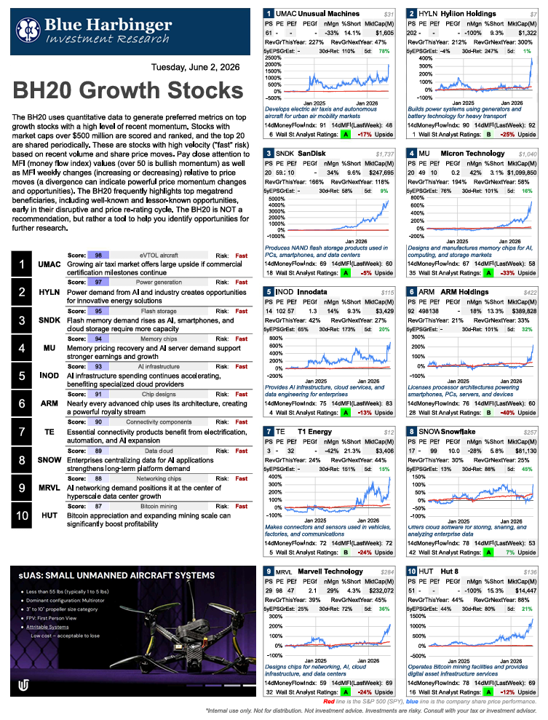

From time-to-time, I like to run (and share) this report on fast-paced growth stocks. The top 20 (plus honorable mentions) are generated based on technical and fundamental data “screens'“ as described below. To be clear, the BH20 is NOT a recommendation, but rather a tool to help you (and me) identify opportunities for further research.

Coming in at #1 in this week’s iteration, is Unusual Machines (UMAC). These shares spiked after The Wall Street Journal reported that the Trump administration was considering funding a group of U.S. drone companies.

Note: The BH20 uses quantitative data to generate preferred metrics on top growth stocks with a high level of recent momentum. Stocks with market caps over $500 million are scored and ranked, and the top 20 are shared periodically. These are stocks with high velocity ("fast" risk) based on recent volume and share price moves. Pay close attention to MFI (money flow index) values (over 50 is bullish momentum) as well as MFI weekly changes (increasing or decreasing) relative to price moves (a divergence can indicate powerful price momentum changes and opportunities). The BH20 frequently highlights top megatrend beneficiaries, including well-known and lessor-known opportunities, early in their disruptive and price re-rating cycle. The BH20 is NOT a recommendation, but rather a tool to help you identify opportunities for further research.

1. Unusual Machines (UMAC)

Unusual Machines is focused on drones and drone components, serving commercial, recreational, and potentially defense-related applications. The investment thesis is that domestic drone manufacturing could become strategically important as governments and enterprises seek alternatives to foreign suppliers. If the company captures a meaningful share of a rapidly expanding drone ecosystem, revenue growth could be substantial relative to its current size. The biggest risks are execution, limited scale, competition from much larger players, and the possibility that anticipated drone-market growth takes longer than expected.

2. Hyliion Holdings (HYLN)

Hyliion develops power-generation technologies designed to provide reliable electricity for data centers and industrial users. The bull case centers on exploding electricity demand from AI infrastructure, which could create a shortage of power capacity and increase demand for distributed energy solutions. If Hyliion's technology gains traction with large customers, the stock could benefit from a dramatic re-rating. The primary risks are commercialization challenges, customer adoption uncertainty, and the company's history of operating in highly competitive and capital-intensive markets.

3. SanDisk (SNDK)

SanDisk produces NAND flash memory products used in smartphones, PCs, data centers, and storage devices. The opportunity comes from AI, cloud computing, and data creation trends that require ever-increasing amounts of storage. Memory markets are cyclical, so if pricing enters a strong upcycle, earnings can rise much faster than revenue. The main risk is that memory is a commodity business, where oversupply can quickly compress margins and profitability.

4. Micron Technology (MU)

Micron is one of the world's largest producers of DRAM and NAND memory chips. It is particularly well positioned for AI because advanced AI servers require far more high-bandwidth memory than traditional computing systems. If AI infrastructure spending remains elevated for several years, Micron could experience a sustained earnings boom. Risks include cyclical downturns in memory pricing, aggressive competition, and the possibility that AI-related demand growth slows.

5. Innodata (INOD)

Innodata helps organizations prepare, label, structure, and manage data used to train AI models. As AI systems become more sophisticated, high-quality training data becomes increasingly valuable, creating a potentially attractive niche for the company. Because Innodata is relatively small, even a few major contracts could significantly impact financial results. The risks are customer concentration, valuation expansion that may already reflect optimistic expectations, and intense competition within the AI services industry.

