With inflation on the rise, and interest rates poised to move higher, does it still make sense to own bonds? Depending on your situation, the answer is a resounding, yes! And this article reviews a compelling closed-end fund (“CEF”) that owns attractive bonds, trades at a discounted price, and offers a juicy 7.2% yield—paid monthly. We currently own shares.

DoubleLine Yield Opportunities (DLY), Yield: 7.2%

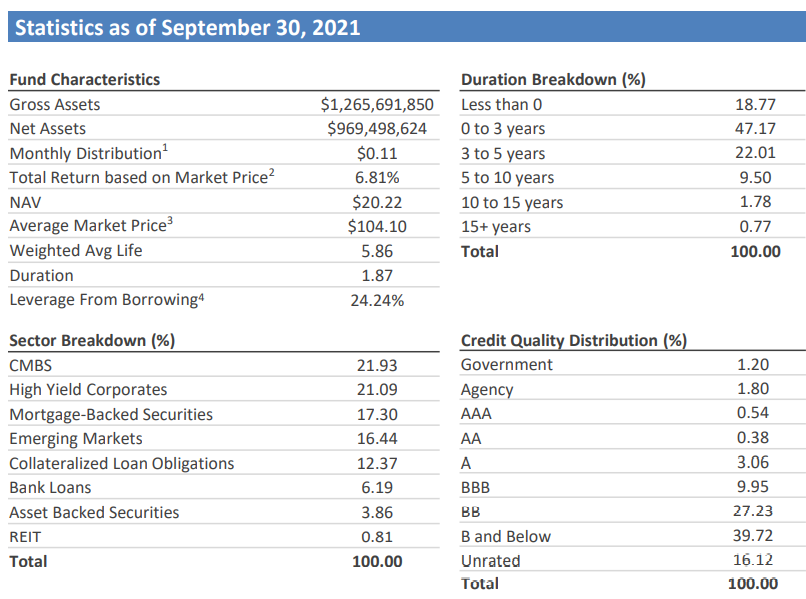

Managed by renowned bond investor, Jeffrey Gundlach, DLY’s objective is high total return (i.e. income plus price appreciation) with an emphasis on current income. And the fund accomplishes this objective by owning a diverse set of bonds across styles, as you can see in the sector breakdown below.

Also worth mentioning, DoubleLine enjoys many economies of scale and benefits that you don’t have as an individual investor, such as better borrowing rates (more on this later) a bigger team, and access to bonds that you simply don’t have the scale to buy on your own.

What is a Closed-End Fund (“CEF”)?

Similar to mutual funds and exchange traded funds, closed-end funds are a pooled vehicle that holds a basket of individual investments (for example, DLY recently had 477 holdings). And as a quick reminder, unlike mutual funds and exchange-traded funds, their is no immediate mechanism to bring the price of a closed-end fund in line with the value of its underlying holdings (or net asset value—NAV), and as such, CEFs can trade at significant discounts and premiums versus their NAV. This creates opportunities and risks, including buying at unusually high or low prices, as well as an ideal situation to apply leverage (or borrowed money) because CEFs don’t have to worry about the margin calls associated with fund inflows and outflows (because there are none—they’re closed end).

Discount to NAV:

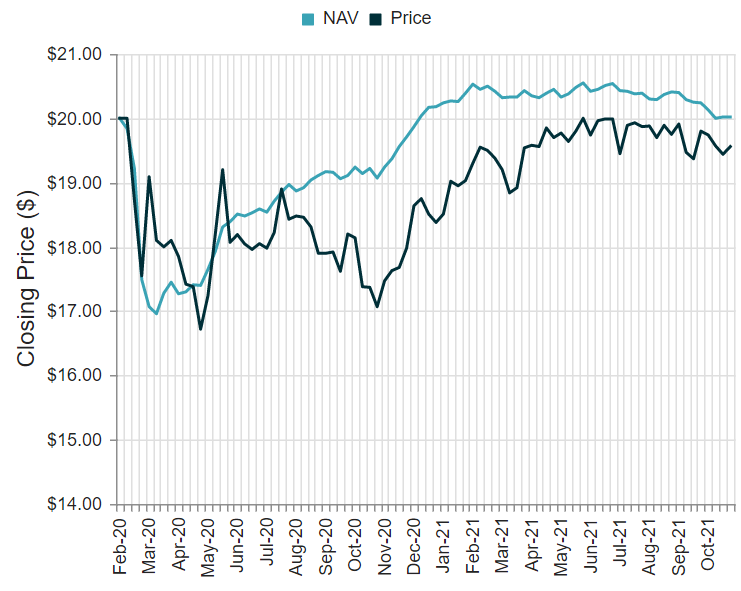

We generally prefer to purchase funds at a discount (on sale) than at a premium because it means we are getting access to the underlying holdings (and the income they produce) at a discounted price. Many popular bond CEFs currently trade at significant premiums. However, as you can see in the following graphic, DLY currently trades at a discount (currently -2.57%), something we like.

