ServiceNow’s stock has been hammered in recent months, down more than 50% amid broader SaaS-sector fears (that generative AI could commoditize or replace traditional workflow software). However, beneath the surface, the company is thriving (particularly in AI), and the steep share price decline has created a rare entry point for long-term investors.

Overview of the Business

ServiceNow, founded in 2003 and public since 2012, began as a cloud-based IT service management (ITSM) platform but has evolved into the leading enterprise workflow automation company. Its “Now Platform” orchestrates processes across IT, HR, customer service, security operations, and finance in one unified system of record.

Now’s more than 8,800 customers (including 603 that spend over $5 million annually) use the platform to replace fragmented legacy systems with intelligent, automated workflows.

In the AI era, ServiceNow has repositioned itself aggressively as “the AI control tower for business reinvention.” “Now Assist” embeds generative AI directly into workflows, enabling natural-language requests, automated resolutions, and agentic AI that can plan and execute multi-step tasks.

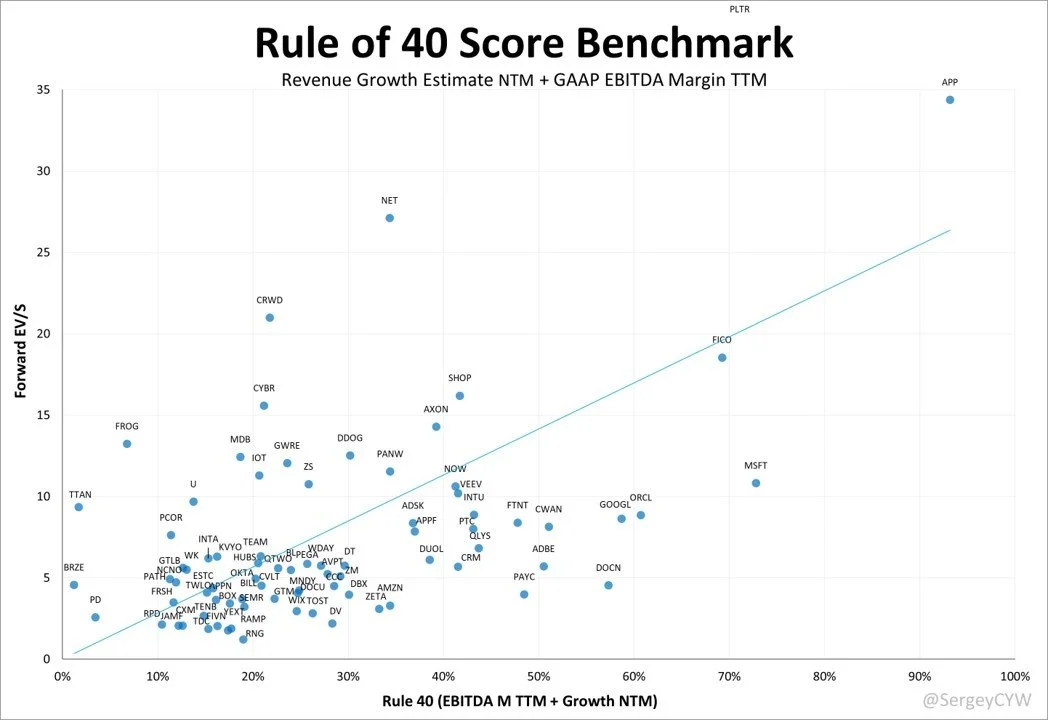

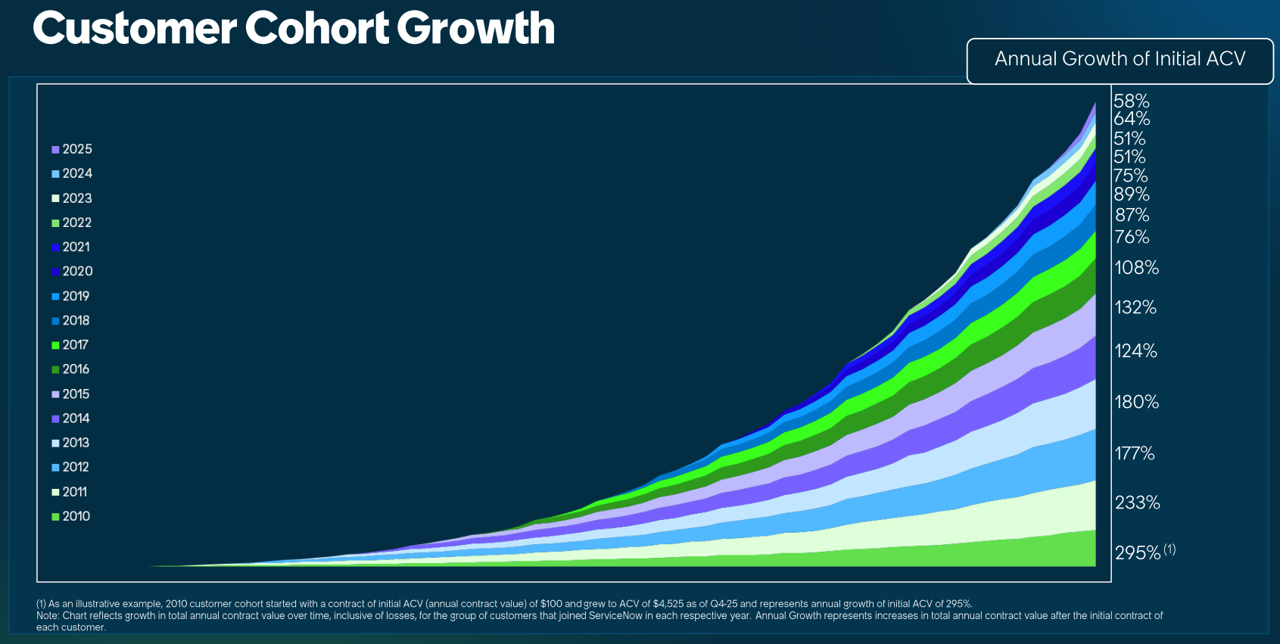

Recent acquisitions (e.g. Moveworks, Armis, Veza) and deep integrations with frontier models have expanded its reach into AI security, data fabric, and agent orchestration. And with 98% gross retention and Rule of 55+ performance (growth plus free-cash-flow margin, see graphic below), ServiceNow has built a durable, high-margin software fortress that is difficult for point-solution competitors to displace.

