On social media, the line is often blurred between attractive growth stocks and ugly (emotionally-charged) meme stocks. And when you throw in an overly-sensationalized dose of internet fear mongering and logic-defying greed, investors are often left in the lurch. In this report, I rank and countdown my top 10 disruptive growth stocks, including an attractive mix of blue-chip megatrend leaders as well as lesser-known up-and-coming market disruptors (carefully balancing current valuations against long-term potential, and thereby keeping emotions in check). Enjoy!

Meme Stock Bubble?

Before getting into the top 10 ranking and countdown, it’s worth first asking the question: Are we in a (meme stock) bubble?

From a short-term perspective, and if you haven’t been paying attention, you might not realize the market is up 20% (S&P500) since the depths of the Trump tariff turmoil 3 months ago. And select high-growth stocks (arguably “meme” stocks) are up dramatically more (see table below).

Some media pundits are arguing we’re in a bubble, while others suggest “this time it’s different.” I’ll argue my case for when this “meme stock” bubble will burst (and how you might want to play it) in the conclusion of this report.

Entire Market Bubble?

And from a longer-term perspective, two of the most common arguments I hear to suggest we’re in an “entire market” bubble are market valuations (such as price-to-earnings ratios—they’re at historical highs) and the massive size of the top 10 US stocks by market cap (in percentage terms relative to the rest of the market).

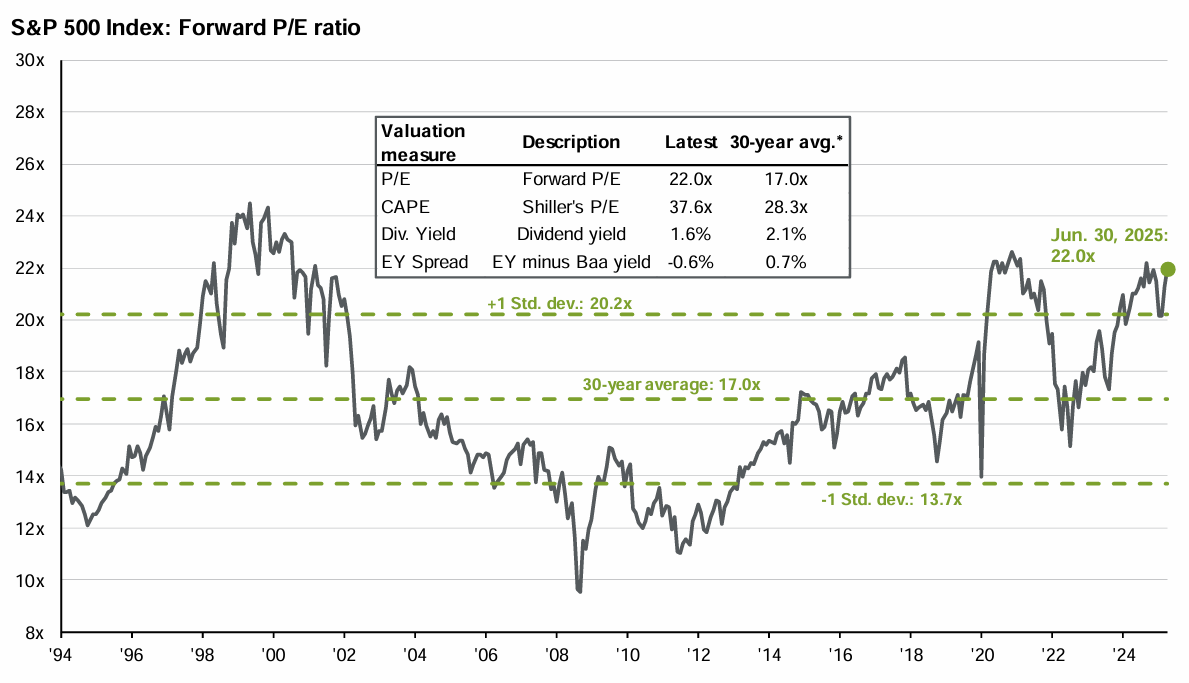

For example, you can see in the following chart (as of June 30th) forward P/E ratios on the S&P 500 are well above the 30-year average (and they’ve only gotten higher as stocks are up so far this month—and quarterly earnings season is only just beginning).

