Triangle Capital cut its big dividend this week, and we bought shares shortly thereafter. Following the dividend cut, the stock declined roughly 15%, the yield is now around 10.5%, and we believe the company is significantly undervalued. Specifically, we bought Triangle because of its attractive cash flows, its big dividend yield, its strong internal management team, and its multiple layers of diversification benefits within the Blue Harbinger Income Equity portfolio.

Three Terrific Buying Opportunities

This week’s Blue Harbinger Weekly reviews three of our current holdings that present terrific buying opportunities right now. First, a diversified refining company that recently sold off thus creating an attractive buying opportunity. Second, a revenue-growing juggernaut that likely can’t be stopped for many years to come. And third, a smaller utility company that may soon be acquired. Log in to view all the details, and if you’re not currently a member, consider a subscription.

Williams Partners: Turmoil Creates Opportunity

We believe the market has overreacted to the challenges Williams faces (e.g. low energy prices, counterparty credit/default risk, management reorganization, and rising interest rates), under-reacted to the value it creates (e.g. energy price agnostic fee business, the value of its assets, and its future growth potential), and it could be a valuable addition to the higher risk portion of a diversified, income-focused, investment portfolio.

This 12% Yield MLP is Worth Considering

The main focus of this week’s Blue Harbinger Weekly is an attractive Master Limited Partnership investment opportunity that currently pays big monthly distributions that amount to approximately 12% per year. We review the merits of this MLP in detail, and discuss why income-focused investors may want to consider it (and no it’s not Plains All American). Additionally, we briefly review three of our value stocks that recently reported earnings and have been performing very well over the last month (and why we expect them to continue performing well going forward).

Ladder Capital: Fear Highlights Risk, Creates Opportunity

Ladder Capital an mREIT with a big +9% dividend yield, (~+20% dividend yield if you count the December special dividend). Ladder’s price has fallen 30% in the last year for a variety of reasons (e.g. fears related to commercial real estate prices, rising interest rates, widening credit spreads, decreased CMBS issuance, and increasingly challenging regulations). But we believe this maybe creating opportunity...

This 20% Dividend mREIT is Worth Considering

The primary focus of this week’s Blue Harbinger Weekly is an attractive mREIT investment opportunity that currently pays a +20% dividend yield. We review the merits of this mREIT in detail, and discuss why income-focused investors may want to considering adding it to their diversified investment portfolio (and no, it’s not New Residential). Additionally, we discuss our small cap utilities stock holding that recently gained nearly 20% on talks of being acquired.

Top 5 Blue Chip Stocks Worth Considering

In a continuation to part 1 of our free report (Ten Blue Chip Stocks Worth Considering) this week's Blue Harbinger weekly reviews the remaining (top 5) blue chip stocks on our list. And yes we do own all five of the top five stocks.

Top 5 Big Dividend Investments Worth Considering

In a continuation to part 1 of our free report (Ten Big Dividend Investments Worth Considering), this week's Blue Harbinger Weekly includes the remaining (top) five big dividend investments (we currently own three of them). We also discuss the market's reaction to Fed Chair Janet Yellen's recent comments on interest rates, as well as the continued outperformance of Blue Harbinger's members-only investment strategies through the end of the first quarter (3/31/2016).

Bubbles Bubbling? ETFs, Volatility and Retirees

Some market pundit is always trying to scare investors with talk of the next market bubble and the impending market crash. In this weekend’s shortened Blue Harbinger Weekly (it’s Easter!) we discuss the merits of three such bubbles that have recently been pushed by media pundits: 1) The Smart Beta ETF bubble, 2) The impending VIX volatility spike bubble, and 3) The giant vacuum and market crash to be created by retiring baby boomers.

Business Development Companies: Big Dividends, Differentiated Risks

This week’s Blue Harbinger Weekly reviews a variety of topics including the prospects for high dividend Business Development Companies (see table), our Tsakos options trade (it’s up nearly 100% in two months), the foolishness of those who fearfully sold at the bottom earlier this year (the Dow Jones is actually now positive for 2016), and the continued strong outlook for “value” stocks as we believe their outperformance has only just begun.

Continued Outperformance for Blue Harbinger Stocks

All three Blue Harbinger strategies continue to outperform. This week’s Weekly reviews the performance of the individual holdings within each strategy, and we focus on several stocks in particular that we believe provide terrific buying opportunities right now. And just for grins, here is a fun quote from Charlie Munger.

What a Difference a Week Can Make

Strong jobs data and a rebound in oil prices fueled the S&P 500 2.6% higher last week. Our Income Equity, Disciplined Growth and Smart Beta strategies all outperformed for the week, and they all continue to outperform since inception. Also, our Tsakos options trade is now up 98% since we initiated it on Feb 8th. Next week’s biggest scheduled data release will be crude oil inventories on 3/9, and we believe the stocks in all three of our strategies are set to climb higher. Here are the holdings (and recent performance) for each strategy:

Income Equity Stocks Continue to Outperform

Since its launch in January, the Blue Harbinger Income Equity strategy continues to outperform the S&P 500. As the following chart shows, its holdings are well-diversified across market sectors. Further, the strategy’s dividend yield is well above the dividend yield of the benchmark S&P 500 index. In this week’s Weekly, we review several holdings in particular, and describe why the strategy is positioned for continued outperformance.