Growth and Market Opportunity

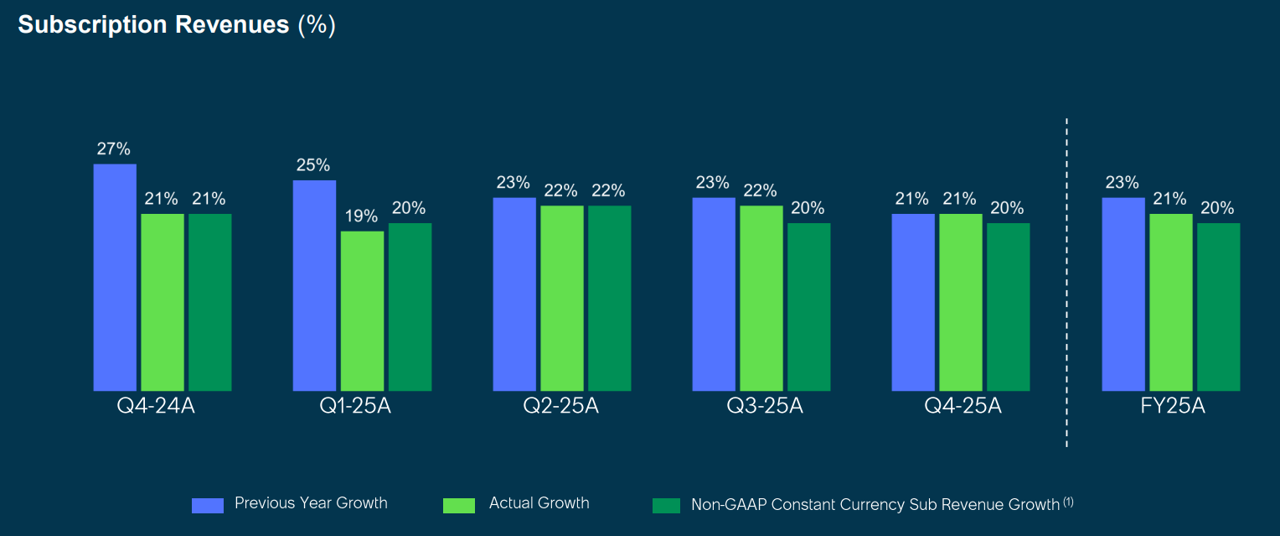

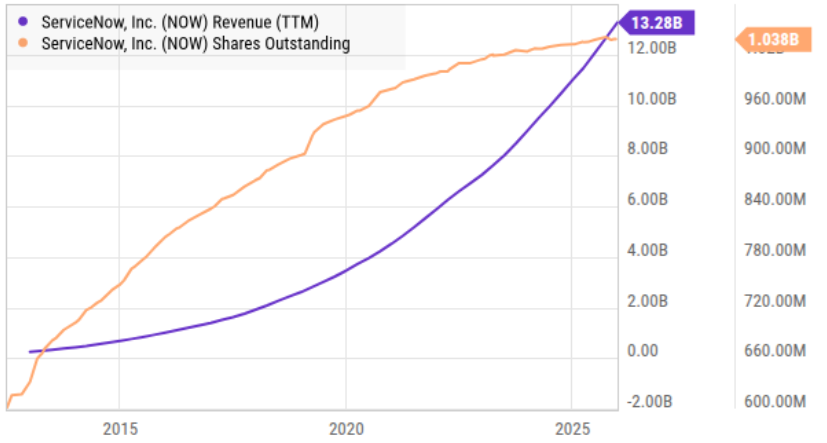

ServiceNow delivered consistent 21% subscription revenue growth in 2025 (see chart below) while expanding non-GAAP operating margins to 31%. For 2026, management guided subscription revenue of $15.53–15.57 billion (19.5–20% constant-currency growth, including a modest 100-basis-point boost from Moveworks). Current remaining performance obligations (cRPO) grew 21% in constant-currency, signaling continued momentum.

However, the real accelerator is AI. “Now Assist” is scaling faster than any prior product launch, with large enterprises deploying it across multiple workflows simultaneously. CEO Bill McDermott calls 2026 “the year of agentic collaboration,” and the company’s AI Control Tower will let enterprises govern thousands of AI agents securely—exactly the governance layer most CIOs now demand.

The addressable market is enormous. Enterprise digital-workflow and process-automation spending already exceeds $100 billion and is accelerating as organizations move from pilot AI projects to production-scale agentic systems.

ServiceNow’s platform sits at the center of this shift, turning AI hype into measurable ROI through workflow orchestration, data unification, and secure execution. With 244 seven-figure net-new deals and expanding multi-product penetration, the company is capturing share in what many analysts view as the largest software opportunity of the decade.