6. Arm Holdings (ARM)

Arm licenses the chip architecture used in billions of smartphones, embedded devices, and an increasing number of AI and cloud-computing systems. The appeal is that Arm earns royalties on a huge ecosystem without having to manufacture chips itself, creating a highly scalable business model. If Arm continues gaining share in data centers and AI computing, royalty growth could accelerate for years. The biggest risks are its already-high valuation, dependence on partners, and the possibility that competing architectures gain traction.

7. TE Connectivity (TE)

TE Connectivity makes connectors, sensors, and components that are embedded in vehicles, industrial equipment, factories, and communications infrastructure. While less flashy than AI software companies, TE benefits from long-term trends such as electrification, automation, and increased electronic content in nearly every device. The company could be a strong compounder because it sells critical products into many growing end markets. Risks include economic slowdowns, industrial spending cycles, and slower-than-expected growth in key sectors such as electric vehicles.

8. Snowflake (SNOW)

Snowflake provides a cloud-based platform that helps companies store, analyze, and share data. Its opportunity lies in becoming a central hub where enterprises organize data for AI applications, analytics, and machine learning workflows. If Snowflake successfully becomes a foundational layer of enterprise AI infrastructure, revenue growth could remain strong for a long period. Risks include fierce competition from large cloud providers, pressure on customer spending, and the challenge of justifying a premium valuation.

9. Marvell Technology (MRVL)

Marvell designs chips used in networking, data centers, cloud infrastructure, and AI systems. As AI clusters become larger and more complex, networking hardware becomes increasingly important, creating a potentially massive growth opportunity. The company could benefit from both AI compute expansion and the supporting infrastructure required to connect those systems. Risks include customer concentration, semiconductor industry cyclicality, and the possibility that AI infrastructure spending eventually moderates.

10. Hut 8 (HUT)

Hut 8 operates Bitcoin mining facilities and increasingly positions itself as a broader digital infrastructure provider. The bullish case is straightforward: if Bitcoin prices rise significantly, mining economics and company profitability can improve dramatically. Additionally, the company may benefit from demand for power and data-center infrastructure beyond cryptocurrency. The major risks are Bitcoin volatility, regulatory uncertainty, energy costs, and the fact that mining economics can deteriorate quickly during crypto downturns.

11. Datadog (DDOG)

Datadog provides monitoring, security, and observability software that helps companies keep cloud applications running efficiently. As enterprises deploy more AI workloads and increasingly complex cloud infrastructure, the need to monitor systems becomes mission-critical. The bull case is that Datadog becomes a standard operating system for cloud operations, allowing it to grow into a much larger software platform. The risks are slowing enterprise spending, competition from cloud vendors, and the challenge of maintaining high growth as the company matures.

12. Super Micro Computer (SMCI)

Super Micro designs and assembles servers used in AI data centers. The opportunity is enormous because every AI deployment requires vast amounts of computing infrastructure, and Super Micro has become a major supplier to that ecosystem. If AI spending remains elevated for years, revenue and earnings could continue expanding rapidly. The biggest risks are hardware-industry cyclicality, dependence on a handful of suppliers and customers, and the possibility that AI infrastructure spending cools after the current boom.

13. Redwire Corporation (RDW)

Redwire develops space technologies including satellite systems, manufacturing platforms, and space infrastructure. The investment thesis is that commercial space activity is still in its early innings and could become a multi-decade growth industry. If space manufacturing, defense contracts, and satellite deployments accelerate, Redwire could emerge as a key supplier. Risks include execution challenges, government budget uncertainty, and the inherently speculative nature of the space sector.

14. Nebius Group (NBIS)

Nebius is building AI-focused cloud infrastructure designed for training and running large AI models. The bull case is that demand for AI compute significantly exceeds supply, creating opportunities for specialized providers. If Nebius successfully scales its infrastructure and wins enterprise customers, growth could be extraordinary. Risks include massive capital requirements, fierce competition, and the possibility that larger cloud providers dominate the market.

15. Applied Optoelectronics (AAOI)

Applied Optoelectronics makes fiber-optic networking products used in data centers and telecommunications. AI clusters require huge amounts of high-speed networking, which could dramatically increase demand for optical components. The company has historically been volatile, but AI networking demand creates a potential new growth cycle. Risks include customer concentration, pricing pressure, and intense competition in optical hardware markets.

16. Red Cat Holdings (RCAT)

Red Cat develops drones and related technologies for military and commercial applications. The opportunity comes from rising defense spending and increasing use of autonomous systems in modern warfare. If Red Cat secures large military contracts, revenue growth could be dramatic relative to its current size. The risks are contract uncertainty, competition, and dependence on government procurement cycles.

17. DigitalOcean (DOCN)

DigitalOcean provides cloud infrastructure primarily for startups and small-to-medium-sized businesses. Its appeal is a simpler and often more affordable alternative to hyperscale cloud providers. If smaller companies continue adopting cloud and AI tools, DigitalOcean could grow steadily while expanding margins. Risks include competition from much larger rivals and limited pricing power.

