SoFi is a millennial-focused financial services company that’s up more than 200% in the last year. And the gains are not just because of social media hype, but also due to SoFi’s impressive fundamental growth (as the company capitalizes on millennials’ growing distrust of traditional finance). This report reviews SoFi’s powerful “product differentiation” strategy, growth opportunities (particularly its latest foray into cryptocurrency and private equity), current valuation and risks, and then concludes with my strong opinion on investing.

About SoFi

SoFi divides its business into three main segments, including Lending, Technology and Financial Services, with respective revenue and profit per segment as shown in the following table (i.e. lending is the most profitable, followed by financial services which is also the fastest growing).

The SoFi Brand: Distrust of Traditional Finance

However, to really understand the business, you need to appreciate the company’s brand focus on millennials (born from 1981-1996), and in particular their distrust of traditional finance.

Having witnessed big-bank bailouts (as the housing bubble burst in 2008-2009) and also have grown up entirely in the age of the internet, Millennials appreciated SoFi’s seamless digital platform (for banking, investing, and lending) whereby branch offices and their parents’ big bank “financial advisors” are completely cut out of the process.

Millennials also appreciate SoFi’s embracement of decentralized finance (or “defi”) such as cryptocurrency (because it disrupts traditional money, which they increasingly don’t trust) as well as new product availability (such as new initiatives to make private equity investments available to the masses instead of only the ultrawealthy as is traditionally the case). More on this later.

SoFi’s Product Differentiation Strategy

SoFi differentiates itself (and thereby is growing its competitive advantage, or moat) not on cost leadership (they are not necessarily the lowest cost on anything), but rather on product differentiation. Specifically, SoFi differentiates itself from traditional financial services by offering products that appeal to (and capitalize on) millennials distrust of the legacy system (as described earlier), but also by offering more expansive, comprehensive products than other defi companies (such as Robinhood (HOOD) and Coinbase (COIN)) which focus more narrowly on trading or crypto.

Student Loans: A gateway to long-term high-value customers

Originally known for providing private loans to students at elite universities, SoFi’s product offerings have expanded dramatically, but student loans (including those now beyond just elite universities) continue to be the main initial customer product (that gets SoFi’s foot in the door), but also these student loans are the early relationship gateway into more expansive wide-ranging financial products. Basically, providing student loans allows SoFi to build a relationship with future high earners (before competing financial services firms can get to them).

Current Valuation:

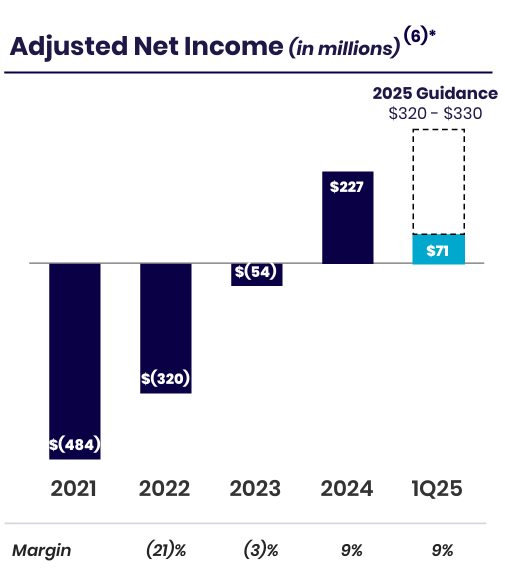

SoFi is bemoaned by traditional valuation analysts for having a very high price-to-earnings ratio (recently over 50x). However, it’s important to note (see graphic below) that the company just became profitable in 2024, revenues are growing rapidly, and economies of scale (and profit margins) are on pace to improve significantly (and arguably make that price-to-earnings ratio much more reasonable than a lot of people suspect).

For some additional perspective, here is a look at SoFi’s revenue growth expectations (very strong) and valuation metrics (arguably more reasonable) versus a variety of loose but differentiated peers and competitors.

As you can see, Wall Street does not love SoFi (they rate it closer to a hold than a buy on a scale of 1 to 5, with 1 being “strong buy” and 5 being “strong sell”). However, what analysts may not be fully appreciating is the long-term and expansive relationships SoFi is building with its very high value (future high earner) millennial customers, especially considering the company’s leadership position in an increasingly changing financial services industry.