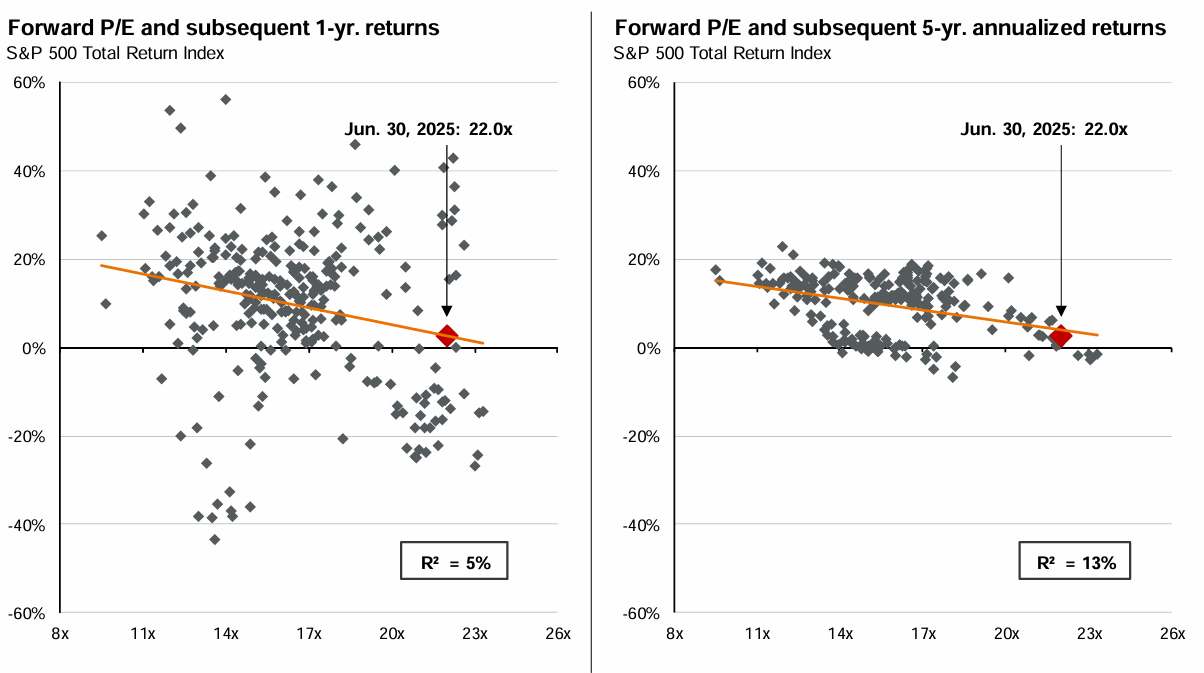

And then of course subsequent stock market returns are lower when the P/E ratio is higher, as you can see in this next chart.