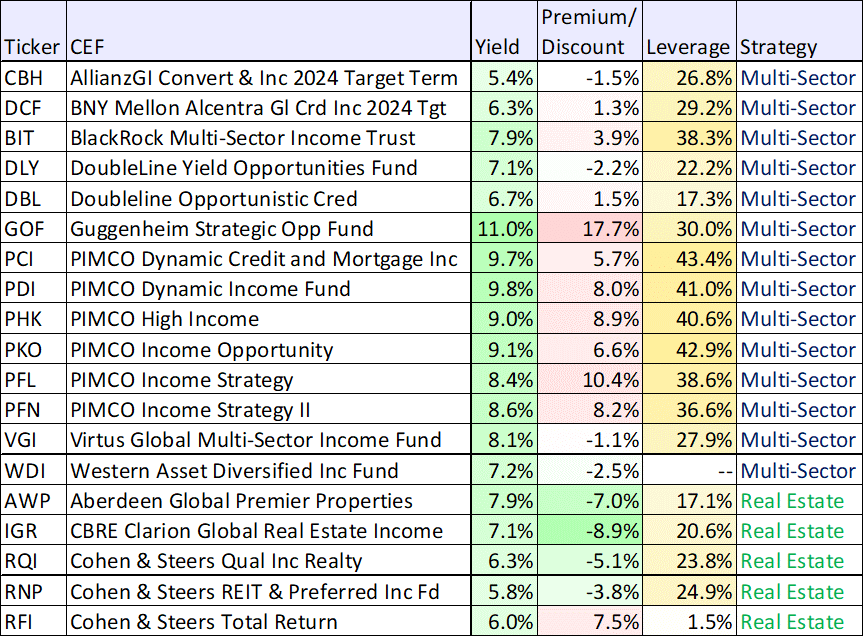

For a little more perspective, here is a chart from our article back on October 9th showing most multi-sector bond CEFs actually trade at a premium (something that is less attractive in our view). DLY is still a relatively new CEF, and we expect the discount to eventually sway to a premium (a good thing for current investors).

Use of Leverage

As mentioned, CEFs are attractive vehicles for portfolio managers to use leverage (or borrowed money) to magnify returns (because they don’t have to deal with margin call risks generated by fund inflows and outflows). And leverage can be really good in the good times (because it magnifies returns), but bad in the bad times (i.e. when the market goes down) because it can magnify losses.

DLY currently uses around 22.4% leverage, which we view as attractive because it is enough to make a positive long-term difference, but not so much to create difficult volatility risks (for perspective, many popular PIMCO CEFs generally have around 40% leverage).

Rising Interest Rates and Inflation

Many investors are wondering if now is a good time to invest in bonds, considering high inflation and the expectation of rising interest rates. Generally speaking, bond prices fall when interest rates rise. However, if you if you are in search of high income, this fund is extremely likely to keep paying it (based on its underlying high-income-producing holdings). Furthermore, it’s extremely difficult predict interest rate moves, and realistically it seems the US can’t afford to raise rates too high anyway because it will create a crushing impact on the economy because the amount of interest it would have to pay on its own treasury bonds. Nonetheless, we like that DLY’s duration breakdown (a measure of interest rate risk) is well-spread across timeframes (see early table) thereby reducing the impact of interest rates changes.

Sources of Income

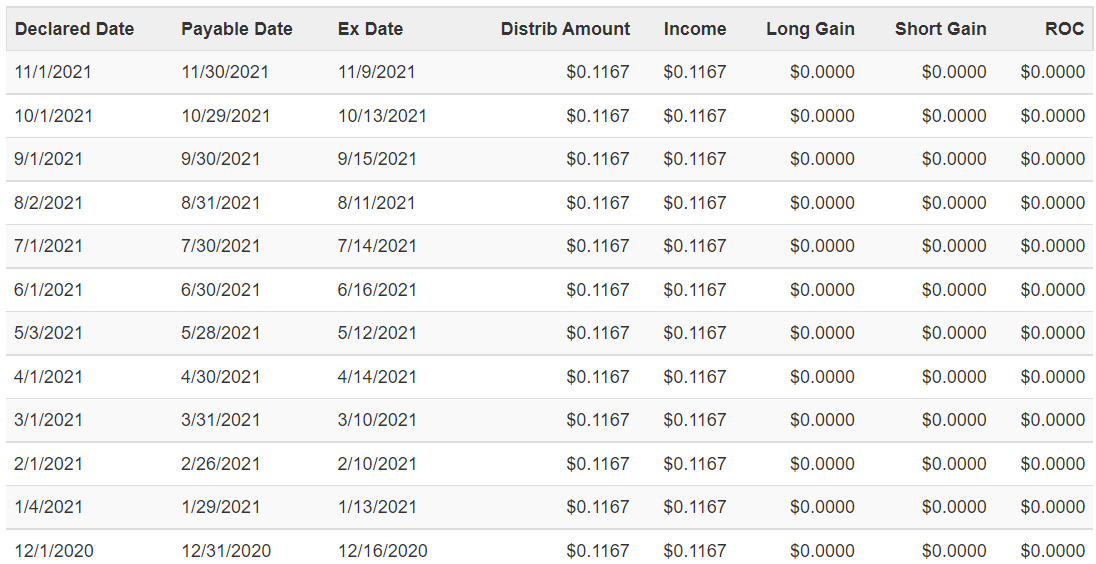

Another important consideration when investing in closed-end funds is the source of income. For example, income can come from interest payments on bonds, capital gains (long-term or short-term) and a return of capital. These differences can cause different tax impacts on you as the investor (for example, a return of capital can cause your cost basis to fall, thereby increasing your tax bill if/when you decide to sell). As you can see in the following table, all of DLY’s income payments have come from actual income (since inception) which is an attractive quality (it’s an indication of health).

Conclusion

If you are an income-focused investor, it can still make a lot of sense to invest in high-income bond funds (such as DLY) despite fears about rising interest rates and inflation. Realistically, it would be extraordinarily difficult for the US fed to raise rates too much (because of the crushing negative impact on increased interest expense on US treasuries). And even if rates are increased, DLY is well-diversified across bond maturities and duration (thereby reducing the impacts), and it will very likely continue to pay high income (and deliver strong total returns) regardless.

We like DLY in particular, for the big monthly income, strong management team and the discounted price. We currently own shares of DLY in our Income Equity portfolio.