And regarding longer-term growth, some estimates suggest SoFi is leading in an $882 billion dollar fintech market opportunity (that is growing at 17% CAGR through 2023) as well as the massive opportunities in lending (i.e. lots of room for SoFi’s continued high growth).

The Risks

Obviously, there are a lot of risks associated with investing in SoFi. Here are some of the big ones that investors should consider.

Meme Stock Status: A meme stock is one that can be driven to extreme highs and lows by social media hype and regardless of underlying fundamentals. And even though SoFi does have healthy and improving financials/fundamentals, it’s still a bit of a meme stock whereby the share price is driven (at least in part) by extreme social media sentiment. Afterall, part of the company’s brand is to play off millennials strong emotional dislike for traditional finance. This can be a good thing (and it is likely part of the reason the current P/E ratio is so high), but it can also be a bad thing and a risk that investors need to keep on their radar.

Private Equity: People often want what they cannot have, whether or not it’s a good or bad thing for them. And SoFi’s latest foray into private equity may be a good example of this. Private equity investments are traditionally only available to the very wealthy and/or institutional investors. But to capitalize on this jealously, SoFi recently announced it would be making private equity investments available to the “little guy” through its new partnerships with Templum, Cashmere, Fundrise, and Liberty Street Advisors.

However, it appears SoFi investors will only have access to secondary offerings (i.e. existing private equity deals and funds the big boys want to exit). So even though the little guy at SoFi may think he’s getting a seat at the big boy table, he may likely be only getting access to the table scraps the big boys are trying to exit (not to mention a litany of private equity characteristics that make it not as attractive as some people think, including high fees, low liquidity and high uncertainty).

Cryptocurrency and Stablecoin: SoFi recently announced that, starting later this year, SoFi members:

“will be able to buy, sell, and hold a selection of crypto currencies like Bitcoin and Ethereum.”

And that

“Over time, SoFi intends to offer stablecoins and a wide range of other services, such as providing members the ability to borrow against their crypto assets, expanding payment options, and introducing new staking features, as well as blockchain and digital asset infrastructure capabilities for other companies offered by Galileo, SoFi’s technology platform.”

While this is exciting news for many supporters of fintech and defi, it also introduces risks, such as potential regulatory burdens as well as likely high costs and expenses that a lot of SoFi members may not be fully considering if and when they participate in such activities.

Further, the idea of stablecoin may be appealing for its ability to bypass traditional banking expenses, but its value is generally pegged to something (such as the US dollar or gold) but not necessarily backed by those things (the stablecoin is only as safe as whatever real assets it is backed by—i.e. stablecoin is a derivative, not the real thing).

High Beta: Not only does SoFi have some meme stock risks, but it is also a high beta stock (you can see its beta is over 2 in the earlier table). This means when the market is going up, SoFi shares can do very well. But if and when the market turns south—SoFi shares can perform very poorly (and this type of stress can create heightened problems for financial services companies in particular, due to leverage and lending book value requirements).

High Valuation: As mentioned, SoFi has a high current valuation as measured by P/E ratio (and other metrics in the earlier valuation table). This means if market sentiment changes, SoFi shares may be at heightened risk of a correction if the valuation multiples contract, even if growth remains robust.

The Bottom Line:

SoFi is an impressive disruptive growth stock effectively capitalizing on fintech opportunities and millennials’ distrust of traditional finance. It continues to release innovative new products (such as cryptocurrency and private equity) beyond just student loans (which remain an attractive first product for the company to get its foot in the door with future high earners).

However, it’s also a high-risk and high-volatility company that investors need to be aware of. I continue to own a significant amount of shares (thanks in large part to the tremendous run-up in price over the last year—it’s up over 200%). However, I am considering reducing my position size (within my prudently concentrated “disciplined growth” portfolio) for risk management purposes and to make room for other even more attractive high-growth opportunities.

At the end of the day, you need to do what is right for you based on your own individual situation. Disciplined goal-focused long-term investing continues to be a winning strategy.