Valuation

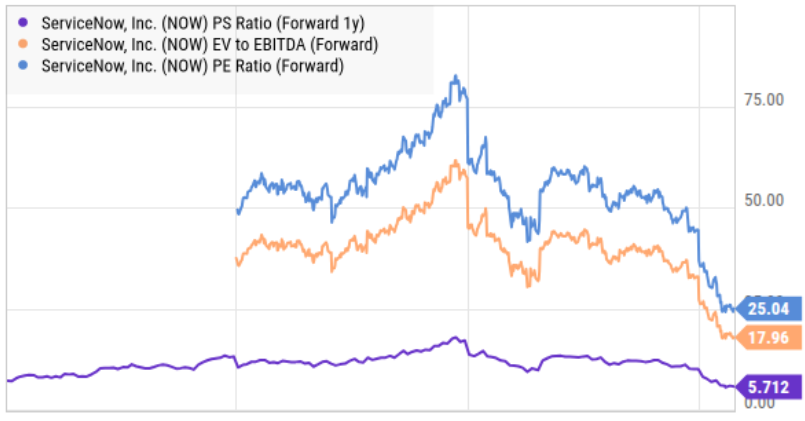

After the deep 50% sell-off, ServiceNow trades at a far more reasonable valuation. Now trading at around $100 per share, the market capitalization is just over $100 billion. And on 2026 guidance, the shares trade at roughly 7× forward subscription revenue and about 45× forward non-GAAP earnings—well below its historical 60–100× multiples and dramatically cheaper than pre-crash levels. You can see more specific valuation multiples in the chart below, including forward price-to-earnings, Enterprise Value to Earnings Before Interest Taxes Depreciation and Amortization and price-to-sales multiple, all of which have compressed.

Now’s profitability basically remains elite with non-GAAP gross margins hitting 80.5% in Q4, operating margins at 31%, and free-cash-flow margins reaching 35% for the full year ($4.636 billion). Management just authorized an additional $5 billion share repurchase (including a $2 billion accelerated program) and lifted the 2026 free-cash-flow-margin target to 36%.

