors should monitor closely is valuation. PDI recently traded at roughly a 6.5% premium to net asset value. Closed-end fund premiums can persist for long periods, especially when supported by a strong distribution history and a respected management team. However, premiums also introduce an additional layer of risk. If investor sentiment deteriorates or a distribution cut becomes more likely, the premium itself can contract quickly, creating downside pressure even if the underlying portfolio remains relatively stable.

This dynamic is particularly important because PDI’s distribution rate remains exceptionally high. Based on recent figures, the fund’s NAV distribution rate is above 16%, which places considerable pressure on management to continue generating distributable cash flow in a challenging fixed-income environment.

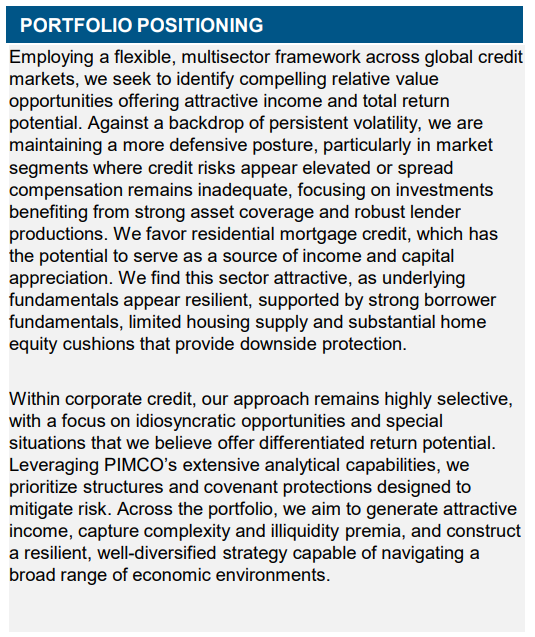

To be fair, PIMCO is quite aware of the risks. Recent portfolio commentary emphasized a more defensive and selective posture, focusing on residential mortgage credit, asset-backed securities, and structured credit opportunities where the managers believe fundamentals remain resilient. The firm also highlighted efforts to prioritize higher-quality opportunities and maintain flexibility amid ongoing macro uncertainty.

The Bottom Line

In this author’s view and best estimation, PIMCO remains one of the best bond fund managers in the world (with very deep resources and expertise). However, it seems likely they were not anticipating the fed’s rapid interest rate hikes (to fight inflation) after the covid-crisis (it was truly unprecidented)—and as a result PDI’s highly-leveraged holdings lost a lot of value (when rates rise, bond prices fall—all else equal). And PDI’s highly sophisticated management team kicked that can down the road as long as they could to avoid heavy return of investor capital (which many income investors loathe).

Through the uses of derivates (e.g. interest rate swaps), PDI delayed ROC (and the dreaded section 19(a) notices) in hopes interest rates would come down, the value of their holdings would go up, and they could better support the high distributions with capital gains (instead of ROC). They’ve done a diligent job, but they delayed as long as they could and the “paid-in surplus or other capital sources” (which means they’ve not be covering the income paid each period) have been rolling in.

The bad news is the yield is still very high and a bit unreasonable unless they get some significant interest rate cuts from the fed soon (PDI’s duration, or interest rate risk, is ~4.4 years). The good news is, they’ve been getting some of the pain out of the way (the “paid in surplus or other capital sources” has been a bit of a pressure release valve that goes unoticed by some investors). Additionally, the newly appointed fed chair seems to believe in interest rate cuts more than Jerome Powell.

If you are an income-focused investor, PDI remains an attractive option, but certainly don’t bet the farm on it (keep your allocations reasonable and prudently diversified to reduce risks).

And most importantly, at the end of the day, do what is right for you and your own individual situation.