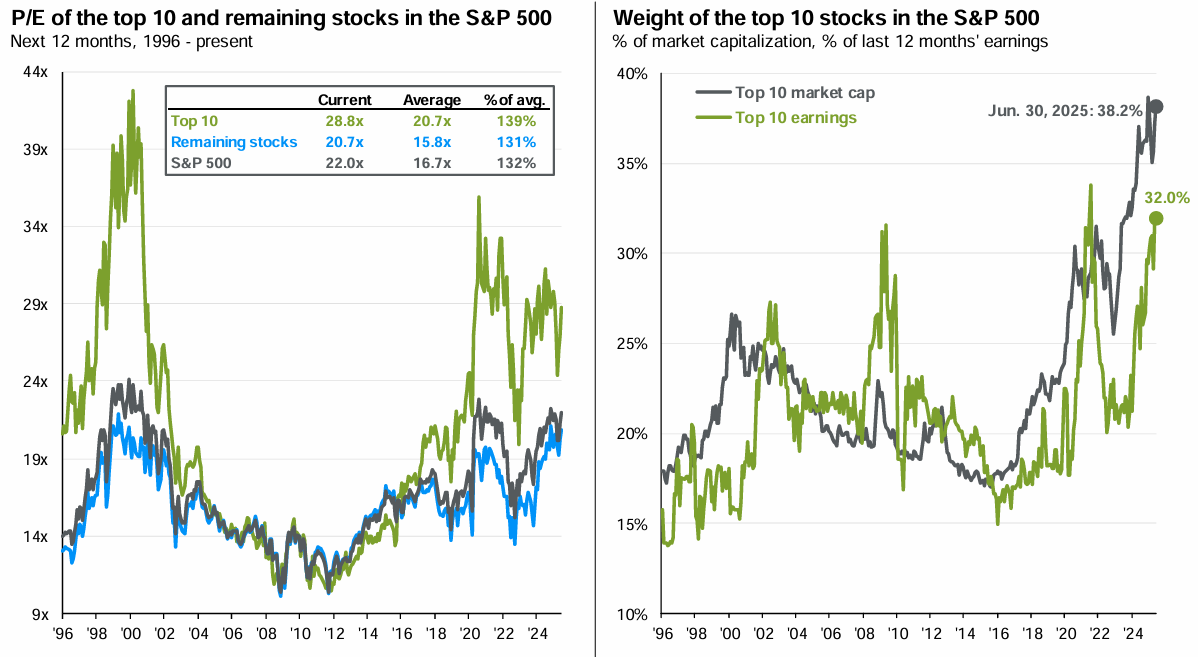

And then here is a look at just how big the top 10 US stocks (by market cap) are related to the rest of the S&P 500 (i.e. they’re really big right now, and their P/E ratios are really high).

So by traditonal, high-level metrics, the stock market is a little “frothy” right now, to put it mildly (more on this in the conclusion).

Top 10 Disruptive Growth Stocks (Ranked):

So with that backdrop in mind, and remembering that not all disruptive growth stocks are meme stocks (select names are supported by extremely healthy fundamentals), let’s get into the top 10 ranking and countdown.

10. SoFi Technologies (SOFI):

SoFi is an impressive disruptive growth stock effectively capitalizing on fintech opportunities and millennials' distrust of traditional finance. It continues to release innovative new products (such as cryptocurrency and private equity) beyond just student loans (which remain an attractive first product for the company to get its foot in the door with future high earners). The shares are up more than 200% over the last year, which makes some investors nervous, but the market opportunity remains large.

You can view my full report on SoFi here.

9. Meta Platforms (META)

If ever there was a company that symbolized “revenge of the nerds,” this would be it. Nerdy CEO Mark Zuckerberg grew his Facebook app (which stalks user data and sells it for advertising revenue) into Instagram (more social media creepiness) and WhatAp (the grand daddy of creepy stalker-ness because AI listens to your phone calls and is just now beginning to unlock this massive new advertising revenue source). Plus, Zuckerberg is relatively young for a CEO and still seems dead set on growing his creepy empire of social media stalker-ness). At 25x forward earnings, with double digit growth and incredible margins, this megacap still has lots of room to run.

You can view my latest full report on Meta here.

8. Vertiv (VRT)

Vertiv basically makes electrical components for datacenters, and this positions the company (a leader in the space) smack dab in the middle of the AI megatrend. Demand is high and will likely remain so as the AI megatrend continues to need data centers. However, the valuation, relative to the demand growth, is low (a good thing). Trading at 6.3x sales and 31.1x forward earnings (with a double-digit revenue growth rate), Vertiv is worth considering.

You can view my previous full report on Vertiv here.

7. Innodata (INOD)

It’s a bit of a turnoff to see a 30-year-old stock marketing itself as an Artificial Intelligence play (considering that’s a megatrend that only just started to ramp within the last 2-years). Nonetheless, Innodata (INOD), a data engineering company, is finding its niche (capitalizing on the surging demand for high-quality AI training data) and hitting its stride (5 “Mag 7” clients) with a lot of room to run (massive TAM) and a reasonable valuation (7.6x sales).

You can view my latest full report on Innodata here.

6. Astera Labs (ALAB)

Astera Labs presents a compelling investment opportunity thanks to its important role in the AI megatrend (it solves connectivity bottlenecks), combined with its dramatic growth trajectory. And contrary to initial sticker shock, its valuation metrics are arguably very compelling as compared to its tremendous ongoing growth rate (Wall street rates it a “strong buy” and the shares can easily 2x considering growth is set to more than 2x in the coming years while profit margins will expand for this already profitable young business, and the long-term TAM is even dramatically larger still).

You can view my latest full report on Astera Labs here.

