Year-to-date performance across the S&P 100 continues to highlight a powerful market rotation—one driven less by broad bullish or bearish sentiment and more by shifting narratives, earnings durability, and valuation resets. Let’s take a look at year-to-date performance for energy, mega-caps and software—highlighting a select group of extreme performers—with lots of volatile big risks and increasingly tempting opportunities.

1. Energy’s Leadership: Cash Flow Meets Macro Tailwinds

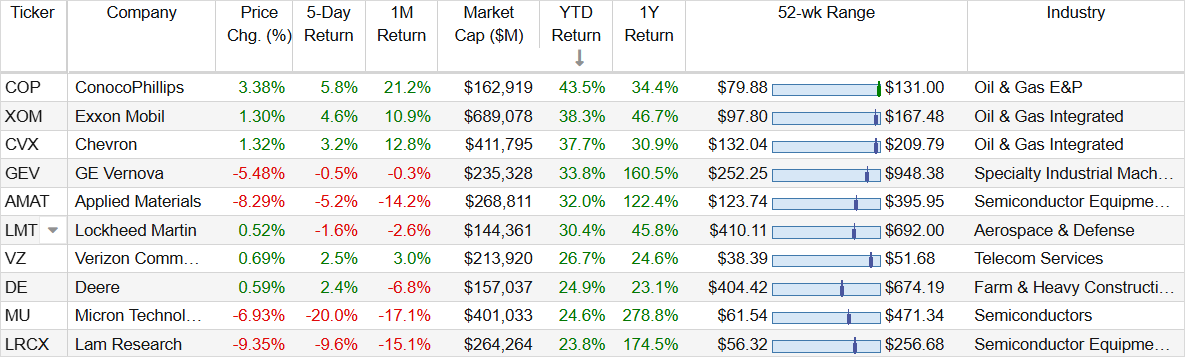

Energy names dominate the top performers this year, led by ConocoPhillips, Exxon Mobil, and Chevron, as you can see in the table below. While the headline story is strong oil prices, the deeper driver is capital discipline.

For example, Exxon Mobil’s continued outperformance reflects not just pricing, but execution—its Guyana production ramp, for example, and its refining strength have both driven better-than-expected earnings and free cash flow. Meanwhile, ConocoPhillips has leaned heavily into shareholder returns, maintaining aggressive buybacks and variable dividends that directly tie investor upside to commodity strength.

And then Macro Forces are doing the rest:

OPEC+ supply management has kept a floor under oil prices.

Geopolitical instability (from Eastern Europe to the Middle East) has added a persistent risk premium.

Underinvestment in supply over the past decade is constraining production growth.

Those 3 are a recipe for the higher prices we are seeing.

And beyond oil, GE Vernova till stands out. Its strong YTD performance is tied to the global electrification push, including grid upgrades and renewable integration. This reflects a broader theme: energy isn’t just about oil—it’s about infrastructure—and GE Vernova has been in the right place at the right time (and it still only trades at 6.3x sales—not bad for a company growing revenue at 17 this year and 14% next year with a healthy 12.8% net margin).

2. Mega-Caps: Great Companies, Tough Comps

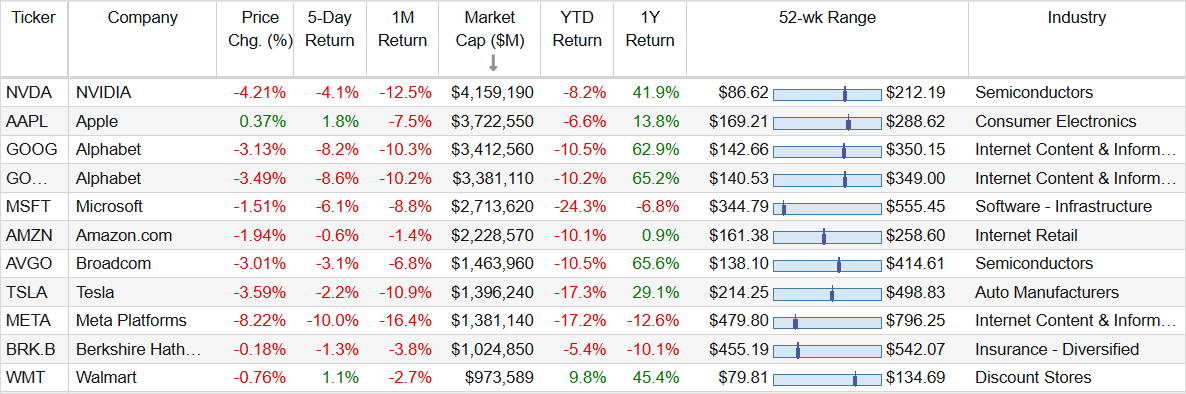

The largest stocks—Nvidia, Apple, Microsoft, and Amazon—are no longer carrying the market the way they did in prior years (as you can see by the sea of ytd red in the table below).