Where Will Yahoo! Go To Die?

Yahoo is looking to sell its core business, and the board is excluding CEO Marissa Mayer from the process. In this week’s Weekly, we consider who might actually buy Yahoo and what they’ll pay (spoiler alert: they’re not going to pay much, and they are going to cut costs to the bone). On a separate note, our new big-dividend Blue Harbinger Income Equity strategy is off to a terrific start this year, outperforming the S&P 500 by 2.2% already.

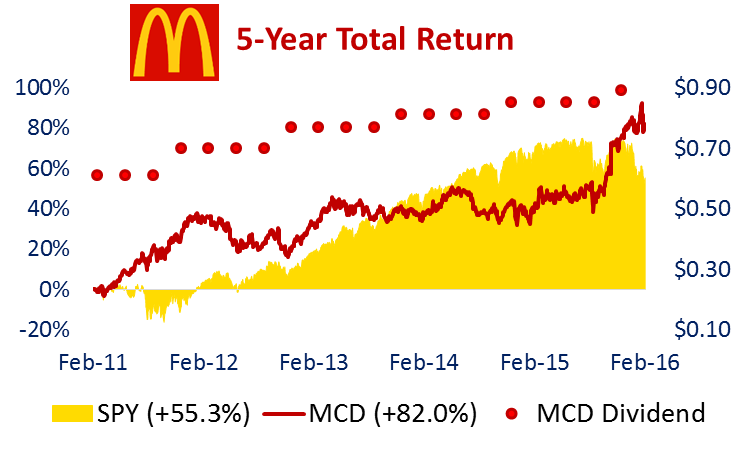

McDonald’s: Weighing the Risks Ahead

McDonald's (MCD) - Thesis

McDonalds (MCD)

Rating: Hold

Current Price: $117.60

Price Target: $128.57

Thesis:

We believe McDonald’s stock is approaching its fair value as it has increased significantly over the last year, and we see less-dramatic growth opportunities going forward. We believe the stock continues to offer shareholders an attractive dividend yield and lower volatility than most stocks.

Weighing the Risks Ahead:

McDonald’s has outperformed an S&P 500 ETF (SPY) by 37% over the last year. However, the company faces a variety of risks moving forward. In the week’s Blue Harbinger Weekly we weigh the risks ahead for McDonald’s, and provide our view on why it might be time to reduce your exposure to this blue chip behemoth. We also provide an update on the one Blue Harbinger stock that announced earnings last week (it beat estimates by a very wide margin, and it continues to look great going forward!).

For starters, McDonald’s has undertaken a variety of initiatives over the last year that have improved the strength of the company and improved its stock price significantly. However, these initiatives are now baked into the stock price, and it is unlikely for McDonald’s to generate the same level of big gains over the next year. We have described these initiatives below.

- Chinese supplier issues: Part of the reason McDonald’s has been able to generate outsize returns over the last year is because the stock was starting from a very low level. McDonald’s stock was still in the dog house (pun intended) due to Chinese supplier issues that caused customers in the region to lose faith in the company. Since then China has been able to rebuild trust from its customers, and this has contributed to stock price gains. And while McDonald’s hopes to maintain the traction they’ve built in China, it is unlikely they’ll experience the same types of gains considering they are starting from a much higher price now (more on valuation later).

- New CEO: Steve Eastbrook became CEO in March 2015, and the stock immediately gained 6% on the news. We believe the stock price will continue to demand a premium with Steve as CEO, but it’s not likely to experience a similar 6% pop in 2016 because there isn’t likely to be another new CEO that is perceived to be even better.

For added color, shareholders were unhappy with the old CEO and welcomed Steve’s previous experience as the Chief Brand Officer of McDonald’s. Not unlike other large global employers, McDonald’s constantly faces brand challenges (for example quality of food perceptions), and thus far Steve has done an excellent job addressing the challenge. For example, he changed some recipes to improve the quality of ingredients (e.g. using real butter in egg McMuffins).

- All Day breakfast: McDonald’s made breakfast items available all day and this had a positive impact on sales. We believe this will continue to be a positive impact going forward, but it’s already baked into the price (more on valuation later).

- Turnaround Plan Completion: McDonald’s has been in a multi-year turnaround plan whereby capital expenditures have been heighted. Turnaround initiatives included significant expenses around reimaging a variety of restaurants. These turnaround plans are largely competed, and as a result capital expenditures are expected to be significantly lower going forward. McDonald’s has been transparent with the progress of the turnaround plans, and the gains from lower future expected capex is largely baked into the price already.

Valuation:

We are raising our McDonald’s price target to $128 per share compared to our previous target of $122.69. To arrive at this valuation we used a discounted cash flow model. Our model assumes approximately $5.1 billion of free cash flow in 2016, a 5.82% weighted average cost of capital and a conservative 1.5% growth rate. Our price target is approximately 9% higher than McDonald’s current market price, and this is not unattractive, especially considering its 3% dividend yield and lower volatility versus the rest of the market. However, this is a lower expected return compared to many other stocks, and McDonald’s faces a variety of risks.

