Bonds are boring, right? Not so fast. In the last year, bond yields have risen dramatically. In this report, we share details (opportunities and risks) on 5 different bond strategies (currently yielding 5% to over 13%) for income-focused investors to consider. Let’s get right into it…

1. 1-Year U.S. Treasuries, Yield 4.6%

A year ago, a 1-year U.S. treasury bill (bond) yielded approximately 0.0%. Now it yields around 4.8%. That is a shockingly big number to “savers” who have been complaining since the Great Financial Crisis (in ‘08-’09) how the Fed was screwing them over by holding interest rates artificially low. And U.S. treasuries are 100% guaranteed by the full faith and credit of the U.S. government (i.e. they can just tax people and/or print more money to make sure you get paid back in full). If you are a highly risk averse investor, a 1-year treasury bond is probably a lot better than the interest rate you’re getting in you checking, savings and/or money market accounts.

2. Vanguard Total Bond Market ETF (BND), Yield: 2.7%

Vanguard is famous for low-cost passive investment strategies. And this particular ETF fits that bill as it is designed to basically invest in the total U.S. investment-grade bond market (it has over 17,000 holdings, including treasuries, corporate and international dollar-denominated bonds) for an annual fee of only 0.03%.

You might expect this strategy to yield higher than US treasuries because its holding are slightly riskier than a U.S. treasury—but it doesn’t. The main reason for this is because it has interest rate risk. As you know, when interest rates rise, bond prices fall. And this fund has an effective maturity of over 8 years (and a duration of over 6) which means as bond prices keep rising, the price of this fund will fall. That’s basically what has been happening to this fund all year, as you can see in the following chart (this has been an unusually terrible yield for longer-term bonds as the fed keeps raising interest rates).

Importantly, this interest rate risk (i.e. the falling ETF price, as you can see in the chart above) highlights another advantage of the 1-year treasury in our previous example. Specifically, because it matures in the 1-year, the treasury has dramatically less interest rate risk price volatility, and if you hold it for the full one year, you are guaranteed (by the U.S. government) to get paid in full.

At risk of getting too detailed, another risk for the BND ETF is that is has cash inflows and outflows (as investors buy and sell shares) and this can force Vanguard to sell bonds at undesirable prices before the mature. On the other hand, if you buy the 1-year treasury then YOU get to decide when to sell and that works to your advantage (again, if you hold to maturity you get paid in full—guaranteed). Plus the treasury is exempt from paying state and local taxes (if you hold it in a taxable account), unlike some of the corporate bonds in BND.