18. POET Technologies (POET)

POET develops advanced optical technologies intended to improve data transmission in AI and networking systems. The company is attractive because its technology could solve bottlenecks in next-generation AI infrastructure. If its products achieve broad adoption, the upside could be many times its current valuation. The risk is that commercialization may take longer than expected or fail to gain meaningful market share.

19. ASP Isotopes (ASPI)

ASP Isotopes focuses on isotope enrichment technologies used in nuclear energy, medicine, and industrial applications. The bull case revolves around growing interest in advanced nuclear technologies and increasing demand for specialized isotopes. If its technology proves cost-effective, the company could participate in several large emerging markets. Risks include technical execution, regulatory hurdles, and commercialization uncertainty.

20. Astera Labs (ALAB)

Astera Labs develops semiconductor solutions that improve connectivity and data movement inside AI servers and data centers. As AI systems become larger, moving data efficiently becomes nearly as important as computing itself. If AI infrastructure spending remains strong, Astera could become a critical supplier. Risks include valuation risk, competition, and dependence on continued AI investment growth.

Honorable Mentions…

Ondas Holdings (ONDS)

Ondas develops wireless communications technologies and autonomous drone solutions. The investment thesis combines two growing markets: industrial automation and autonomous systems. If adoption accelerates in infrastructure, defense, or industrial markets, growth could be substantial. Risks include small-company execution challenges and uncertainty around customer adoption.

Applied Digital (APLD)

Applied Digital builds and operates facilities that support AI computing and high-performance workloads. The bull case is that demand for AI infrastructure remains so strong that additional capacity becomes extremely valuable. Long-term contracts with major customers could create substantial cash flow growth. Risks include financing needs, customer concentration, and potential oversupply of data center capacity.

Celestica (CLS)

Celestica manufactures and designs hardware used in networking, cloud computing, and communications systems. It benefits from many of the same AI infrastructure trends as more visible names but often receives less investor attention. If demand for networking and data-center hardware remains robust, earnings growth could continue for years. Risks include lower margins than software businesses and sensitivity to customer spending cycles.

IREN Limited (IREN)

IREN operates Bitcoin mining facilities and increasingly targets AI infrastructure opportunities. The appeal is a combination of energy assets, data-center capacity, and exposure to digital assets. If Bitcoin appreciates and AI demand remains strong, the company could benefit from two powerful growth drivers simultaneously. Risks include crypto volatility, power costs, and execution risk in expanding AI operations.

Zeta Global (ZETA)

Zeta uses AI and large-scale data analytics to help businesses acquire and retain customers. Its opportunity lies in leveraging proprietary consumer data to improve marketing outcomes. If AI-driven advertising becomes increasingly effective, Zeta could see meaningful revenue growth. Risks include privacy regulation, advertising spending cycles, and competition from larger platforms.

NVIDIA (NVDA)

NVIDIA is the dominant supplier of AI accelerators used to train and run advanced AI models. The company sits at the center of nearly every major AI investment trend and continues to expand into networking, software, and data-center infrastructure. If AI becomes as transformative as many expect, NVIDIA could remain one of the world's most important technology companies. Risks include its already massive valuation, growing competition, and the possibility that AI spending growth eventually normalizes.

CoreWeave (CRWV)

CoreWeave provides cloud infrastructure optimized for AI workloads. It has rapidly emerged as one of the most important independent AI cloud providers. If AI demand continues outpacing traditional cloud capacity, CoreWeave could grow at an extraordinary rate. Risks include heavy debt and capital spending requirements, customer concentration, and dependence on continued AI investment.

Bloom Energy (BE)

Bloom Energy develops fuel-cell systems that provide on-site power generation. The rise of AI data centers is creating immense electricity demand, potentially increasing the value of distributed power solutions. If utilities struggle to keep pace, Bloom could become an important provider of reliable energy infrastructure. Risks include execution, project financing, and competition from other energy technologies.

Vertiv Holdings (VRT)

Vertiv supplies power management, cooling systems, and infrastructure for data centers. Every AI server deployment requires substantial supporting infrastructure, making Vertiv a key beneficiary of AI growth regardless of which AI model wins. If AI data-center construction continues at current levels, Vertiv's addressable market could expand dramatically. Risks include cyclical capital spending and the possibility of slower-than-expected data-center buildouts.

Oklo (OKLO)

Oklo is developing small modular nuclear reactors intended to provide reliable, carbon-free power. The company has attracted attention because AI-driven electricity demand may require entirely new power-generation solutions. If Oklo successfully commercializes its reactor technology, the long-term opportunity could be enormous. The risks are significant: regulatory approvals, technology execution, financing needs, and the fact that meaningful revenue may still be years away.