Risk Factors:

- Already Near Fair Value: For starters, we believe McDonald’s is not nearly as undervalued as it was in our last valuation report on July 27, 2015. At that time the price was $97 per share, and we believed the stock had over 26% upside due mainly to the initiatives we described above. Now that McDonald’s has executed on many of those initiatives, we believe the stock has less upside going forward. Our valuation (above) assumed only a 1.5% growth rate for McDonald’s, but if that growth rate falls to only 1% then our price target would fall to only $115 per share, which is $2 lower than its current market price. For reference, McDonald’s global comparable sales grew by 1.5% in 2015 (source: fourth quarter earnings announcement).

- Unattractive Growth Prospects: With many major initiatives now in the past, McDonald’s future growth prospects seem far less attractive.

- Value Menu Initiatives: One potential source of growth is the company’s expansion of “value initiatives.” For example, McDonald’s recent “Two for Two” menu offers may drive traffic in the near term, but eventually the effects of the promotion may wear off, traffic may decrease, and McDonald’s may be left with reduced traffic spending at lower price points.

- REIT Spinoff: Another potential source of growth is the possibility of a REIT spinoff. There has been some talk among McDonald’s board as to unlocking shareholder value by spinning off the company’s real estate into a real estate investment trust (REIT). We believe this could unlock a one-time valuation increase for shareholders, but this seems unlikely based on recent news as we have written about here. Further, we don’t believe it offers as much stock price appreciation potential as the company has achieved over the last year.

- Changing Consumer Preferences: There is a constant and evolving risk that consumer preferences could shift away from McDonald’s and more towards, smaller, healthier, more socially responsible restaurants. We believe there is some truth and some falseness to this perception. It is true that consumer preferences change, and may shift away from McDonald’s. However, McDonald’s has very significant socially responsible initiatives underway to address customer concerns. More information is available on the Sustainability section of the company’s website. In our view, McDonald’s often receives a disproportionately large amount of negative media attention simply because it is so large that it has become an easy target for a variety of activists and causes.

- Currency Risks: The impacts of foreign currency exchange rates are largely out of McDonald’s control, and they have had a significantly negative impact on the company’s recent earnings. For example, McDonald’s consolidated revenues decreased 7% in 2015, but would have actually increased 3% if it were not for the strong US dollar. We believe any strong currency moves in the opposite directions could cause a jump in McDonald’s earnings. However, this is not a long-term strategy, and we don’t expect it to significantly improve earnings on a sustainable basis. And in fact, it could continue to move against McDonald’s in the future.

Conclusion:

We rate McDonald’s a hold with a price target of $128.57. We are not yet selling our MCD holdings, but we are not adding to our position either. We are currently reinvesting all McDonald’s dividend payments into other stocks. We still believe McDonald’s stock has price appreciation potential, but simply not as much as it had a year ago due to its recent strong rally. We recognize the stock offers an attractive dividend yield (over 3%) and lower volatility. We believe the stock is still attractive to income investors (we own it in our Income Equity portfolio), and we continue to hold it in our Disciplined Growth strategy as well because it offers some price appreciation potential and it adds important diversification to the strategy.

Will Oil Drag the Market Lower Again?

The market followed oil lower last week as crude inventories exceeded expectations. Important economic releases this upcoming week include crude inventories on Wednesday (2/10) and retail sales on Friday (2/12). In this week’s Weekly we review the Blue Harbinger stocks that announced earnings last week (they were better than expected) and the ones that announce this upcoming week. We also share a top contrarian idea we’ve been working on to profit from “low for longer” oil prices.

Upcoming Earnings Announcements: Plenty of Upside Ahead

In this week’s Weekly, we review the Blue Harbinger stocks that announced earnings last week (they completely knocked it out of the ball park), and we explain why we believe they’ll continue to deliver very big gains going forward. We also review the Blue Harbinger stocks that will be announcing earnings over the next two weeks, and why we believe they too will deliver terrific results. Also worth noting, this weekend Barron’s announced it is “Time to Buy Bank Stocks.” We highlight our favorite bank stock in particular.

Are You Diversified? Appropriately?

Long-term investors should not forget the risk-reward tradeoff. For example, if you were diversified into investment-grade bonds over the last year then your account balance probably hasn’t suffered as much as if you’d invested entirely in stocks. However, over the long-term, we expect stocks to significantly outperform less-risky bonds. This week’s Weekly highlights some extremely attractive stock-specific opportunities that have been created by 2016’s recent market volatility.

Attractive Dividend Yields: Healthcare REITS

This week we review how recent market declines have created some very attractive dividend yields, especially for our favorite healthcare REIT (Hint: It's one of the REITs in this table, and no, it’s not Omega!). We also provide a review of our favorite industrials stock (not a REIT!) which happens to be offering an extremely attractive dividend yield right now. Additionally, we share our view on how we expect this earnings season to impact the sharp decline in stocks we’ve experienced so far this year.