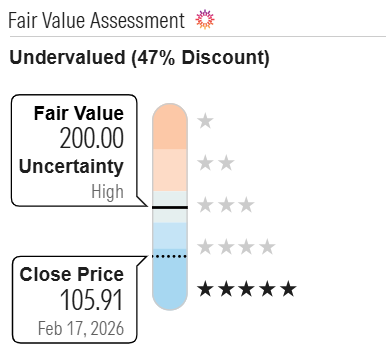

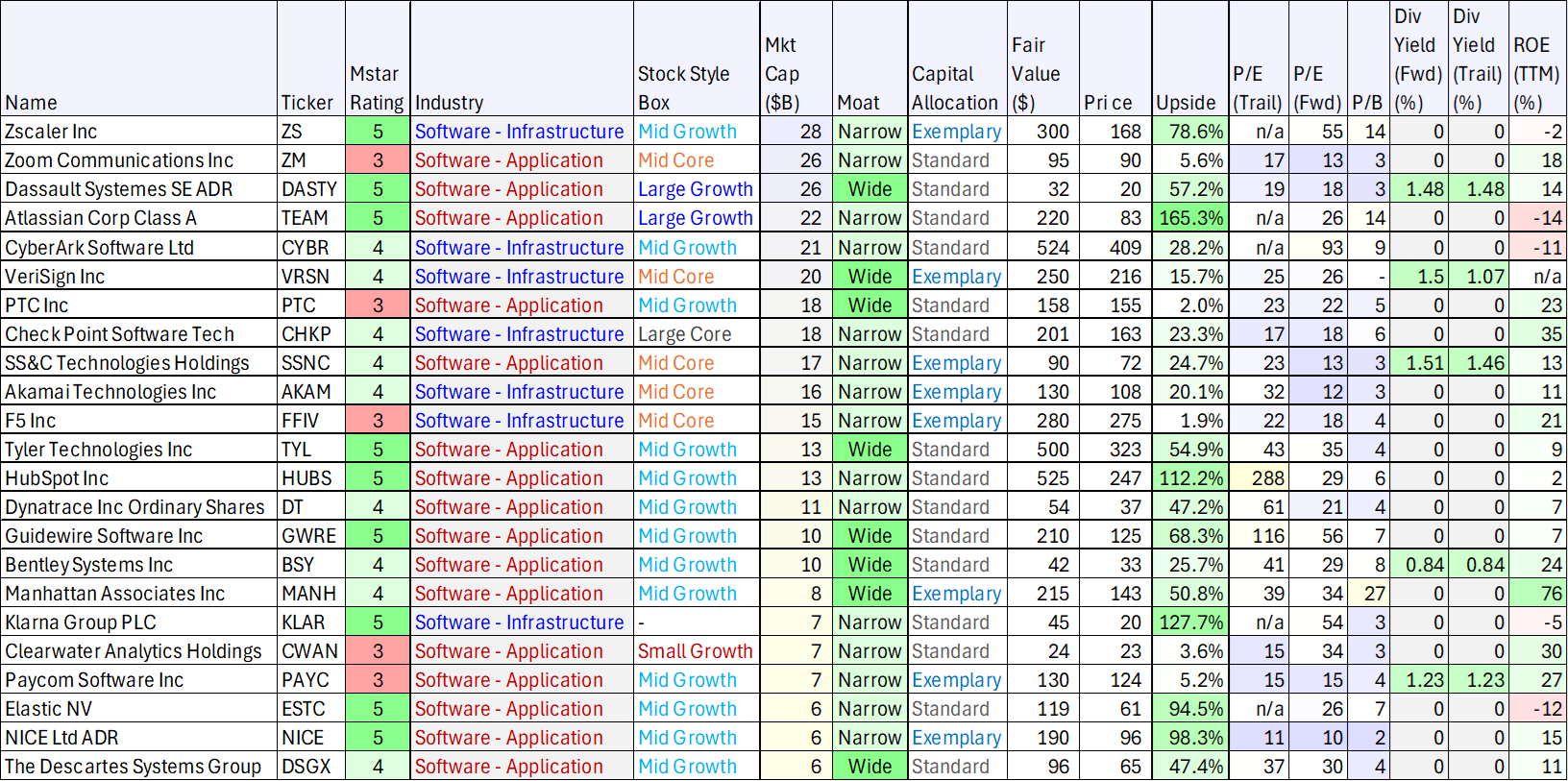

Here is a look at how Morningstar (a notorious Discounted Free Cash Flow modeler) values ServiceNow:

