Down nearly 20% this year, United Parcel Service (UPS) may look ugly (especially considering revenue is expected to decline), but a closer look reveals a compelling big dividend (6.5% yield) value play (14.8x P/E) with operational and financial strengths, despite the big risks (e.g. tariffs, discontinued Amazon (AMZN) business, rising labor costs and a high dividend payout ratio). In this report, I review the details and conclude with my strong opinion on who might want to consider investing.

Overview

UPS is a global leader in package delivery and supply chain solutions. The company manages a fleet of over 500 planes and 100,000 vehicles to deliver ~22 million packages per day (across more than 200 countries). The business includes US package delivery (ground and express), international package services, and supply chain logistics. And the company has a growing focus on high-margin sectors like healthcare. Important to note, UPS divested its “less-than-truckload” division in 2021 and its Coyote brokerage unit in 2023, aligning with CEO Carol Tomé’s “better, not bigger” strategy to prioritize efficiency and profitability (more on this later).

Attractive Qualities (and Moat)

UPS has a wide economic moat driven by massive scale, network density, and technological investments. For example, its deep infrastructure (including automated sorting and routing systems) creates high barriers to entry (enabling cost efficiencies that competitors like FedEx (FDX) and Amazon’s in-house logistics struggle to match). Also, UPS’s focus on higher-margin deliveries (such as healthcare logistics and international expansion including a new Hong Kong air hub) strengthens profitability. With 490,000 employees and a strong brand, UPS maintains a competitive edge in a consolidating industry.

Current Valuation

UPS shares currently trade at around 14.8 times earnings (i.e. a low P/E ratio in absolute terms and compared to its own history) which is attractive considering the reason why. Specifically, sales are expected to shrink this year as UPS sheds unprofitable Amazon business (which is a good thing for the bottom line) and due to tariff concerns (which appear increasingly behind us).

As you can see in the table, the 28 Wall Street analysts covering the shares rate them a “buy” (1.97 on a scale of 1 to 5, with 1 being the best) and suggest the shares are currently 12.8% undervalued. However, when you factor in the additional returns from the dividend, combined with the company’s stable profitability, UPS shares are increasingly compelling.

Dividend Safety

UPS currently offers a 6.5% dividend yield, impressive by historical standards and very impressive on a standalone basis (6.5% is a great dividend yield, considering the quality company supporting it).

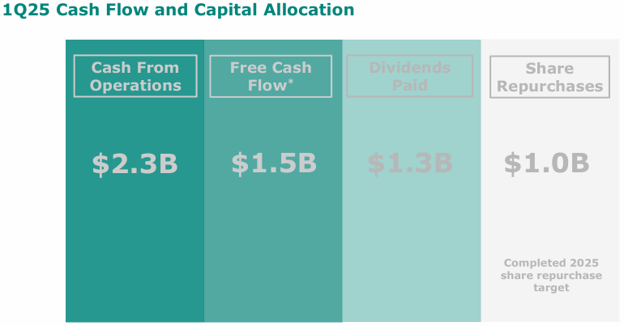

Some investors have concerns because the company paid out nearly 100% of free cash flow in Q1 to support the dividend (see table below), and then exceeded that number when you factor in share repurchases (i.e. it seems unsustainable).

However, factoring in the company’s cost cutting efforts (see graphic below) and healthy balance sheet (strong investment grade credit ratings) the dividend is attractive, and likely to continue its long-track record of increases (and the yield is likely to mathematically shrink as the share price rebounds).

Big Risks

Tariffs have created a lot of uncertainty this year and have also increased costs on international business. For example, operational costs, restructuring costs, lost revenue and margin impacts are all bad for UPS’s bottom line. However, as mentioned, tariff uncertainty appears to be increasingly behind us, a good think for UPS and its investors going forward.

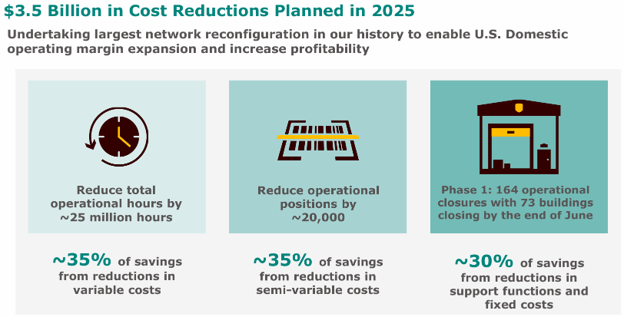

Amazon is another risk factor for UPS. For starters, UPS elected to eliminate significant low-margin business with Amazon, which will reduce UPS’s overall revenue by 5-6% in 2025. The good news is this was low margin (often unprofitable) business, so eliminating it will be good for the bottom line, even if some investors reacted negatively. More specifically, UPS expects to reduce the volume of packages it delivers for Amazon by 50% by the second half of 2026 (enabling UPS to focus on the delivery of heavier packages traveling a longer distance), and this shift is expected to result in a workforce reduction of 20,000, closure of 73 facilities, ~$3.5B in savings for UPS. Worth mentioning, CEO Carol Tomé explained on the most recent UPS earnings call

“Amazon is our largest customer, but not our most profitable customer,” and that the “Amazon volume we plan to keep is profitable and is healthy volume.”

Labor Costs are another big risk factor. For example, a 2023 Teamsters union contract (which increased wages and benefits) contributed to a decrease in 2024 margins, and continues to pressure labor costs (and threatens operations disruptions), particularly in the US.

Conclusion

Amazon isn’t some disruptive high-growth technology stock. But it does offer a very large 6.5% dividend yield (supported by healthy cash flows) and an attractive low share price (as the market incorrectly reacts to a good revenue decrease and tariff risks that are increasingly behind us). If you are looking for a big-dividend value play with attractive share price appreciation potential too, UPS is absolutely worth considering.