AI Software | The Debasement Trade (Gold, Silver, Crypto) | Private Credit

I start with this long-run versus short-run illustration to remind investors that when the market seems “dramatic” (like it may seem recently), disciplined long-term investing is often the best course. However, periodically adjusting your portfolio around the edges (to manage risks and take advantage of opportunities) is warranted. This report reviews 3 dramatic market themes currently dominating the headlines and daily market swings, and then shares specific ideas on how to play them.

Theme 1:

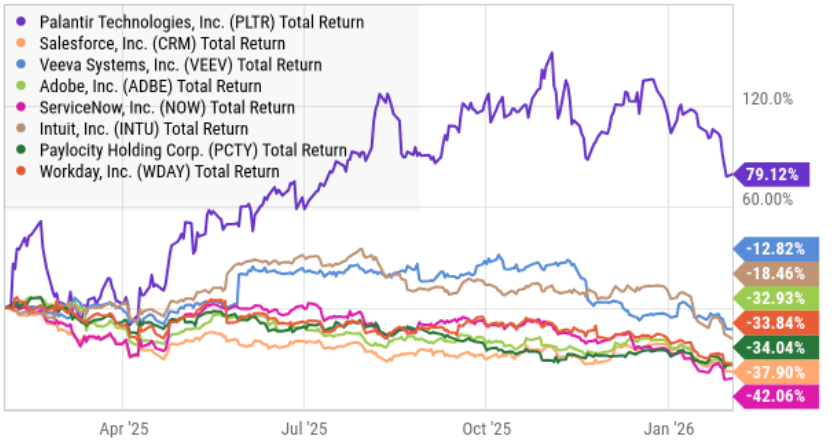

AI’s Big Winners and Big Losers: Palantir Vs Everyone Else

As you can see in the chart below, AI software darling, Palantir (PLTR) is continuing to dominate the software space as a big winner (especially after its latest earnings announcement) while once beloved Software stocks (especially Software-as-a-Service stocks) are falling steadily.

The market narrative is that AI is quickly making once favored SaaS stocks increasingly irrelevant to the future. For example, Palantir is taking unstructured data, organizing it, and making it extremely useful—fast—and with far less human beings needed in the process. “Better. Faster. Smarter.” as the business saying often goes.

Along these lines, one of the reasons the S&P 500 index is so hard for many investors to beat is because it adjusts periodically to reflect changes in company sizes (the S&P 500 is a market-cap-weighted index). And from a market cap standpoint, leading AI companies like Palantir, and frankly all of the Magnificent 7 stocks, have increased in size and weighting in the US markets. Rather than hiding from this reality (they are big growing businesses) investors may want to lean into it, just like the S&P 500 index does, so they don’t miss out (or overexpose themselves) to these increasingly dominant parts of the market. After all, with the US people and government working hard to keep the economy strong, they want to support these big companies—not hide from them.

Google's Big Rally: Ranking The Magnificent 7 (2026-2027) — Blue Harbinger Investment Research

Palantir: 5 Big Risks of Backward-Looking Financial Analysis — Blue Harbinger Investment Research

Theme 2:

The Debasement Trade: Gold & Silver (Commodities) + Crypto

It’s no secret that the US government credit rating has declined and national debt and deficits rise over time (combined with a US Congress that seems to spend more time fighting than anything else). These factors, combined with heightened global politics and inflation (Congress keeps spending and central banks regularly manipulate the value of currencies) leave a lot of investors looking for alternatives.

The classic “debasement trade” is owning gold. After all, the US dollar used to be backed by gold, and people have used it as a currency for many centuries. Additionally, many national governments have increasingly been stock piling gold (e.g. Russia, China, India). All of this adds to its recent epic rally (which has also recently extended to silver too—although silver is also impacted by industrial demand).

Another alternative currency is cryptocurrency (such as Bitcoin). A ton of investors view crypto as an alternative to the US dollar—although it isn’t backed by any world superpower (such as the US). Rather, crypto is backed by limited supply and strong demand (which can shift). There is increasingly talk of stable coins as an alternative to volatile Bitcoin and such, but any stable coin backed by a national government automatically loses a lot of the allure that makes crypto currencies attractive in the first place.

Theme 3

Private Credit Investments

There has been a growing infatuation with private credit investments since the Great Financial Crisis in 2008-2009 mainly because people wanted out of the stock market (because they thought it was too risky) and they didn’t want to buy traditional “bonds” because interest rates were too low (again, central banks were holding interest rates artificially low to boost economic recovery) and then duration bond prices fell too hard (when the fed rapidly increased interest rates to fight the extreme inflation that they caused in the first place—yuck!). As a result people invested in private credit.

Private credit comes in many forms, ranging from private funds for institutional and high-net-worth investors to Business Development Companies or BDCs (which aren’t really private credit, they’re public equities, but they still give private-credit-like returns and income because BDCs do invest in private credit—that is basically their business—they make private loans).

The problem with private credit now is there are too many people chasing after the same opportunities, which are now arguably a lot less attractive. Specifically, the private-credit-funds space got too big and so did the BDC space, and this leads to too many people chasing after the same opportunities (which drives down returns and can result in lower compensation for taking on risk as credit spreads narrow). Complicating the matter, big banks are now getting back into the space after being basically banned after the Great Financial Crisis due to more restrictive reserve requirements. Big banks will just create more competition and drive down spreads further.

If you are a private credit (or BDC) investor, be highly selective. Winning in this space used to be like shooting fish in a barrel right after the GFC because there were a lot of opportunities and little competition—an environment which has now basically reversed. Further complicating the matter, highly successful and extremely wealthy hedge fund manager, Ken Griffin recently said he fears AI will also put further pressure on this space.

Be highly selective in private-credit-related investments!

The Bottom Line

Three takeaways: (1) If you are going to invest in AI and software, you don’t have to chase value traps. The best business can be too expensive, but they’re almost never going to be extremely cheap. (2) The US dollar continues to face pressure, and it may be a good idea to consider alternatives, but don’t go overboard—especially considering the US dollar is still backed by the full faith and credit of the US government—a continuing economic superpower in the world. (3) Stop chasing high-yield private credit. Now is not the right time for that—considering where we are in the longer-term market cycle.

Overall—be selective. Prudently diversified, goal-focused, long-term investing continues to be a winning strategy.