Novo Nordisk (NVO) is a global leader in diabetes and obesity care, and its shares are down 50% since peaking in June 2024 (due to competition, pipeline setbacks and political uncertainty). However, the underlying fundamentals appear compelling. This report reviews the business, growth, risks, valuation and capital allocation, and then concludes with my strong opinion on investing.

About the Business:

Founded in 1923 and headquartered in Denmark, Novo Nordisk is a pharmaceutical giant (~$290B USD market cap) with roughly 72,000 employees across 80 countries (and with products marketed in 170 countries)

Novo Nordisk operates in two primary business segments:

Diabetes and Obesity Care: This segment represents over 93% of Novo Nordisk’s total revenue, and includes insulin products and GLP-1 receptor agonists (i.e. Ozempic for diabetes and Wegovy for obesity). Novo Nordisk has a ~34% share of the $80B diabetes treatment market and roughly half of the $15B insulin market. GLP-1 drugs, particularly Ozempic and Wegovy, have driven recent growth due to their efficacy in diabetes management and weight loss.

Rare Disease: This smaller segment focuses on treatments for conditions like hemophilia and growth hormone deficiencies, and contributes less to overall revenue (but adds some diversification to the company’s portfolio).

Profit Drivers:

The GLP-1 portfolio (primarily Ozempic and Wegovy) is the primary profit driver, fueled by growing demand for diabetes and obesity treatments. For example, in Q1 2025, Novo Nordisk reported 18% sales growth and 20% operating profit growth, with a 35% net income margin and 70.38% return on equity (placing it among the highest in the pharmaceutical industry).

Continuing Growth:

Novo Nordisk’s high-growth trajectory is being driven by several factors:

Market Leadership (in diabetes and obesity drugs): The company’s dominance in diabetes and obesity, combined with growing prevalence of these conditions, is supporting long-term demand growth. The obesity treatment market is expanding particularly quickly, with Wegovy benefiting from increasing acceptance of GLP-1 therapies.

Pipeline Innovation: Novo Nordisk is investing heavily in next-generation therapies, including amycretin (a promising obesity drug that showed positive early results in January 2025). Also, Ozempic’s potential in treating opioid use disorder and kidney disease could open new revenue streams.

Manufacturing Expansion: To meet GLP-1 demand, the company is scaling up production capacity, with planned capital expenditures of DKK 65 billion in 2025 (i.e. ~$9.5B USD).

Risks:

Of course Novo Nordisk also faces very real risks that investors should consider, such as:

Competition: Eli Lilly’s (LLY) Zepbound has gained traction, and has the potential to erode Novo Nordisk’s first-mover advantage in obesity drugs. And the exit of CEO Lars Fruergaard Jorgensen in May 2025 (on concerns of losing market share to Lilly) underscores this risk.

Pricing Pressure: A price war in GLP-1 drugs, with Novo Nordisk cutting Wegovy’s price to $499/month through its NovoCare pharmacy, could impact margins negatively. In Q4, declining profit margins were noted (due to price cuts and rising costs).

Patent Expiration: Wegovy’s patent expires in the early 2030s, posing a long-term risk of generic competition.

Regulatory/ Policy Risks: Considering 57% of Novo Nordisk sales are in the US, it’s exposed to policy change risks, such as drug price controls, and political pressure from the Trump Administration’s Secretary of Health and Human Services, Robert F Kennedy, Jr.

Pipeline Challenges: The underperformance of cagrisema (a next-generation obesity drug) in late-stage trials (22.7% weight loss vs. 25% expected) led to a sharp stock price decline, highlighting constant R&D risks for the company.

Valuation:

From a valuation standpoint, Novo Nordisk is increasingly compelling. For example, after declining ~50% over the last year, it now trades at a P/E ratio below 20x, which compares favorably to its main competitor Eli Lilly, as well as other pharmaceutical companies, as you can see in the table below.

Also, Wall Street Analysts covering the shares have recently estimated the shares are more than 50% undervalued (see above), and have dramatic 5-year EPS growth potential.

Further still, as compared to its own valuation metric history (see below), Novo Nordisk shares appear compelling (e.g. the P/E ratio is well below recent averages).

Capital Allocation:

From a capital allocation standpoint, Novo Nordisk is measured and balaced. For example:

Research and Development (R&D): NVO invests heavily in R&D (basically a requirement in the pharmaceuticals industry) to maintain its innovation edge, including a focus on extending patent protection and developing new therapies. Recent trials of amycretin and expanded indications for Ozempic demonstrate the company’s commitment.

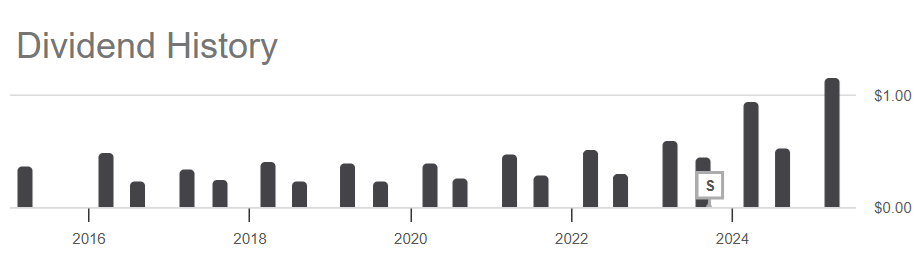

3.4% Dividend Yield: Novo Nordisk has a 29-year streak of dividend growth, raising its 2024 dividend by 21.3% to DKK 11.40 per share. Worth mentioning, the dividend is paid annually in 2 parts.

Share Repurchases: In 2024, the company announced a DKK 20 billion share buyback program, repurchasing 24.8 million B shares (0.6% of share capital) by February 2025. However, the company has no plans for repurchases in 2025, prioritizing R&D and capital expenditures.

Overall, the company’s capital allocation strategy prudently enhances current shareholder value and cash flow, while also supporting long-term growth.

The Bottom Line:

The shares are down 50% over the last year (because of growing competition from Eli Lilly, pipeline setbacks and some regulatory uncertainty), but the company remains dramatically profitable and growing (thanks to diabetes and weight loss drugs) supported by impressive dividend growth and a particularly attractive current valuation. I have no position in Novo Nordisk at this time, but may add shares in the relatively near future.