5. Microsoft (MSFT)

Microsoft is a special company because it leads in so many ways. For example, in addition to its strong financials (i.e. consistent revenue growth and very high profit margins) and its dividend reliability (it yields 0.65% but the actual dividend has been growing rapidly for decades), it also dominates in the cloud megatrend (Azure is now the second largest cloud provider behind Amazon Web Services, but Azure is growing faster), AI innovation (its heavy investment in AI, including Copilot and partnership with OpenAI) and its overall diversified portfolio (from Windows to Office 365 and gaming), Microsoft is a juggernaut and one of my largest positions.

4. CoreWeave (CRWV)

Similar to Nebius (see table above), CoreWeave partners with Nvidia to give hyperscalers (like Microsoft and Meta) early access to Nvidia’s latest GPUs in datacenters prepped and primed for the demands of AI. Personall, I purchased shares in the $60, sold 2/3 over $150, and now the most recent price pullback makes the shares even more attractive again. I believe these shares still have dramatic upside potential.

You can read my recent CoreWeave report here.

3. Alphabet (GOOGL)

Google generates big revenue with its world-dominating search engine (which generates massive high-margin ad revenue), its YouTube platform (which generates massive high-margin ad revenue) and its cloud services (which generates massive high-margin revenue). In fact, it is all of this massive high-margin revenue that allows Alphabet to spend heavily on other big bets, such as Waymo (its differentiated competitor to Tesla in self-driving vehicles) and its own AI model called Gemini.

However, despite all this massive high-margin revenue and constant innovation, Alphabet’s share price has been relatively weak because people think other AI models (such as ChatGPT and DeepSeek) are going to dethrone Google as the dominant search engine (or at least cut into its profit margins significantly). To the contrary, we view this as an attractive opportunity to own shares of one of the best Mag 7 stocks at an attractive price.

You can read my recent writeup on Alphabet here.

2. ServiceNow (NOW)

If you are looking for disruptive companies with sticky high revenue growth that have shares with recent relative underperformance (i.e. margin of safety), consider ServiceNow. It’s a leader in cloud-based workflow automation solutions, benefiting dramatically from the ongoing digital revolution and AI megatrends.

You can view my latest full report on ServiceNow here.

1. Nvidia (NVDA)

If you are sick-and-tired of hearing about what a great company Nvidia is—don’t be. It’s basically ground zero for the ongoing AI megatrend (because its GPU chips basically fuel 90%+ of all AI) and it’s still cheap (i.e. it trades at an attractively low >30x forward PE with incredible revenue growth and high margins). Demand is still higher than Nvidia can deliver chips—the ideal situation for pricing power and attractiveness.

You can view my recent report on Nvidia here.

How should you play the current “Frothy” market conditions?

So with those rankings in mind, the “boring” answer (to the above question) is that you should play the market according to your own personal goals. If you cannot handle another 20% or 30% or more pullback and market correction—then for goodness sake don’t put everything you own in the stock market (especially growth stocks!).

But if you have a longer-term horizon (7-10 years or more) then stay invested. Don’t try to time the market’s short-term moves. You WILL get it wrong (despite armies of media pundits and sales people that will tell you otherwise—hint: they just want your money).

How am I playing the current “Frothy” market conditions?

As mentioned, I currently own most of the top 10 (see my Disciplined Growth Portfolio), but I am NOT being overly aggressive right now (but I am sticking to my long-term goal-focused strategies).

For example, my Disciplined Growth Portfolio is still overweight megatrend themes I like (such as AI, the cloud and related businesses), but I am not being overly aggressive (I still have exposure to other market sectors and business strategies) and I am absolutely NOT going all in on meme stocks right now.

And in my High Income NOW” strategy, I am not being overly risky compared to usual, but I am still staying exposed to a prudently-concentrated portfolio of high-income opportunities. I know that both strategies seem very different, but they are both still affected by the same market volatility and economic conditions.

And I also know that all investment decisions should be driven by your own personal situation and goals.

The Bottom Line

Yes, we’re in a bubble. It’s driven by inflation, fiscal and monetary policies and high-valuations (particularly by social media exuberance for meme stocks).

But that does NOT mean it will burst tomorrow, next month or even next year. In my opinion, now is NOT the time to bet your livelihood on meme stocks, but it is time understand your personal situation and stick to a prudent, long-term, goal-focused strategy.

*You can view all of my current holdings (including portfolio weights) here.