Take Nvidia: despite still delivering strong growth, the stock is down YTD as expectations had simply run too far ahead. Even minor signs of AI spending normalization or margin pressure have triggered pullbacks. This is a classic case of “great company, lofty-market-expectations.” Notable however, Nvidia trades at a 0.7x price-to-earnings/growth ratio (anything below 1.0 is impressive, especially considering Nvidia’s 5-year EPS growth estimate is north of 30%—wow!).

Similarly, Apple’s softer YTD reflects slowing hardware growth, particularly in iPhones, and increasing scrutiny over its China exposure. Microsoft, while fundamentally strong, has also faced pressure as investors reassess how quickly AI monetization will translate into sustained earnings growth.

Even Meta Platforms and Tesla have stumbled, the latter dealing with EV demand concerns and pricing pressure.

The common thread: valuation compression after extraordinary runs. These companies aren’t broken (they’re still great)—but they’re no longer being repriced upward every quarter.

3. Software Selloff: AI Disruption or Overreaction?

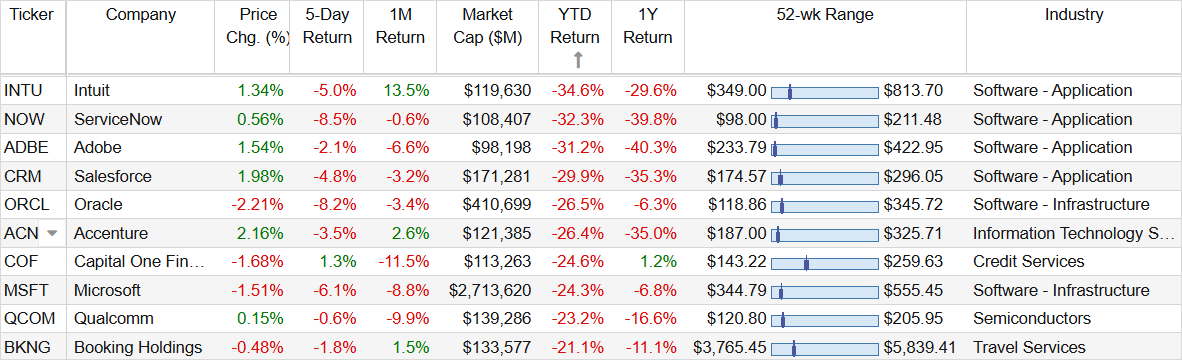

The most striking weakness lies in enterprise software: Intuit, ServiceNow, Adobe, and Salesforce are all down sharply YTD, as you can see in the table below.

Adobe is a particularly telling case. Investor concerns have centered on generative AI commoditizing creative tools, raising fears that pricing power could erode over time. Similarly, ServiceNow’s decline reflects worries that AI could automate workflows more cheaply, threatening its core value proposition. Of these two, ServiceNow appears on stronger footing (even though both are extremely financially sound).

Intuit has faced questions around AI-native competitors potentially disrupting tax preparation and small business tools, while Salesforce continues to battle slower enterprise spending alongside margin pressures.

But here’s the nuance: many of these companies are still growing, still profitable, and actively integrating AI into their platforms. The market is pricing in disruption risk ahead of clear evidence. If/when the narrative shift, these very profitable business have strong financial footing to build on (i.e. the selloff is likely overdone—but time will tell).

The Bottom Line: Rotation Creates Opportunity

This market is not bearish—it’s rotational. But the implication isn’t simply to chase what’s working.

Yes, energy and industrials are benefiting from strong fundamentals and supportive macro trends. But they are also increasingly well-owned and well-understood trades.

At the same time, mega-cap tech and software are undergoing valuation resets, not necessarily fundamental breakdowns. That opens the door for a more balanced approach:

Stay exposed to cash flow leaders in energy and infrastructure

Be selective in mega-cap tech, focusing on reasonable entry points

Consider contrarian positions in beaten-down software, especially where AI risk may be overstated

The real opportunity in a rotational market isn’t just identifying winners—it’s recognizing when losers are being mispriced.

Because in markets like this, today’s laggards often become tomorrow’s leaders—once expectations reset and reality proves more resilient than feared.