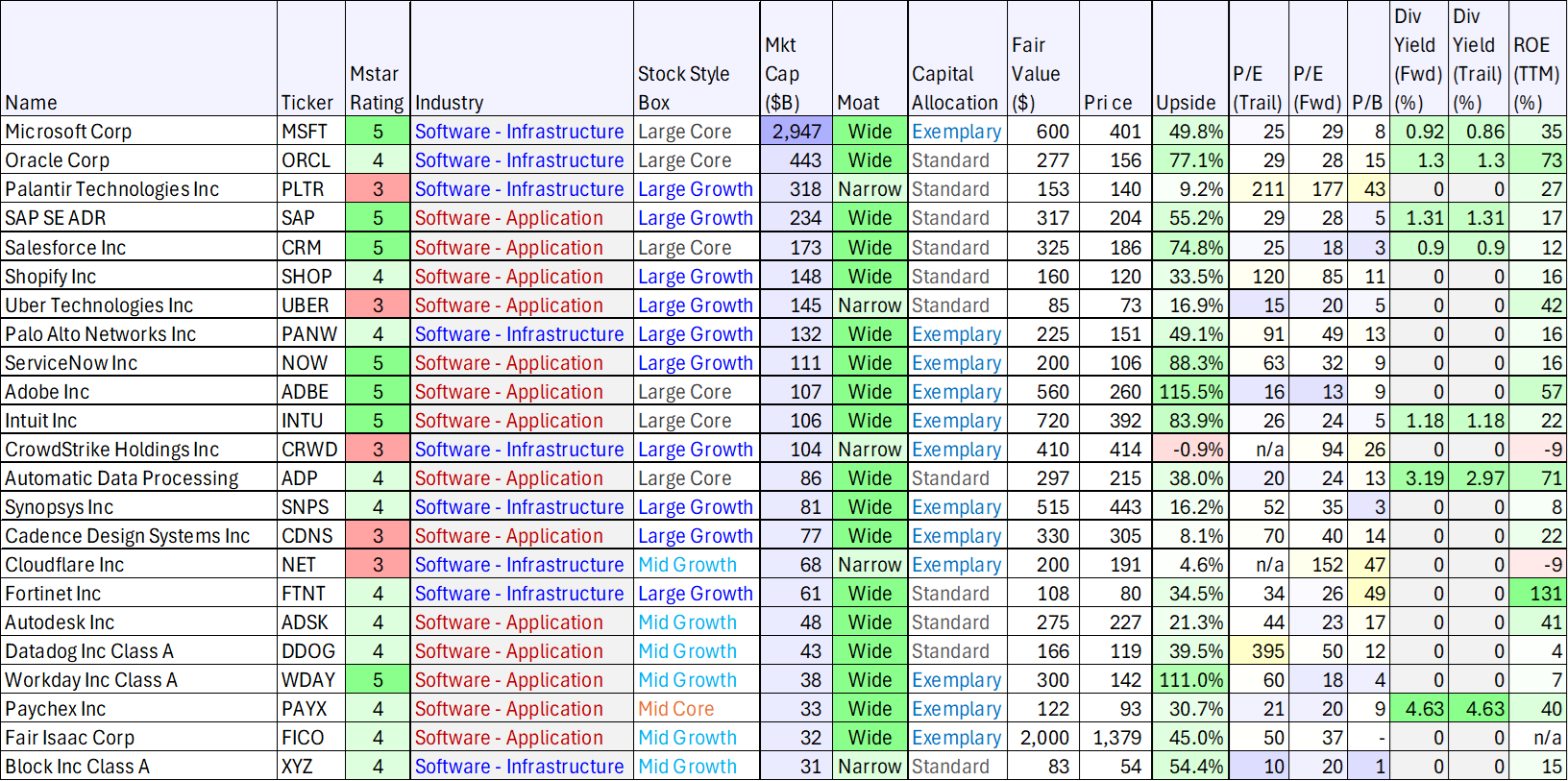

And here is a closer look at Morningstar rates ServiceNow and other top software stocks, also caught up in the recent AI induced so called “SaaS-pocalypse” in terms of star ratings (5 is the best), upside and competitive “moat” (ServiceNow ranks well is all categories).

Insider buying is also a signal with CEO Bill McDermott planning to purchase $3 million of shares personally, and several executives canceled planned sales. The combination of 20% growth, expanding margins, and aggressive capital return at a compressed multiple makes the risk/reward increasingly asymmetric (attractive!).

Risks

No investment is without risk. ServiceNow still carries a premium valuation (as compared to lower margin, lower growth businesses, and any macro slowdown in enterprise IT spending or delayed AI ROI could pressure multiples further.

And of course competition is intensifying with Salesforce (CRM), Microsoft (MSFT), and pure-play AI startups all chasing workflow and agent opportunities. Execution risk exists around integrating recent acquisitions and scaling agentic AI securely.

Finally, broader SaaS volatility could keep the stock range-bound even if fundamentals remain strong.

The Bottom Line:

ServiceNow isn’t becoming obsolete because of AI. Rather, AI is the biggest tailwind in the company’s 20 year history. And at current price and valuation multiples, ServiceNow is one of the more attractive risk/reward opportunities in the entire technology sector. The business isn’t going away—it’s going to the net level.

More specifically, with accelerating AI bookings, pristine financials, a massive secular opportunity, and valuation multiples that have finally come back to earth (as investors have shifted their eyes and dollars to more obvious AI opportunities), ServiceNow offers compelling upside for patient investors. Especially considering NOW’s 2026 guidance is conservative, insider buying signals confidence, and the AI flywheel is just getting started.

For growth-oriented investors comfortable with software volatility, the shares are absolutely worth considering. Long ServiceNow.