Business Development Company (BDC) stock prices have sold off sharply in 2026, but this isn’t random volatility—it’s a deliberate market repricing. Investors are adjusting expectations for a sector that benefited from post-GFC tailwinds—that are now shifting. The key question now is whether the selloff is overdone—or an emerging opportunity.

Despite Recent Weakness, BDCs Strong Over the Previous Decade

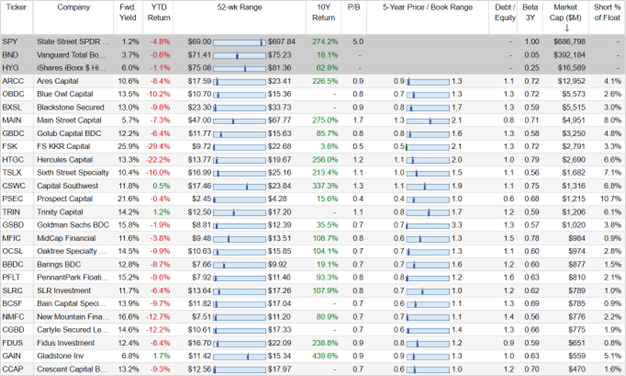

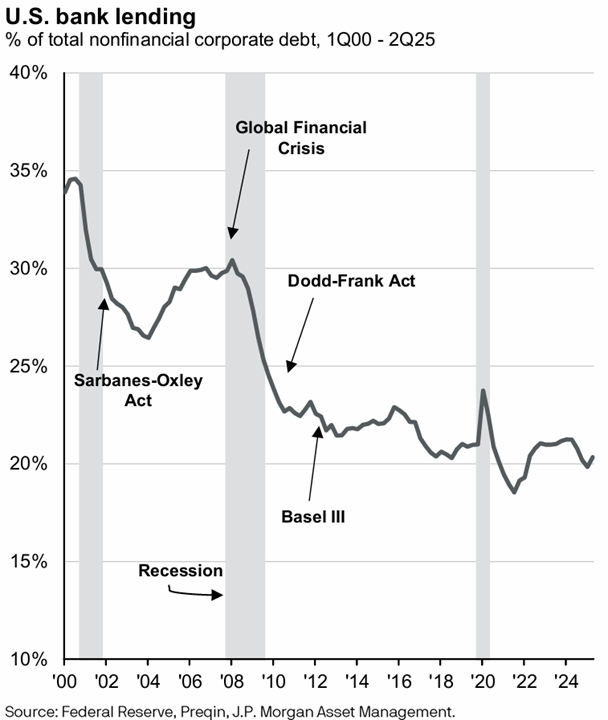

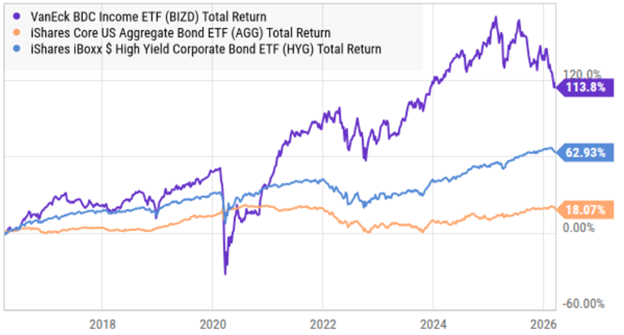

As you can see in the table above, BDCs have posted healthy gains over the last decade as compared to investment-grade and high-yield bonds. And one of the biggest reasons for this (as you can see in the chart below) is because BDCs have benefited from a post-GFC regulatory environment that forced banks to de-risk of BDC-type loans, and thereby creating lots of low hanging fruit lending opportunities for enterprising BDCs.

The Macro Script Has Now Flipped

However, as all good investors know, strong past performance does not guarantee future success, and the macro environment has now shifted—and it doesn’t favor BDCs quite so much.

Competition has grown, as the extremely niche BDCs space has become less so over the last decade as more BDCs now compete for attractive lending opportunities. Not to mention big bank lending restrictions are now relaxing (creating more competition for BDCs) as reserve requirements are exceeded and the GFC is further in the rearview mirror.

Credit Risk Is No Longer Theoretical as credit quality concerns have emerged after years of being largely ignored. BDCs lend to middle‑market companies that are more vulnerable to economic stress and refinancing risk. Rising use of payment‑in‑kind (PIK) structures—often a stress signal—is increasing investor scrutiny, and some funds are already pricing in elevated credit concerns.

Discounts to NAV Signal Trust Issues as many BDCs are trading at significant discounts to net asset value (see price-to-book values in the earlier table), indicating that investors may not trust the current portfolio marks. Because private credit valuations lag actual market conditions, this disconnect can widen uncertainty and incentivize selling.

AI Exposure Is an Underappreciated Risk for BDCs as a meaningful share of private credit and direct lending, including BDC portfolios, has exposure to software and technology sectors. With accelerating uncertainty due to artificial intelligence disruption, investors worry this exposure could lead to higher defaults or weaker cash flows than previously expected.

Sentiment Has Turned on Private Credit as investor sentiment has softened dramatically. After years of strong inflows, signs of fatigue are visible with slowed issuance, redemption pressures, and cautious positioning from asset managers—a dynamic that disproportionately affects liquid vehicles like BDCs.

Interest Rates also create challenges as BDC earnings are highly sensitive to rates because most portfolios are floating‑rate. As rate cuts move from expectation to reality, yields on new and existing loans are compressing, directly pressuring net investment income and dividend coverage.

Not All BDCs are the Same

Obviously, BDCs vary widely in terms of who they lend to (e.g. Main Street versus Silicon Valley, for example), but they also vary in terms of competitive advantages like size (financial wherewithal and resources) and borrower relationships (strong networks go a long way). However, all BDC are often treated equally, for example they’re almost all down this year—despite their differences.

Buying Opportunities

Separating the wheat from the chaff matters more now than at many other points in BDC history, and it can make a lot of sense to own BDCs with competitive advantages as described above. As such, the following BDCs are attractive, considering their strength and price discounts as compared to their normal price-to-book values—even after considering the market wide rerating going on (i.e. BDCs may trade at a bit lower valuations going forward as compared to their recent history):

Ares Capital (ARCC) is the blue-chip leader in the space with better financial wherewithal and wider networks than basically everyone else. Trading below book value, Ares is a buy.

Hercules Capital (HTGC) with a focus on more disruptive and technology-focused borrowers, Hercules should be a bit more volatile than peers, but it also has more upside considering the deal structures (high rates and equity warrants). Still trading a bit above book value, but below its historical norm, Hercules is a buy if you can tolerate a little more price volatility along with your big dividend yields.

The Bottom Line on BDCs

We may see an increasing shakeout in the BDC industry as macroeconomic conditions are not as strong as they once were. However, even after adjusting for market sentiment and arguably permanently lower price-to-book values (as compared to recent history), some BDCs are currently trading at attractive prices (such as Ares and Hercules).

Depending on your goals as an investor, if you are looking for some attractive high income to add as one part of your broader diversified portfolio, select BDCs are currently attractive and absolutely worth considering for investment.