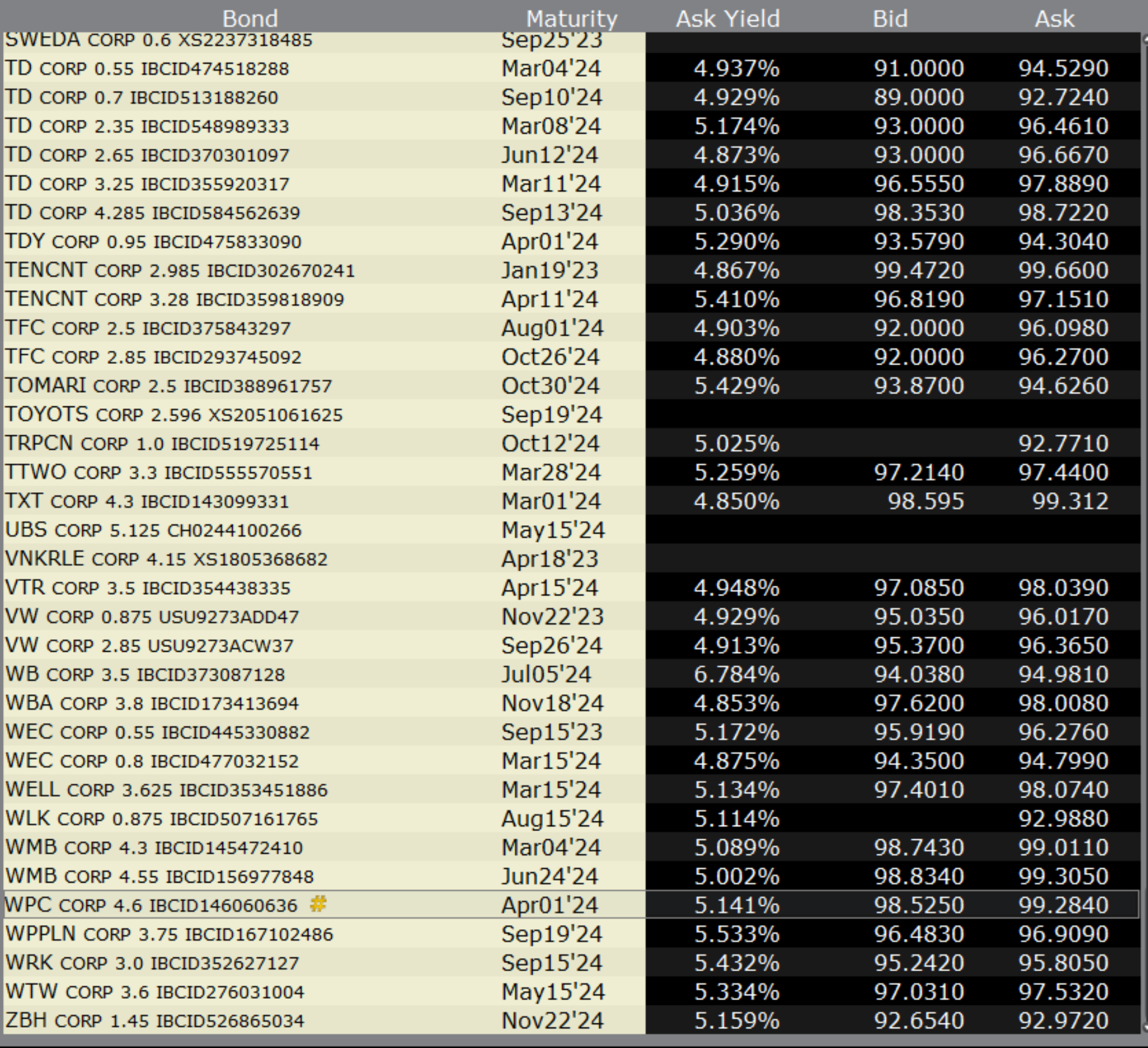

3. Individual Corporate Bonds, Yield: 4.8% to 6.8%

If you want to avoid the risks of a bond fund (such as BND), you might also consider investing in individual investment-grade corporate bonds, currently yielding slightly more than treasuries. For example, you can see the list of yields on a variety of corporate bonds (maturing within the next 1-2 years) in the following table.

Each of these bonds is guaranteed by the company that issued them, and by constructing a portfolio of corporate bonds, you can reduce the risks while keeping the yield high. Plus, if you hold them to maturity—you don’t necessarily have to worry about the price volatility associated interest rate moves (again, as long as you hold to maturity, the issuer guarantees you get paid in full). And if you select individual corporate bonds with longer maturities, the yields go even higher.

4. Business Development Companies, Yields: 5%-13%

Although they trade as public equities, BDCs essentially provide capital (mostly loans) to companies that need to borrow. And BDCs can offer some highly attractive yields. Here is a recent article we wrote (with a lot of BDC data and analysis) to give you an idea of the high yields BDCs can offer.

BDCs are different than bonds or bond funds because they are essentially underwriting each “loan” they issue. This takes more time and operational effort, but it can also offer some very attractive opportunities. BDCs are similar to a bond fund because their balance sheets generally consist of a book of many loans.

Part of the way BDCs get their yields so high is by lending to riskier companies (but a lot of this risk is reduced through diversification—i.e. they make a lot of loans) and through leverage (BDCs do a little borrowing of their own—at lower rates—so they can turn around and lend out at higher rates).

BDCs are absolutely benefiting from higher interest rates, and they currently offer some unusually attractive opportunities. Check out our recent detailed article on BDCs here.

5. Bond Closed-End Funds, Yields: 5% to 13%+

Bond closed-end funds (“CEFs”) are similar to bond ETFs, but with some important differences. For example, PIMCO offers a variety of popular bond CEFs that are actively managed (rather than passively buying the entire market, the management team actively selects the opportunities they see as most attractive).

Bond CEFs also often use leverage (borrowed money) to magnify returns. This can be helpful in the good times, but risky in the bad times (like this year). Bond CEFs are typically limited to a maximum of 50% leverage (1.5x their book value) by regulation.

Bond funds also charge higher fees (often around 1% management fee, plus more for expenses). In some cases, these higher fees can be acceptable because firms like PIMCO have access to bonds ordinary investors do not, and because PIMCO has much more discipline in managing leverage and this can reduce some of that risk.

We recently wrote in great detail about Bond CEFs (including sharing a lot of valuable data) and you can read that report here.

X. Mortgage REITs, Yields: 7% to 19%+

Stepping even further out on the risk-reward lending spectrum, Mortgage REITs can offer even higher yields. Mortgage REIT strategies can vary widely, but a lot of them basically invest in a portfolio of mortgage-backed bonds (for example, AGNC investment Corp (AGNC) and to a slightly lessor extent Annaly Capital (NLY) both own Agency Mortgage-Backed Securities). A strategy of investing in mortgage bonds guaranteed by US agencies (such as Fannie Mae) sounds safe—and it is—but mortgage REITs apply very high amounts of leverage, or borrowed money—thereby making them risky.

For example, Vanguard’s bond fund uses no leverage, BDCs leverage their book values typically by 1.2 times, Bond CEFs leverage up to 1.5 times, and mortgage REITs leverage their book values by 5x to 7x or more! This high borrowing by mortgage REITs can create incredible returns in the good times, but incredibly bad returns (and very high risk) in the bad times (like this year).

Some investors make the argument that mortgage REITs are excellent trading securities (suggesting they have the ability to get in and out of their positions at the right time). There may be some truth to this strategy (but it is risky) and from a long-term standpoint—mortgage REITs are NOT attractive investments to us (simply because they are so risky that they end up permanently damaging their book value every time the market gets volatile—like this year).

We recently wrote more about mortgage REITs (and shared a lot of data on them) in this report.

The Bottom Line

Bonds are just loans, and when you make a loan you should expect to get your capital returned plus interest. Interest rates have risen dramatically this year, and that has created a lot of price pain, but also higher yields going forward.

Generally speaking, we do NOT like mortgage REITs, but we do like individual bonds (such as treasuries and corporates) depending on your strategy, tolerance for risk and personal goals. Bond closed-end funds (such as those offered by PIMCO) can also be attractive considering they have such strong track records of paying consistent high income.

At the end of the day, you need to select an investment strategy that is right for you (based on your own individual situation and goals). Disciplined, goal-focused, long-term investing is a winning strategy. Be smart. Stay focused on your long-term goals.